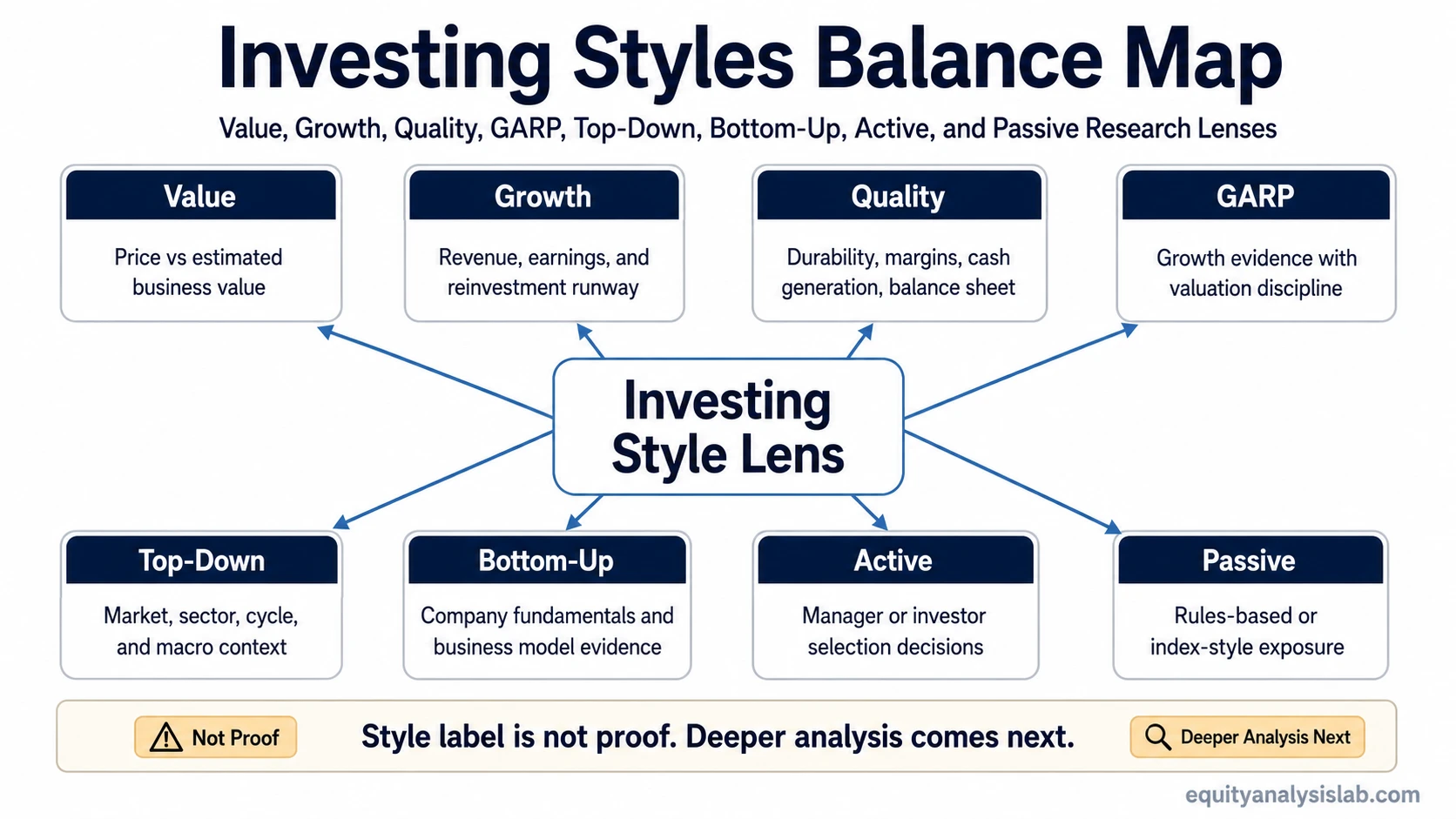

Investing styles are frameworks investors use to decide what kind of evidence matters most when evaluating investments, such as valuation, growth, business quality, market context, or company-specific fundamentals.

A style label does not prove that an investment is attractive. It only describes the lens an investor may use before moving into deeper analysis, such as whether the main question is price versus value, earnings growth, business durability, market context, or company-level research.

Key Points

- Investing styles describe the evidence an investor emphasizes during research.

- Common style labels include value, growth, quality, GARP, active, passive, top-down, and bottom-up investing.

- A style is not a return guarantee, a stock recommendation, or a substitute for company analysis.

- The useful next step depends on whether the reader is comparing valuation, growth, business quality, or research process.

What Investing Styles Mean

An investing style is a research lens. It shapes which questions come first, which evidence receives more weight, and what kind of investment case an investor is trying to understand.

For example, a valuation-focused investor may start with whether a company trades below a reasonable estimate of value. A growth-focused investor may start with revenue expansion, earnings growth, or market opportunity. A quality-focused investor may care more about durable margins, balance-sheet strength, pricing power, or management discipline.

The same company can look different through different style lenses. That is why style should be treated as a starting framework, not as proof that a stock, fund, or portfolio choice is suitable.

