Rules-based investing is an investor decision process that uses predefined criteria before a portfolio decision is made. The rules are set before market noise, urgency, or emotional investing pressure can lower the evidence-review threshold.

In this context, a rule is not a buy or sell signal. It is a review guardrail. It asks whether the thesis evidence, valuation evidence, risk boundary, contrary evidence, portfolio fit, and review trigger have been checked before the investor changes exposure, sizing, or conviction.

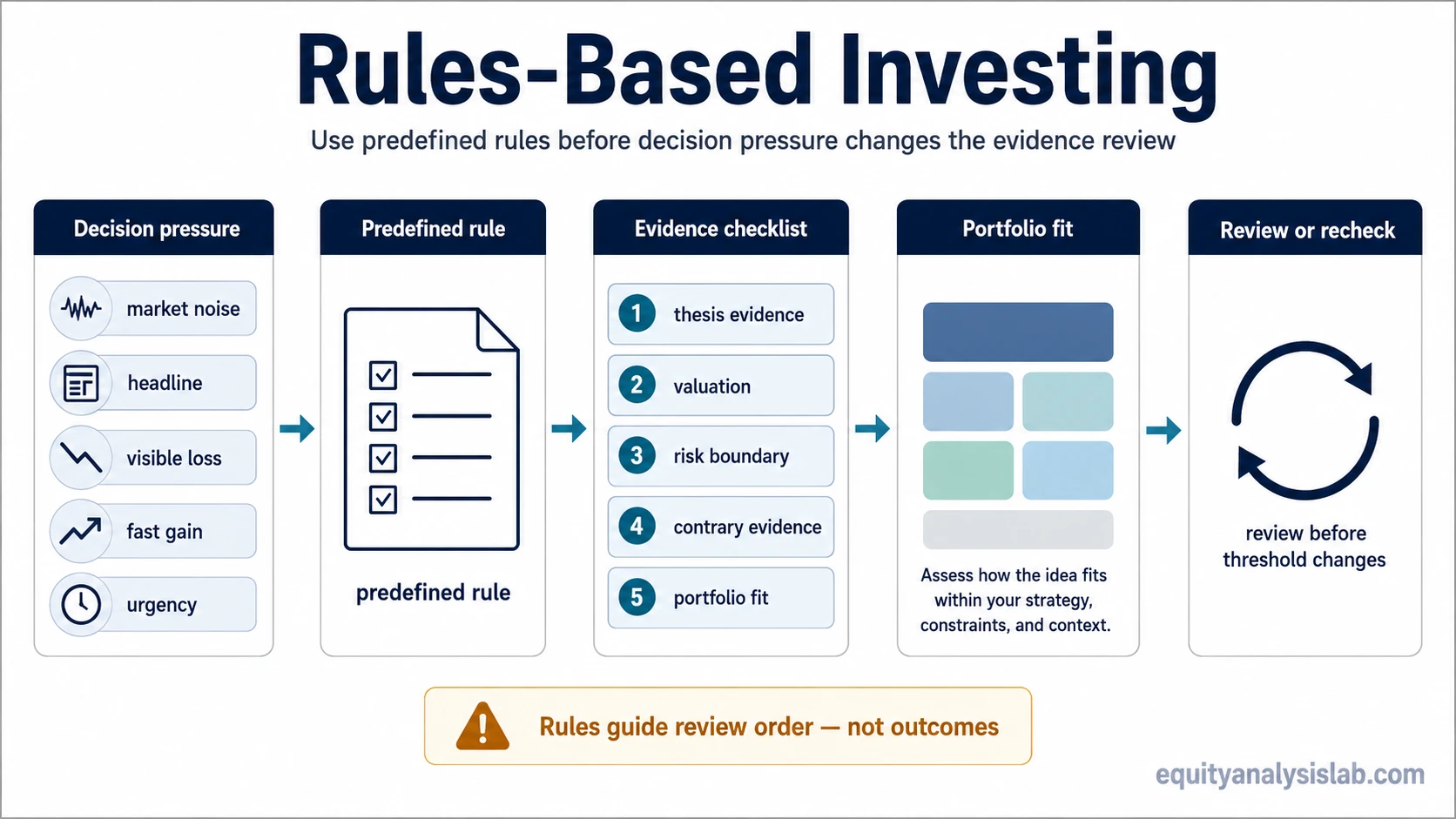

What rules-based investing means

Definition: Rules-based investing means defining the decision conditions before the pressure of the decision arrives. Instead of asking, “What do I feel like doing now?”, the investor asks whether the current evidence still satisfies the rules that were written before the headline, price move, loss, gain, or portfolio pressure appeared.

The rule can be simple or detailed, but its job is the same: keep the decision sequence stable. It does not remove judgment; it makes sure judgment comes after the thesis, valuation, risk, contrary evidence, and portfolio fit have been checked.

Rules-based investing in three points

- Rules-based investing uses predefined criteria before a decision point, not after emotion or market noise has already changed the threshold.

- The checklist should test thesis evidence, valuation, risk, contrary evidence, portfolio fit, and the reason for review.

- The rules reduce review drift; they do not remove uncertainty, guarantee better results, or decide the investment automatically.

Why rules help before emotion or noise changes the review

Investment decisions often become harder after the portfolio is already under pressure. A visible loss can make supportive evidence feel more comforting. A fast gain can make risk limits feel less important. A headline can create urgency before the business evidence has changed.

A written rule gives the investor a fixed review sequence. That matters because loss aversion can make the discomfort of a decline feel more important than the actual change in evidence. The checklist does not say what the investor must do. It forces the review to happen before the decision threshold moves.

The strongest use of rules-based investing is therefore not mechanical prediction. It is process control. The rule separates the current evidence from the pressure created by price, news, recent gains, recent losses, or portfolio regret.

How a rules-based investing checklist works

A rules-based investing checklist should be narrow enough to use repeatedly and broad enough to prevent one piece of evidence from dominating the decision. For an investor, the checklist usually works best when it reviews the investment thesis, valuation, risk, contrary evidence, portfolio fit, and the reason for reopening the decision.

