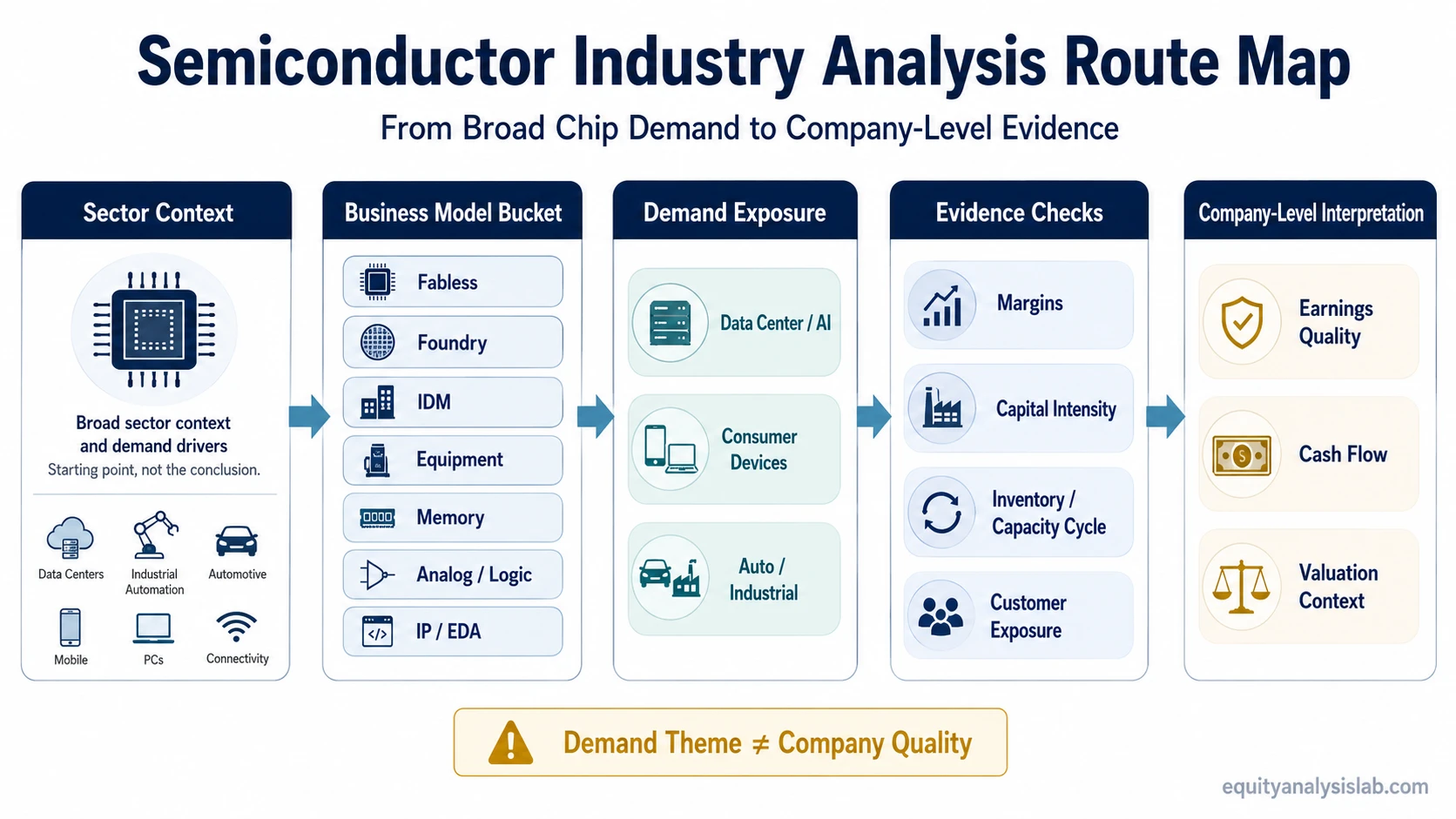

Semiconductor industry analysis separates broad chip demand from the business-model, margin, capacity, cycle and valuation evidence that matters for individual companies.

Chip companies can look similar from a distance, but their economics differ sharply depending on whether they design chips, manufacture them, sell equipment, supply memory, license IP or serve specialized end markets.

The useful output is not an industry forecast. It is a clearer set of company-level evidence questions before any investor judges business quality, earnings durability or valuation context.

Key Points

- Semiconductor industry analysis is an investor lens, not a stock recommendation.

- Semiconductor companies can have very different economics even when they benefit from the same broad demand theme.

- Demand growth should be checked against margins, capacity needs, cyclicality, customer exposure and valuation context.

- The useful outcome is a clearer company-level research path, not a single sector ranking.

