Threshold vs calendar rebalancing is a comparison between two portfolio review rules. Calendar rebalancing reviews a portfolio on a fixed schedule. Threshold rebalancing reviews the same portfolio against a drift trigger, such as a tolerance band around the target allocation.

Both methods belong inside rebalancing, but they answer different timing questions. A calendar rule asks, “Has the scheduled review date arrived?” A threshold rule asks, “Has the portfolio moved far enough away from target to justify review?”

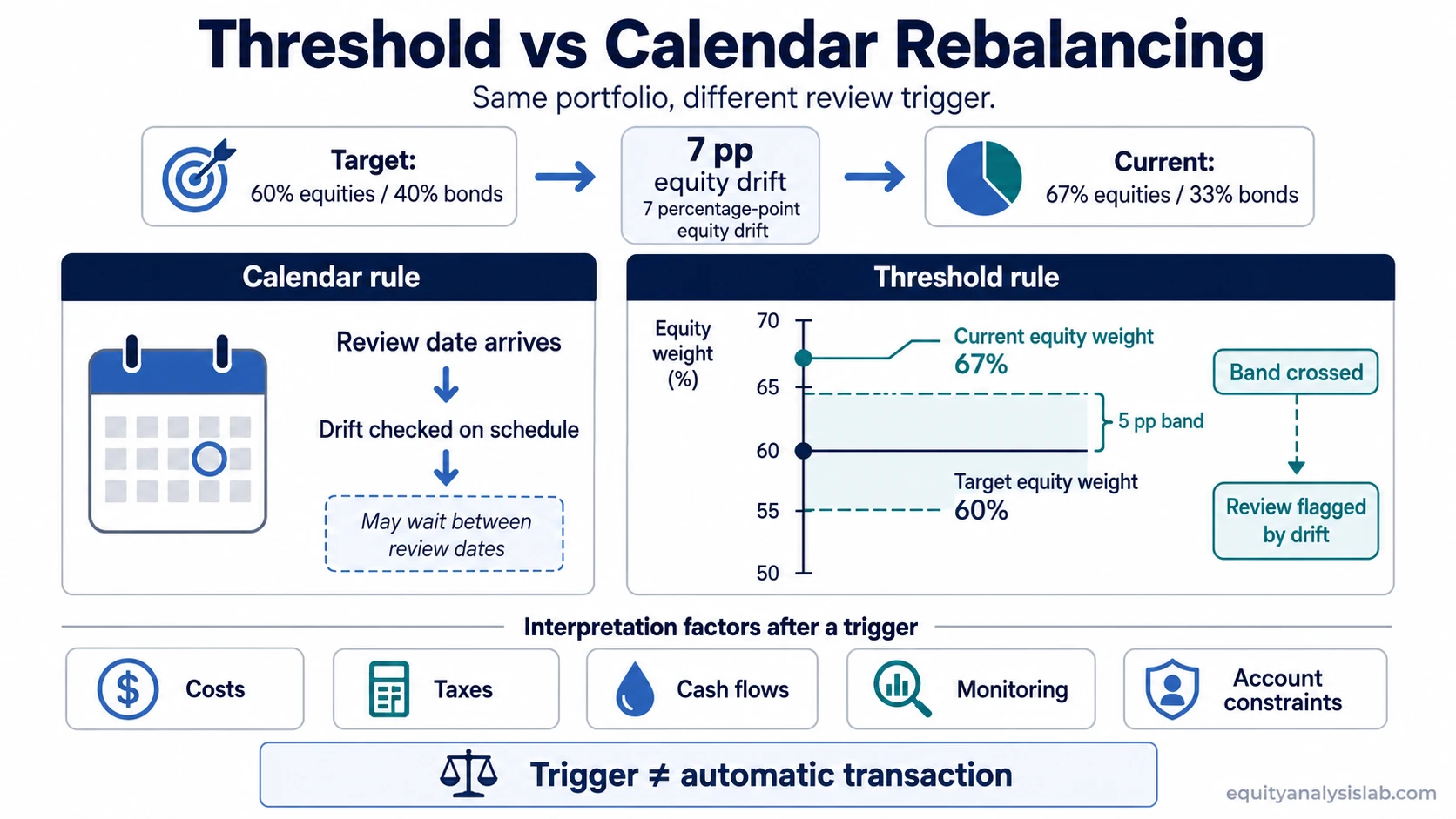

Core distinction: calendar rebalancing is time-based, while threshold rebalancing is drift-based. The difference is not the portfolio itself, but the rule that decides when the portfolio gets reviewed.