| Checklist area | Question the rule should ask | What it prevents |

|---|---|---|

| Thesis evidence | Has the business, earnings, cash flow, competitive position, or original thesis changed? | Reacting to price movement without checking whether the underlying reason to own or avoid the investment has changed. |

| Valuation evidence | Is the expected return still reasonable relative to the price, assumptions, and margin of safety? | Treating a good company or appealing story as automatically attractive at any valuation. |

| Risk boundary | What evidence would show that the thesis is weakening or no longer fits the original risk case? | Moving the risk boundary after the position becomes emotionally harder to review. |

| Contrary evidence | What evidence argues against the preferred interpretation, and has it been reviewed directly? | Accepting only supportive information while delaying or softening uncomfortable evidence. |

| Portfolio fit | Does the position still fit concentration limits, liquidity needs, time horizon, and the rest of the portfolio? | Letting conviction in one idea override portfolio-level discipline. |

| Review trigger | Why is the decision being reopened now: new evidence, price movement, emotion, or external noise? | Confusing urgency with evidence. |

The checklist is most useful when it is written before the investor needs it. A rule created during stress can easily become a justification for the decision the investor already wants to make.

Rules-based investing vs discretionary reaction

Rules-based investing and discretionary judgment are not opposites. A rules-based process can still include judgment, but it requires the judgment to pass through the same review structure each time. A discretionary reaction begins with the current feeling, narrative, or pressure and may only search for evidence afterward.

| Decision area | Rules-based investing | Discretionary reaction |

|---|---|---|

| Starting point | Predefined review criteria | Current feeling, headline, price move, or portfolio pressure |

| Evidence order | Thesis, valuation, risk, contrary evidence, and portfolio fit are checked in sequence | Evidence may be selected around the preferred decision |

| Role of emotion | Emotion can trigger a review but should not control the evidence threshold | Emotion can decide which evidence feels important |

| Role of judgment | Judgment interprets the evidence after the checklist is applied | Judgment may appear before the evidence is fully reviewed |

| Main risk | The rule becomes stale, too rigid, or falsely precise | The decision changes with mood, narrative, or recent price movement |

The point is not that rules are always better than discretion. The point is that rules make the decision process inspectable. If the rule is weak, stale, or poorly designed, the investor can revise the process instead of pretending the process was objective.