What Semiconductor Industry Analysis Means for Investors

Semiconductor industry analysis starts with the sector, but it should not stop at the sector. The stronger question is how chip demand reaches a specific company, what that company must spend to serve demand, how margins are earned and which risks can change the interpretation.

The same broad theme can affect several types of semiconductor businesses in different ways. A company that designs chips, a company that manufactures chips, a company that sells manufacturing equipment and a company exposed to memory pricing may all sit inside the semiconductor industry, but they do not convert demand into revenue and cash flow in the same way.

Industry structure gives context. Company-level evidence determines whether that context supports durable earnings quality, margin resilience, cash generation and valuation discipline.

Why the Semiconductor Industry Is Not One Business Model

The semiconductor value chain includes design, manufacturing, equipment, software, intellectual property, materials, testing, packaging and distribution. Each layer has a different economic profile.

Fabless chip designers may depend more on product cycles, design wins, software ecosystems and access to manufacturing partners. Foundries and integrated manufacturers carry heavier fixed-asset exposure, which makes capacity planning and utilization more important. Equipment suppliers may benefit from factory buildouts, but their revenue can become cyclical when customers slow capital spending.

Memory companies often face more commodity-like pricing cycles than highly specialized analog or logic companies. EDA and IP businesses can have more recurring or design-cycle-linked economics, but they still depend on the pace of semiconductor design activity. These differences are why a broad semiconductor outlook is only a starting point.

The Main Semiconductor Business Model Buckets

A useful semiconductor industry analysis separates business models before comparing margins, growth rates or valuation multiples. The table groups the main buckets by the evidence an investor should examine.

| Business model bucket | What to examine | Investor evidence to look for |

|---|---|---|

| Fabless chip design | Product demand, design wins, customer mix, product roadmaps and access to manufacturing capacity. | Revenue concentration, gross margin stability, research intensity, customer adoption and dependence on external foundries. |

| Foundry | Manufacturing scale, utilization, process leadership, customer commitments and capacity expansion. | Utilization trends, capital spending needs, pricing discipline, depreciation burden and long-term customer relationships. |

| Integrated device manufacturer | Design and manufacturing together, including internal product cycles and factory economics. | Manufacturing efficiency, product competitiveness, inventory cycles, margin spread by segment and reinvestment discipline. |

| Memory | Supply-demand balance, pricing cycles, inventory corrections and capital spending discipline. | Average selling price pressure, inventory levels, cycle timing, balance-sheet resilience and cash flow through downturns. |

| Equipment and process tools | Factory buildouts, process transitions, customer capex cycles and tool demand. | Order patterns, backlog quality, customer concentration, service revenue and exposure to wafer-fab spending cycles. |

| Analog, mixed signal and specialty chips | End-market diversity, product lifespan, industrial exposure and customer relationships. | Margin durability, product stickiness, distribution channel health and evidence of pricing power. |

| EDA, IP and design infrastructure | Design activity, software workflows, licensing models and customer dependence. | Recurring revenue quality, renewal behavior, design-start activity, switching costs and margin structure. |

Demand Drivers Investors Should Separate

Semiconductor demand is not one demand stream. Data centers, AI infrastructure, automotive electronics, smartphones, industrial automation, consumer devices, telecom infrastructure and government-linked supply-chain projects can move at different speeds.

AI and data-center demand can raise attention on advanced logic, memory bandwidth, networking and power-management needs. That does not mean every semiconductor company receives the same benefit. The relevant question is whether the company has direct exposure, durable customer demand, margin capture and enough supply-chain access to convert the theme into financial results.

Automotive and industrial demand may be slower moving, but product lifecycles can be longer. Smartphone and consumer electronics exposure can be more sensitive to replacement cycles and inventory corrections. Telecom and infrastructure demand may depend on carrier spending cycles and policy-linked buildouts.

A clean demand review separates end-market growth from company economics. A demand narrative needs earnings quality and cash-flow support before it becomes useful for company analysis.

The Evidence That Matters at Company Level

After the broad industry read, the next step is to map sector evidence into specific company questions. That is where semiconductor industry analysis becomes more useful than a headline outlook.

