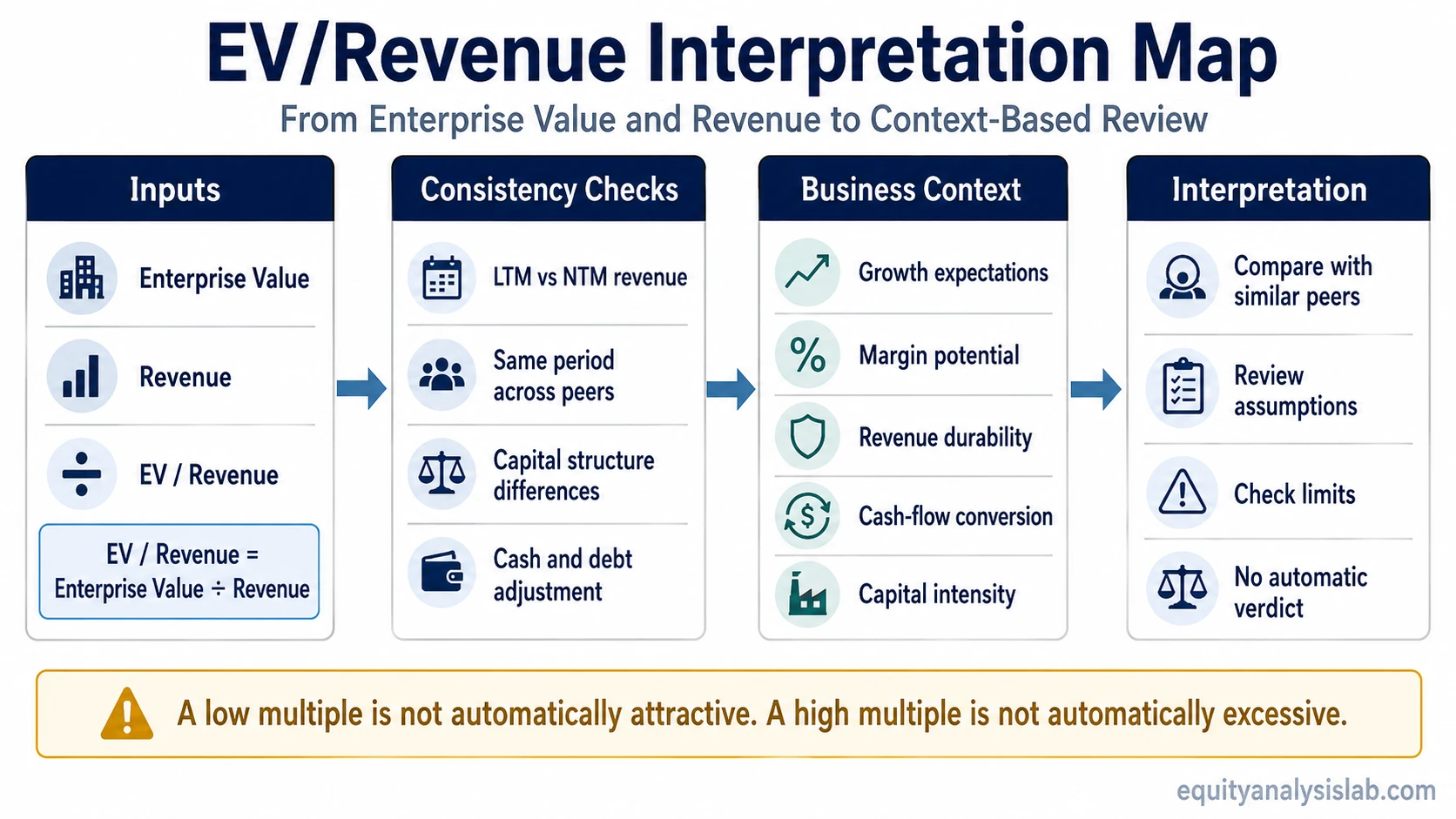

EV Revenue lets an investor compare enterprise value with revenue when profit-based metrics are weak, unavailable, negative, or not yet stable. The EV Revenue multiple, also called EV-to-Revenue or EV/Revenue, divides enterprise value by revenue to show how much total company value is being assigned to each unit of sales.

Key Points

- EV Revenue compares enterprise value with revenue, not market capitalization with revenue.

- The formula is EV / Revenue = Enterprise Value / Revenue.

- The multiple can be useful when earnings, EBITDA, or EBIT are negative, distorted, or temporarily unstable.

- Interpretation depends on peer comparability, growth expectations, revenue durability, margin potential, capital intensity, and cash flow quality.