Key Points

- Calendar rebalancing uses fixed review dates, such as monthly, quarterly, semiannual, or annual reviews.

- Threshold rebalancing uses allocation drift, such as a 5 percentage-point band around a target weight.

- The same target allocation can produce different review timing under each rule.

- A calendar rule can be simpler to administer, but it may wait through meaningful drift between review dates.

- A threshold rule can respond directly to drift, but it requires more monitoring and can create more trading events.

- Neither rule proves better outcomes on its own. Costs, taxes, account type, cash flows, and portfolio design all affect interpretation.

What threshold vs calendar rebalancing means

Calendar rebalancing sets a review date before looking at the portfolio. The investor might review weights at the end of each quarter, once per year, or on another fixed schedule. If the portfolio has drifted enough to matter by that date, a trade may be considered.

Threshold rebalancing sets a drift rule before looking at the calendar. The investor might define a tolerance band around each target weight, then review when an asset class moves outside that band. The trigger is not the date itself. The trigger is the distance between the current weight and the target weight.

The confusion comes from the fact that both methods can use the same inputs: target weights, current weights, asset-class values, cash flows, and transaction constraints. The difference is the trigger logic.

Key differences between calendar and threshold rules

| Comparison point | Calendar rebalancing | Threshold rebalancing |

|---|---|---|

| Main trigger | A scheduled review date arrives. | A portfolio weight moves outside a chosen tolerance band. |

| Primary question | Is it time to review the portfolio? | Has the portfolio drifted far enough to review? |

| Typical cadence | Monthly, quarterly, semiannual, annual, or another fixed interval. | Whenever allocation drift crosses the selected threshold. |

| Monitoring burden | Lower, because review dates are known in advance. | Higher, because weights need to be monitored between calendar dates. |

| Drift sensitivity | May ignore drift until the next review date. | Responds directly to drift when the threshold is crossed. |

| Trading risk | Can create trades even when drift is modest if the schedule is applied mechanically. | Can create more frequent trading when markets move around the band. |

| Cost and tax friction | Depends on how often the schedule leads to transactions. | Depends on how tight the bands are and how often they are crossed. |

| Best understood as | A time discipline for reviewing the portfolio. | A drift discipline for controlling allocation movement. |

Same portfolio, different trigger logic

The clearest way to compare the two rules is to hold the portfolio constant and change only the trigger.

Example: an investor has a 60% equity and 40% bond target. After market movement, the portfolio is 67% equities and 33% bonds. The equity allocation is 7 percentage points above target, and the bond allocation is 7 percentage points below target.

That movement is portfolio drift. It does not automatically say whether a trade is necessary. It only measures how far the current weights have moved from the target weights.

| Rule applied to the same portfolio | What the rule notices | Possible interpretation |

|---|---|---|

| Calendar rule | The portfolio is reviewed at the next scheduled date, such as quarter-end or year-end. | If the next review date is near, the drift is assessed then. If the date is far away, the drift may persist until review. |

| Threshold rule with a 5 percentage-point band | The 67% equity weight is 7 percentage points above the 60% target. | The rule flags the portfolio because the drift has crossed the selected 5 percentage-point threshold. |

The same 60/40 portfolio can therefore be treated differently. Calendar rebalancing waits for a scheduled review. Threshold rebalancing reacts when drift crosses the chosen band. That does not prove either method is better. It shows how the review rule changes timing and monitoring behavior.