Where rules-based investing can fail

Rules can improve the consistency of review, but they can also create their own mistakes. A rule that looks disciplined on paper may still fail if the inputs are weak, the context has changed, or the investor treats the rule as proof instead of as a review tool.

| Failure condition | How it shows up | How to control it |

|---|---|---|

| Stale rule | The rule was built for a prior environment and no longer matches the business, valuation, or risk context. | Review the rule itself when the evidence environment changes, not only the investment. |

| Weak input quality | The checklist is followed, but the evidence inside it is shallow, outdated, or narrative-driven. | Define what qualifies as acceptable evidence before the checklist is used. |

| Checklist bypass | The investor uses the rule only when it supports the preferred action. | Require the same review sequence for adding, trimming, holding, and exiting. |

| False precision | The rule uses numbers or thresholds that look objective but do not reflect the real uncertainty of the thesis. | Treat thresholds as review prompts, not as automatic conclusions. |

| Overfitting | The rule is designed around a narrow past example and then applied too broadly. | Check whether the rule still makes sense across different business conditions and valuation environments. |

| Context blindness | The rule ignores changes in business quality, balance-sheet risk, capital allocation, or portfolio concentration. | Include context checks instead of relying on one isolated metric. |

| Rule confidence | The investor becomes confident in the process and stops checking whether the process is still valid. | Watch for overconfidence in the rule, especially after a few decisions appear to work. |

Illustrative scenario: when a rule slows the decision

An investor owns a company after building a thesis around durable revenue, improving margins, and a valuation that seemed reasonable under conservative assumptions. A sharp price decline creates urgency. The investor feels pressure to act immediately, either to reduce discomfort or to prove the original thesis was right.

A rules-based process changes the sequence. Before any portfolio action, the investor checks whether the business evidence has changed, whether valuation now offers more or less margin of safety, whether the original risk boundary has been crossed, whether contrary evidence has strengthened, and whether the position still fits the portfolio.

The checklist does not decide whether the investor should add, hold, reduce, or exit. It only prevents the decision from being made before the evidence is reviewed. That is the practical value of the rule: it protects the review threshold without pretending to know the outcome.

What rules-based investing does not mean

Rules-based investing does not mean replacing analysis with a formula. It does not mean every decision can be reduced to one ratio, one signal, one backtest, or one line in a checklist. It also does not mean the investor should ignore judgment when the evidence is incomplete.

A better boundary is this: rules should decide the order of review, not the conclusion by themselves. If a rule prevents thesis review, valuation review, risk review, or contrary-evidence review, it is not protecting the investor from bias. It is creating a new blind spot.

How this fits inside decision discipline

Rules-based investing is one part of a broader disciplined investment process. It is narrower than investment discipline as a whole because it focuses on predefined review criteria. It is also narrower than emotional investing because it does not explain every emotional trigger; it gives the investor a way to keep the evidence review from changing after the trigger appears.

The cleanest version is simple: write the rule before the pressure appears, use the rule to review evidence in the same order, and revise the rule only when the process itself has been reviewed. That keeps the rule useful without turning it into a prediction engine.

Rules-based investing FAQ

Is rules-based investing the same as systematic trading?

No. Rules-based investing here refers to an investor evidence-review process. It is not a short-term trading system, market-timing model, or signal engine.

Can rules-based investing remove emotion from decisions?

No. Rules can help slow review drift when emotion appears, but they do not remove emotion or guarantee objective decisions.

When should an investor revise the rules?

Rules should be revised when the process is reviewed, not during the moment when the investor is trying to justify an urgent decision.