- A lower EV/Revenue multiple is not automatically attractive, and a higher multiple is not automatically excessive.

What EV Revenue Means

EV Revenue is a valuation multiple that compares a company’s enterprise value with its revenue. It answers a narrow question: how much total company value is being placed on each dollar of sales before profitability, margins, debt structure, and cash-flow conversion are fully judged.

The multiple is most useful as a starting point, not as a conclusion. It helps compare companies whose profit measures are not yet reliable, but it cannot show whether those sales will become durable earnings or free cash flow.

That distinction matters because revenue is high in the income statement and far away from owner-level economics. A company can report strong sales while still producing weak margins, heavy reinvestment needs, high dilution, or poor cash conversion.

EV Revenue Formula

EV / Revenue = Enterprise Value / Revenue

Enterprise value is usually calculated as market capitalization plus debt and preferred claims, minus cash and cash equivalents. The goal is to measure the value of the operating business before focusing only on the equity portion.

Revenue is usually taken from a defined period. Analysts may use annual revenue, last twelve months revenue, or next twelve months revenue depending on the purpose of the comparison. The denominator must be consistent across the peer set, because an LTM multiple and a forward multiple can tell different stories.

Hypothetical calculation: if a company has an enterprise value of 2 billion and annual revenue of 500 million, its EV Revenue multiple is 4.0x. The calculation is 2 billion divided by 500 million.

The result does not say whether the company is fairly valued by itself. It only creates a common scale for comparing enterprise value against revenue.

What the Multiple Actually Compares

EV Revenue compares a balance-sheet-adjusted value measure with a top-line operating measure. The numerator reflects the value assigned to the whole operating business. The denominator reflects the amount of sales that business generates over the selected period.

| Part of the multiple | What it represents | Why it matters |

|---|---|---|

| Enterprise value | Total business value after considering equity value, debt, and cash | Two companies with similar market caps can have different EV Revenue multiples if their debt and cash positions differ |

| Revenue | Sales generated over a defined period | The same business can show a different multiple depending on whether trailing or forward revenue is used |

| Multiple | Enterprise value per unit of revenue | The number becomes useful only when compared with similar businesses and similar assumptions |

This is why EV/Revenue is often used for companies where earnings are negative or temporarily depressed. The revenue base may still be observable even when operating profit is not yet meaningful.

How to Interpret EV Revenue

EV Revenue is usually interpreted through peer comparison. A 3.0x multiple may look high in one industry and low in another because margin structure, growth durability, capital intensity, cyclicality, and revenue quality differ across business models.

A higher EV/Revenue multiple may signal stronger expected growth, higher future margins, more recurring revenue, better retention, lower capital intensity, or a stronger balance sheet. It may also signal excessive expectations if those assumptions are not supported by future results.

A lower EV/Revenue multiple may signal slower growth, weaker margins, customer concentration, cyclical revenue, poor cash conversion, balance-sheet stress, or a business model that requires heavy reinvestment. It may also indicate a more modest valuation if those risks are overstated by the market.

Interpretation rule: EV Revenue should be read as an assumption-sensitive comparison. The multiple becomes more meaningful when the peer group is close, the revenue denominator is consistent, and the margin path is explicitly considered.

EV Revenue Assumption Stack

The surface calculation is simple, but the interpretation depends on several assumptions underneath the number. The same EV/Revenue multiple can point to very different conclusions if the assumptions differ.

| Assumption | Question to ask | How it changes interpretation |

|---|---|---|

| Revenue durability | Are sales recurring, repeatable, or one-time? | Durable revenue can support a higher multiple than volatile or non-recurring revenue |

| Growth expectations | Is the market pricing high future growth or stable maturity? | A high multiple often depends on future growth being sustained |

| LTM vs NTM denominator | Is the denominator based on trailing revenue or forward revenue? | Forward revenue can lower the stated multiple if growth is expected, but it also adds forecast risk |

| Margin conversion | Can revenue convert into EBITDA, EBIT, earnings, or free cash flow? | Revenue without a credible margin path can make EV/Revenue misleading |

| Cash and debt sensitivity | Does the enterprise value change materially because of debt or cash? | Two companies with similar sales can show different multiples because their capital structures differ |

| Capital intensity | How much reinvestment is needed to maintain or grow revenue? | Revenue that requires heavy capital spending may deserve a different interpretation than asset-light revenue |

How Assumptions Change EV Revenue Interpretation

EV Revenue becomes more useful when the analyst tests what must be true for the multiple to make sense. The table below uses generic scenarios, not real company data.