Main Investing Style Buckets

Most investing style discussions group around a few recurring questions: whether the investor emphasizes price, growth, business quality, portfolio construction, market context, or company-specific research.

| Style bucket | Main evidence emphasized | What it helps clarify | Main limitation |

|---|---|---|---|

| Value | Price compared with estimated business value | Whether expectations may be low relative to fundamentals | A low price alone does not prove quality or upside |

| Growth | Revenue growth, earnings growth, market opportunity, reinvestment runway | Whether the business may compound faster than mature peers | Growth can disappoint or become overpriced |

| Quality | Durability, margins, balance sheet, cash generation, competitive strength | Whether the business can sustain attractive economics | Quality can still be overvalued or face future deterioration |

| GARP | Growth evidence combined with valuation discipline | Whether growth is being evaluated at a reasonable price | The balance can break if growth slows or valuation expands too far |

| Top-down | Sector, economy, interest-rate, cycle, or market-context conditions | Which areas of the market may deserve deeper review | Broad context can miss company-specific differences |

| Bottom-up | Company fundamentals, business model, financial statements, management, valuation | Whether a specific company deserves deeper analysis | Company analysis can miss broader market or portfolio context |

| Active | Security selection, weighting decisions, research judgment | Whether an investor or manager is making discretionary choices | Active decisions can be wrong and may add cost or complexity |

| Passive | Index exposure, rules-based allocation, benchmark tracking | Whether the approach follows a predefined market exposure | Passive exposure still carries market, concentration, and valuation risk |

How Value, Growth, Quality, and GARP Differ

Value, growth, quality, and GARP are often discussed together because they all influence how an investor interprets company fundamentals. The difference is not only which companies they study, but which evidence they allow to carry the most weight.

Value investing starts with price versus estimated value. The central question is whether the market price may be too low relative to the company’s assets, earnings power, cash flows, or long-term economics.

Growth investing starts with expansion. The central question is whether the company can increase revenue, earnings, cash flow, or market share fast enough to justify the expectations built into the price.

Quality investing starts with durability. The central question is whether the company has strong enough economics, balance-sheet resilience, margins, cash generation, or competitive advantages to sustain value over time.

GARP investing tries to connect growth and valuation. The central question is whether growth is attractive enough without requiring an unreasonable price.

These categories overlap. A company can be growing and high quality, but still too expensive. A statistically cheap company can be low quality. A GARP candidate can stop fitting the label if growth slows or if valuation expectations rise too far.

Top-Down vs Bottom-Up Investing

Top-down and bottom-up investing describe where the research process begins.

A top-down investor starts with larger conditions such as the economy, rates, inflation, sector cycles, market structure, or policy environment. The goal is to narrow the opportunity set before studying individual companies.

A bottom-up investor starts with the company itself. The first questions are usually about business model, financial statements, competitive position, management decisions, valuation, and risks specific to that company.

Neither path automatically produces a better result. Top-down research can miss company-specific differences. Bottom-up research can miss macro, sector, or portfolio-level pressure. The distinction is about research sequence, not proof of investment quality.

Active vs Passive Investing as Style Labels

Active and passive investing describe how investment exposure is selected and maintained. They are style labels, but they work differently from value, growth, quality, or GARP.

Active investing relies on discretionary selection, weighting, timing, or manager judgment. Passive investing usually follows a rules-based index or benchmark exposure. Active and passive are therefore process labels, while value, growth, quality, and GARP are mostly evidence-priority labels.

This difference matters because an investor can combine them. A passive fund can track a value index, a growth index, or a quality index. An active investor can also use value, growth, quality, or GARP criteria when selecting securities.

Which Investing Style Should You Study Next?

The next style to study depends on the question the investor is trying to answer. The useful route is not always the most popular style label; it is the style that matches the evidence gap.

| Reader question | Useful next style | Why it fits |

|---|---|---|

| Is the price low compared with business value? | Value investing | It focuses on price, valuation, and business value estimates. |

| Can the company expand faster than mature peers? | Growth investing | It emphasizes revenue growth, earnings growth, reinvestment runway, and future opportunity. |

| Is the business durable enough to deserve attention? | Quality investing | It emphasizes margins, cash generation, balance-sheet strength, and competitive durability. |

| Is growth being evaluated with valuation discipline? | GARP investing | It connects growth evidence with reasonable-price discipline. |

| Should research begin with the individual company? | Bottom-up investing | It starts with company-level fundamentals before broader allocation judgments. |

Common Mistake: Treating a Style Label as Proof

A common mistake is treating an investing style as if it already confirms the investment case. It does not.

Style label limitation

A stock described as value can still be a value trap. A growth stock can still be priced for unrealistic expectations. A quality company can still be overvalued. A passive index fund can still expose the investor to market drawdowns, concentration, or expensive sectors.

Style labels help organize research, but they do not remove the need for valuation, financial statement review, business model analysis, portfolio construction, or risk review. A style label only says what kind of evidence receives priority.

How to Use Investing Styles Without Overusing Them

Investing styles are most useful when they narrow the research question. They are less useful when they become rigid labels that prevent better evidence from being considered.

Example

An investor may start with a value lens because a company appears inexpensive. If deeper analysis shows weak cash flow, declining competitive position, or a balance sheet that limits flexibility, the value label does not solve the problem. It only identifies the reason the investor looked at the company first.

Two investors can use the same style and reach different conclusions because they use different assumptions, time horizons, valuation inputs, or evidence thresholds. A growth investor may reject a company if growth quality is weak. A value investor may reject a statistically cheap company if the business is deteriorating. A quality investor may reject a strong company if the valuation leaves little room for error.

For that reason, investing style works best as a filter for what to study next. It should narrow the research path, not replace the research itself.

FAQ

What are investing styles?

Investing styles are frameworks investors use to emphasize certain types of evidence, such as valuation, growth, business quality, market context, or company-specific fundamentals.

Is one investing style better than the others?

No single investing style is universally better. A style can fit a research question, time horizon, or evidence preference, but it does not guarantee returns or replace analysis.

Are investing style and asset allocation the same thing?

No. Asset allocation describes how capital is spread across exposures or asset classes. Investing style describes the research lens used to evaluate investments.

How should a beginner compare investing styles?

A beginner should compare the main evidence each style emphasizes, then decide which deeper concept matches the research question: valuation, growth, business quality, GARP balance, or company-first analysis.