| Evidence category | Question to ask | Why it matters |

|---|---|---|

| Revenue driver | Which end markets, products or customers explain growth? | Broad sector demand is less useful unless it connects to the company’s actual revenue base. |

| Margin driver | Are margins driven by product mix, utilization, pricing, software attachment, scale or cycle timing? | The same revenue growth can produce very different profit outcomes. |

| Capital needs | How much reinvestment is required to maintain or expand the business? | A more capital-intensive model can turn growth into large funding and depreciation requirements. |

| Fixed-cost exposure | What happens to margins when capacity utilization rises or falls? | Factory-heavy and equipment-linked businesses can show powerful margin changes when volume shifts through fixed costs. |

| Customer concentration | How dependent is the company on a small number of major customers? | A strong sector theme can still be fragile if customer concentration increases revenue risk. |

| Inventory and capacity cycle | Are customers building inventory, drawing it down or delaying orders? | Semiconductor cycles often look better or worse depending on where inventory sits in the chain. |

| Cash conversion | Does accounting profit convert into operating cash flow and free cash flow? | Growth narratives are weaker when working capital, capex or inventory absorb too much cash. |

| Management decisions | How does management handle reinvestment, buybacks, acquisitions, debt and cycle timing? | capital allocation can determine whether industry tailwinds become per-share value or diluted growth. |

| Valuation context | Does the valuation assume durable growth, peak-cycle margins or temporary demand strength? | Revenue-based valuation can look different once margins, reinvestment needs and cycle risk are considered. |

A Simple Investor Scenario

Consider two unnamed semiconductor companies exposed to the same broad demand theme. One designs chips and outsources manufacturing. The other owns manufacturing capacity and must keep expensive facilities utilized. The first may be judged more on product adoption, gross margin durability and customer concentration. The second may require closer attention to utilization, depreciation, capex and cycle timing.

The point is not that one model is automatically better. The same demand theme can pass through different cost structures, cash-flow profiles and risk points. Stronger analysis starts with the sector theme, then tests how the theme appears inside each company’s economics.

Common Beginner Mistakes in Semiconductor Industry Analysis

Assuming sector growth proves company quality: A growing end market can still leave some companies with weak margins, high reinvestment needs or poor cash conversion.

Treating all semiconductor companies the same: A memory producer, foundry, fabless designer, equipment supplier and analog company may respond differently to the same cycle.

Using one valuation multiple for the whole sector: A high-growth design company and a cyclical manufacturer may require different valuation interpretation. A revenue multiple such as EV/Revenue can be incomplete without margin, cash-flow and reinvestment context.

Overweighting AI headlines: AI and data-center demand can be important, but it does not remove inventory risk, export restrictions, capacity constraints, customer concentration or valuation risk.

Ignoring fixed-cost behavior: Factory utilization and equipment demand can create large profit swings. Semiconductor analysis should check how revenue changes flow through costs, margins and fixed-cost leverage.

Which Company-Level Evidence to Check Next

Semiconductor industry analysis becomes more useful when broad sector observations are tested against narrower company-level evidence. The table shows how to move from a sector signal to a more precise research question.

| If the sector observation is… | Then examine… | What the answer should clarify |

|---|---|---|

| Demand is rising in a specific end market. | Revenue source, customer mix and product exposure. | Whether the company actually participates in that demand stream. |

| Margins are expanding or compressing. | Product mix, utilization, pricing, input costs and competitive pressure. | Whether margin movement is structural, cyclical or temporary. |

| Capacity is being added across the industry. | Capital spending, depreciation, utilization risk and financing needs. | Whether growth requires heavy reinvestment before shareholders benefit. |

| A company trades at a premium valuation. | Growth durability, margin structure, cash conversion and cycle exposure. | Whether the premium depends on realistic company-level evidence. |

| The company has strong current fundamentals. | Forward risk, customer concentration, inventory position and valuation assumptions. | Whether current strength is already reflected or vulnerable to reversal. |

Limits of Semiconductor Industry Analysis

Semiconductor industry analysis does not prove that a stock is attractive, safe or undervalued. It provides context for more focused company research.

Industry growth can be offset by overcapacity, weak pricing, export restrictions, customer concentration, inventory corrections, high capital spending, dilution, debt or valuation expectations that already assume strong future results.

The safest interpretation is conditional: a sector tailwind becomes useful only when company-level evidence supports the thesis. Revenue growth, margin durability, cash conversion, reinvestment needs and valuation assumptions still need to be tested separately.

FAQ

What is semiconductor industry analysis?

Semiconductor industry analysis is the process of studying chip demand, business models, value-chain position, margin drivers, capital needs, cyclicality and risks so an investor can evaluate individual semiconductor companies more clearly.

Why are semiconductor companies analyzed differently from each other?

They can sit in different parts of the value chain. Fabless designers, foundries, memory producers, equipment suppliers, analog companies and EDA/IP businesses often have different margin structures, capital requirements and cycle exposure.

Does strong semiconductor demand make every chip company attractive?

No. Demand is only one input. The company still needs to show relevant exposure, durable margins, sound cash conversion, manageable reinvestment needs and valuation assumptions that do not already price in too much optimism.

What is the biggest mistake in semiconductor industry analysis?

A common mistake is treating the sector as one business model. Semiconductor companies can benefit from the same broad theme but produce very different financial outcomes because of cost structure, capacity needs, pricing power and customer exposure.