A portfolio rebalancing strategy is a rule set for deciding when portfolio weights have moved far enough from the intended allocation to justify review, and whether cash flows, taxes, costs, or turnover make action reasonable.

The framework connects target allocation, current weights, drift, trigger rules, and constraints before any portfolio change is considered. The decision is not only about movement away from the plan. It also depends on how costly, taxable, disruptive, or unnecessary the adjustment may be.

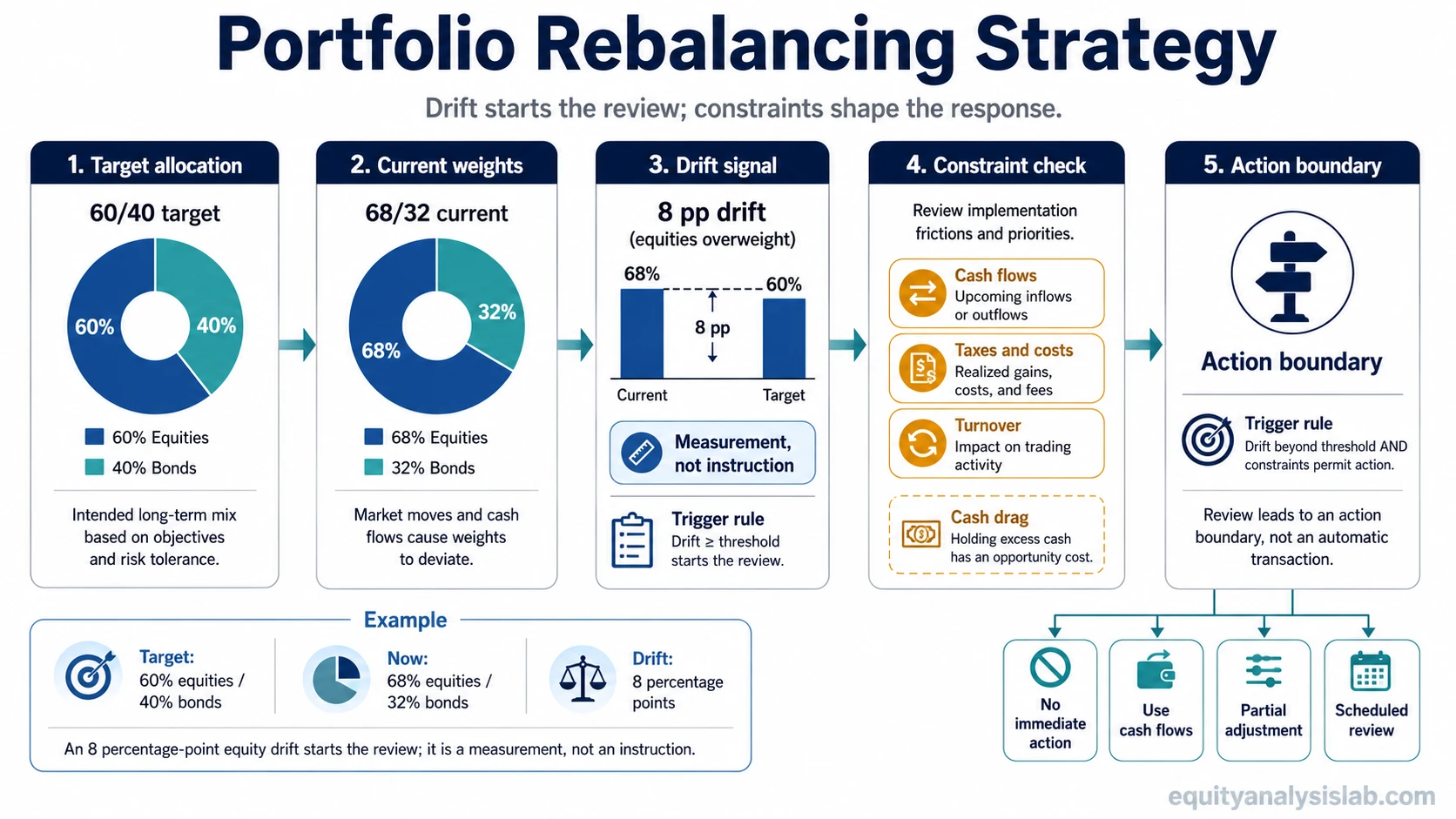

Definition: Portfolio rebalancing strategy is the framework that connects target allocation, current portfolio weights, drift, trigger rules, cash flows, taxes, costs, and action boundaries before a portfolio is moved back toward its intended exposure.