| Scenario | Same reported EV/Revenue multiple | Different interpretation driver | Analytical caution |

|---|---|---|---|

| High recurring revenue, improving margins | 4.0x | Revenue may have stronger conversion potential | Check whether margin improvement is already priced in |

| Fast revenue growth, weak cash flow | 4.0x | Growth may be real, but cash conversion is uncertain | Review working capital, reinvestment needs, and dilution risk |

| Cyclical revenue near a temporary peak | 4.0x | Trailing revenue may overstate normalized sales power | Compare against mid-cycle revenue and margins |

| Low-margin business with heavy capital needs | 4.0x | Sales may not translate into attractive owner earnings | Do not treat revenue scale as value creation by itself |

No scenario is automatically better. EV/Revenue should push the analyst toward the assumptions that explain the multiple.

When EV Revenue Is Useful

EV Revenue can be useful when profit-based multiples are temporarily unhelpful. This can occur when a company has negative earnings, limited EBITDA, early-stage growth, a cyclical margin trough, or accounting costs that make near-term profit difficult to interpret.

The multiple can also help in industries where revenue scale is a relevant first filter, as long as the analyst does not stop at the top line. Revenue must eventually be tested against margins, cash flow, reinvestment requirements, and balance-sheet risk.

For example, two hypothetical companies can each trade at 3.0x EV/Revenue. One may have recurring revenue and a credible path to higher margins. The other may have similar sales growth but high customer churn, weak gross margins, and heavy capital requirements. The same multiple does not carry the same meaning in both cases.

Where EV Revenue Can Mislead

Core limitation: EV Revenue ignores profitability. A company can look modest on an EV/Revenue basis while still failing to turn sales into durable cash flow.

The most common mistake is treating a low EV/Revenue multiple as automatically favorable. A low multiple may reflect real business weakness, declining revenue quality, heavy debt, poor margins, or a peer set that is not comparable.

The opposite mistake is treating a high multiple as automatically excessive. A high multiple may reflect strong revenue durability, expected margin expansion, better cash conversion, or structurally higher returns on capital. It may also reflect expectations that are difficult to meet.

| Misread | Why it is risky | Better check |

|---|---|---|

| Low EV/Revenue means cheap | Revenue may have weak margin or cash-flow quality | Check profitability, free cash flow, and debt burden |

| High EV/Revenue means expensive | The business may have stronger durability or future margin potential | Check growth quality, retention, and operating leverage |

| All revenue is comparable | Revenue mix, recurrence, cyclicality, and accounting treatment can differ | Compare similar business models and similar revenue definitions |

| Trailing revenue is enough | LTM revenue can understate or overstate the forward business base | Review both trailing and forward revenue when forecasts are credible |

EV Revenue Compared With Related Multiples

EV Revenue should stay separate from profit-based valuation multiples. EV/EBITDA valuation compares enterprise value with operating earnings before depreciation and amortization, so it moves one step closer to profitability than revenue.

EV/EBIT goes further by comparing enterprise value with operating profit after depreciation and amortization. That can matter when depreciation, asset intensity, and operating capital requirements are central to the business model.

Price-to-sales is different because it usually compares equity market value with revenue, while EV Revenue compares enterprise value with revenue. The enterprise value approach incorporates capital structure more directly.

Growth-sensitive metrics also have a different job. A valuation multiple can be compared with growth expectations, but a growth-adjusted multiple such as PEG uses earnings-based valuation as its starting point rather than revenue-based enterprise value.

FAQ

What is EV Revenue?

EV Revenue is a valuation multiple that divides enterprise value by revenue. It compares total company value with sales and is often used when earnings or operating profit measures are negative, limited, or unstable.

How do you calculate EV Revenue?

Calculate EV Revenue by dividing enterprise value by revenue. Enterprise value usually includes equity value plus debt and preferred claims, minus cash and cash equivalents. Revenue should come from a clearly defined period such as annual, LTM, or forward revenue.

What is a good EV/Revenue ratio?

There is no universal good EV/Revenue ratio. The right context depends on the industry, peer group, growth expectations, revenue durability, margin potential, capital intensity, and cash-flow conversion.

Is a lower EV/Revenue multiple better?

Not automatically. A lower multiple may reflect a more modest valuation, but it can also reflect weak margins, poor cash conversion, slower growth, cyclicality, debt pressure, or lower revenue quality.

How is EV Revenue different from price-to-sales?

EV Revenue uses enterprise value, which adjusts for debt and cash. Price-to-sales usually uses market capitalization or equity value. This means EV Revenue can be more useful when capital structure differences are important.