Why investors confuse the two rules

Calendar and threshold rules are often confused because a scheduled review can still use thresholds. For example, an investor might review a portfolio quarterly but only trade if an asset class is more than 5 percentage points away from target.

Common confusion: a calendar date is not the same thing as a trade instruction. A quarter-end review can simply measure drift. A threshold crossing can trigger review without requiring a transaction if costs, taxes, or cash flows make immediate action unattractive.

The useful distinction is that a calendar rule governs when the portfolio is checked, while a threshold rule governs how much drift matters. In real portfolio maintenance, those two decisions can be separate.

When each rule can create problems

Both approaches can create weak decisions when the rule is applied mechanically. The rule should clarify review discipline, not replace judgment about costs, taxes, account type, liquidity, cash flows, and the purpose of the target allocation.

| Risk area | Calendar rule issue | Threshold rule issue |

|---|---|---|

| Delayed response | Large drift can develop between scheduled dates. | Less likely if monitoring is frequent, but possible if the portfolio is checked rarely. |

| Unnecessary trading | A scheduled review can encourage trades even when drift is small. | A tight band can trigger repeated trades during volatile markets. |

| Monitoring burden | Lower burden because the review date is fixed. | Higher burden because drift must be tracked against the selected band. |

| Tax and cost friction | Frequent scheduled reviews may increase the chance of taxable or costly transactions. | Tight thresholds may create more transaction events if markets cross the band repeatedly. |

| Cash-flow interaction | New contributions may reduce the need to sell overweight holdings at the review date. | Available cash may help correct drift after a threshold is crossed. |

Limitation: a threshold such as 5 percentage points is an illustrative rule, not a universal setting. A narrow band may create more monitoring and trading. A wide band may allow larger drift. The appropriate band depends on portfolio design, account constraints, tax sensitivity, and the investor’s review process.

Can calendar and threshold rules be combined?

Calendar and threshold rules can be combined. A portfolio might be reviewed quarterly, but trades might be considered only when an asset class has moved outside a defined tolerance band. In that structure, the calendar creates the review habit, while the threshold prevents small deviations from automatically becoming trades.

Hybrid rule: review on a schedule, measure drift at the review date, then decide whether the drift is large enough to justify action after considering costs, taxes, cash flows, and account constraints.

This hybrid approach is common because it separates monitoring discipline from transaction discipline. The review can happen on a schedule, while the decision to trade can still depend on drift size and portfolio context.

Related portfolio maintenance concepts

Threshold and calendar rules are only one part of portfolio maintenance. A rebalancing rule becomes more useful when it is connected to target allocation, drift measurement, cash use, account type, and the reason the portfolio was designed that way.

- Rebalancing: the broader process of bringing a portfolio back toward its intended allocation.

- Portfolio drift: the measurement of how far current weights have moved away from target weights.

- Cash position: available cash can sometimes reduce the need to sell overweight assets when correcting drift.

- Costs and taxes: transaction costs and tax consequences can affect whether a trigger should lead to immediate action.

FAQ

Is threshold rebalancing better than calendar rebalancing?

Threshold rebalancing is not automatically better. It responds more directly to drift, but it also requires more monitoring and can create more transaction events if bands are tight. Calendar rebalancing is simpler to schedule, but it may allow drift to persist between review dates.

Is calendar rebalancing the same as periodic rebalancing?

Calendar rebalancing and periodic rebalancing usually refer to the same idea: reviewing a portfolio on a fixed schedule. The schedule may be monthly, quarterly, annual, or another chosen interval.

Can a portfolio use both calendar and threshold rules?

Yes. A portfolio can use scheduled review dates and still require drift to cross a tolerance band before any trade is considered. In that structure, the calendar controls review timing and the threshold controls drift sensitivity.

Does crossing a threshold always mean the portfolio should be traded?

No. A threshold crossing identifies drift. Costs, taxes, cash flows, account type, and portfolio objectives can still affect whether a transaction is appropriate.