That makes it narrower than general portfolio rebalancing. Rebalancing describes the act of moving weights back toward a target. The strategy defines when that act deserves review, what evidence is checked first, and when no adjustment may be more reasonable than immediate activity.

Key Points

- A rebalancing strategy begins with a clear target allocation.

- Portfolio drift is the measurement that signals weights have moved away from that target.

- Calendar, threshold, hybrid, and cash-flow approaches define different review and action rules.

- Taxes, costs, turnover, and cash position can change whether action is justified.

- The framework weakens when the target is unclear or hidden concentration dominates the visible allocation.

What a Portfolio Rebalancing Strategy Decides

A rebalancing strategy decides how the portfolio moves from observation to possible action. The reference point is asset allocation, because the target weights define what the portfolio is trying to maintain.

The next input is the current portfolio weight. If the actual exposure has moved away from the target, the difference becomes a drift measurement. A small drift may be noise. A larger drift may require review. The strategy defines the boundary between those two states.

The final decision depends on constraints. New contributions, dividends, withdrawals, taxable accounts, trading costs, turnover, and the reason for the target allocation all affect whether a rebalance is justified. A strategy that ignores those constraints can become mechanically active without improving the portfolio’s discipline.

A Framework for Evaluating Rebalancing

A durable rebalancing framework separates measurement, trigger, constraint, action boundary, and failure condition. Those steps prevent a portfolio review from becoming an automatic transaction simply because weights moved.

| Framework component | Question it answers | Evidence or check | What weakens the reading |

|---|---|---|---|

| Target allocation | What exposure was intended? | Stated equity, bond, cash, sector, factor, or asset-class weights. | The target is outdated, vague, or never tied to a real investment plan. |

| Current weights | Where is the portfolio now? | Updated portfolio weights after market movement, contributions, withdrawals, dividends, and cash changes. | Weights are stale, incomplete, or missing indirect exposures from funds and overlapping holdings. |

| Drift signal | How far has the portfolio moved? | Difference between target weights and actual weights, including allocation drift across major exposures. | The drift looks small at asset-class level but hides concentration inside sectors, factors, or correlated holdings. |

| Trigger rule | When does review become action-worthy? | Calendar schedule, threshold band, hybrid review rule, or cash-flow-based adjustment rule. | The trigger is too tight, too loose, or copied without regard to account size, costs, taxes, and portfolio complexity. |

| Constraint check | What could make action unreasonable? | Taxable gains, transaction costs, bid-ask spreads, turnover, account type, and available cash flows. | The rule treats every deviation as equally important even when the adjustment cost is larger than the benefit. |

| Action boundary | What is the least disruptive way to reduce the issue? | New contributions, dividends, withdrawals, partial adjustments, or delayed review before selling existing positions. | The strategy creates unnecessary turnover when cash flows could reduce the drift over time. |

| Failure condition | When is the strategy no longer reliable? | Unclear target, hidden overlap, tax drag, cost drag, cash drag, or a portfolio objective that has changed. | The strategy keeps forcing the old target even after the investor’s constraints or objectives have materially changed. |

Calendar, Threshold, Hybrid, and Cash-Flow Approaches

Calendar rebalancing uses a scheduled review, such as quarterly, semiannual, or annual review. The appeal is consistency: the portfolio is checked at known intervals. The limitation is timing mismatch, because drift may be small on the review date or meaningful before the next scheduled review.

Threshold rebalancing uses tolerance bands. A portfolio might be reviewed when an allocation moves beyond a defined band around the target. This ties action to actual drift, but narrow bands can create excessive activity, especially in taxable or high-cost accounts.

A hybrid approach combines both ideas. The portfolio is reviewed on a schedule, but action depends on whether drift, costs, taxes, and constraints justify adjustment. The rule needs enough clarity to avoid subjective changes every time the portfolio is reviewed.

Cash-flow rebalancing uses contributions, dividends, interest, withdrawals, or available cash before selling existing holdings. A portfolio’s cash position can therefore become part of the strategy. Cash may help reduce drift, but excessive idle cash can also create a separate allocation issue.

| Approach | How it works | Main benefit | Main limitation |

|---|---|---|---|

| Calendar | Reviews the portfolio on a fixed schedule. | Simple and consistent. | May trigger review when drift is not meaningful. |

| Threshold | Reviews action when an allocation moves beyond a tolerance band. | Responds to actual portfolio movement. | Can create turnover if bands are too narrow. |

| Hybrid | Uses scheduled review plus drift-based action rules. | Combines discipline with flexibility. | Requires clear rules to avoid subjective changes every review. |

| Cash-flow | Uses new money, dividends, interest, or withdrawals to reduce drift first. | May reduce the need to sell existing holdings. | May be too slow if drift is large or cash flows are limited. |

Portfolio Rebalancing Strategy Example

A portfolio has a target of 60% equities and 40% bonds. After market movement, the actual weight becomes 68% equities and 32% bonds.

The 8 percentage-point equity overweight is a measurement, not an automatic instruction. The strategy first checks whether that drift exceeds the chosen tolerance band. It then evaluates whether new contributions, dividends, or scheduled cash additions could move the portfolio closer to target without selling existing holdings.

If selling would create a taxable gain, high transaction cost, or unnecessary turnover, the strategy may treat immediate adjustment as less attractive. If the investor’s target allocation is no longer valid because objectives, time horizon, or risk capacity changed, returning mechanically to the old 60/40 target may be the wrong reference point.

Drift identifies the issue; constraints determine whether the response should be immediate, partial, delayed, or handled through cash flows.

Where a Rebalancing Strategy Can Fail

A rebalancing strategy can fail when it treats the target allocation as precise but the target itself is weak. If the target does not reflect the investor’s objectives, time horizon, liquidity needs, or risk capacity, the strategy may enforce a number that does not deserve enforcement.

It can also fail when visible asset-class weights hide underlying concentration. A portfolio may look balanced between equities, bonds, and cash while still carrying heavy exposure to one sector, one factor, one currency, one employer, or one economic driver.

Limitation: Rebalancing can reduce drift from a stated target, but it does not guarantee better returns, lower losses, or better timing. Costs, taxes, turnover, and hidden overlap can make a mechanically correct adjustment less useful than it appears.

Common mistake: Treating every drift reading as a transaction signal can create false precision. A stronger strategy separates the size of the drift from the cost of correcting it.

Changing the Target Is Different From Rebalancing

Rebalancing moves the portfolio back toward an existing target. Changing the target changes the plan itself. That distinction matters because a portfolio can look out of balance for two different reasons.

In one case, market movement pushed weights away from a still-valid allocation. In the other case, the intended allocation no longer fits the investor’s objectives or constraints. The first problem may call for a rebalancing review. The second requires a target-allocation review before any rebalancing rule can be trusted.

How the Core Concepts Fit Together

Asset allocation defines the reference point for portfolio weights. Rebalancing describes the act of moving weights back toward that target. Portfolio drift measures how far the current portfolio has moved. Cash position affects how much flexibility exists before selling holdings becomes necessary.

| Concept | Role in the rebalancing strategy |

|---|---|

| Target allocation | Defines the intended exposure that the strategy compares against. |

| Rebalancing | Describes the portfolio adjustment that may happen after review. |

| Portfolio drift | Measures the distance between target weights and actual weights. |

| Cash position | Shows whether cash flows or existing cash can reduce drift before selling holdings. |

FAQ

What is a portfolio rebalancing strategy?

A portfolio rebalancing strategy is a rule set for deciding when portfolio weights have moved far enough from target allocation to justify review, and whether cash flows, taxes, costs, or turnover make adjustment reasonable.

Is calendar or threshold rebalancing better?

Neither approach is universally better. Calendar rebalancing is simpler, while threshold rebalancing responds to actual drift. A hybrid rule can combine scheduled review with drift-based action boundaries.

Does portfolio drift always mean a portfolio should be rebalanced?

No. Drift is a measurement. The decision depends on the size of the drift, the validity of the target allocation, account type, taxes, costs, turnover, and available cash flows.

Can cash flows be used for rebalancing?

Yes. Contributions, dividends, interest, withdrawals, and existing cash can help move weights closer to target before selling current holdings. The usefulness depends on the size of the drift and the available cash flow.