Valuation examples show how different methods turn company data into an estimated value. The useful starting point is not one universal formula, but the type of valuation question being asked: whole-company value, cash-flow assumptions, peer multiples, or method comparison.

A company can look different under each method because every valuation example depends on inputs. Revenue growth, margins, free cash flow, discount rate, terminal value, balance-sheet adjustments and peer selection can all change the estimate. The example is useful only when those assumptions are visible.

What valuation examples are used for

Valuation examples are used to show how raw business information becomes an estimate of value. They can clarify which numbers matter, how the method works, and where judgment enters the process.

Price is the market quote, value is the estimate the method tries to support, and the gap between them depends on the assumptions used.

They should not be treated as proof of a company’s exact worth. A clean model can still be fragile if its growth rate, margin forecast, terminal value or peer group is weak. For investors, the main benefit is seeing how the estimate is built and where it can break.

Core distinction: a valuation example explains a method and its assumptions. It does not automatically produce a reliable investment conclusion, target price or buy/sell decision.

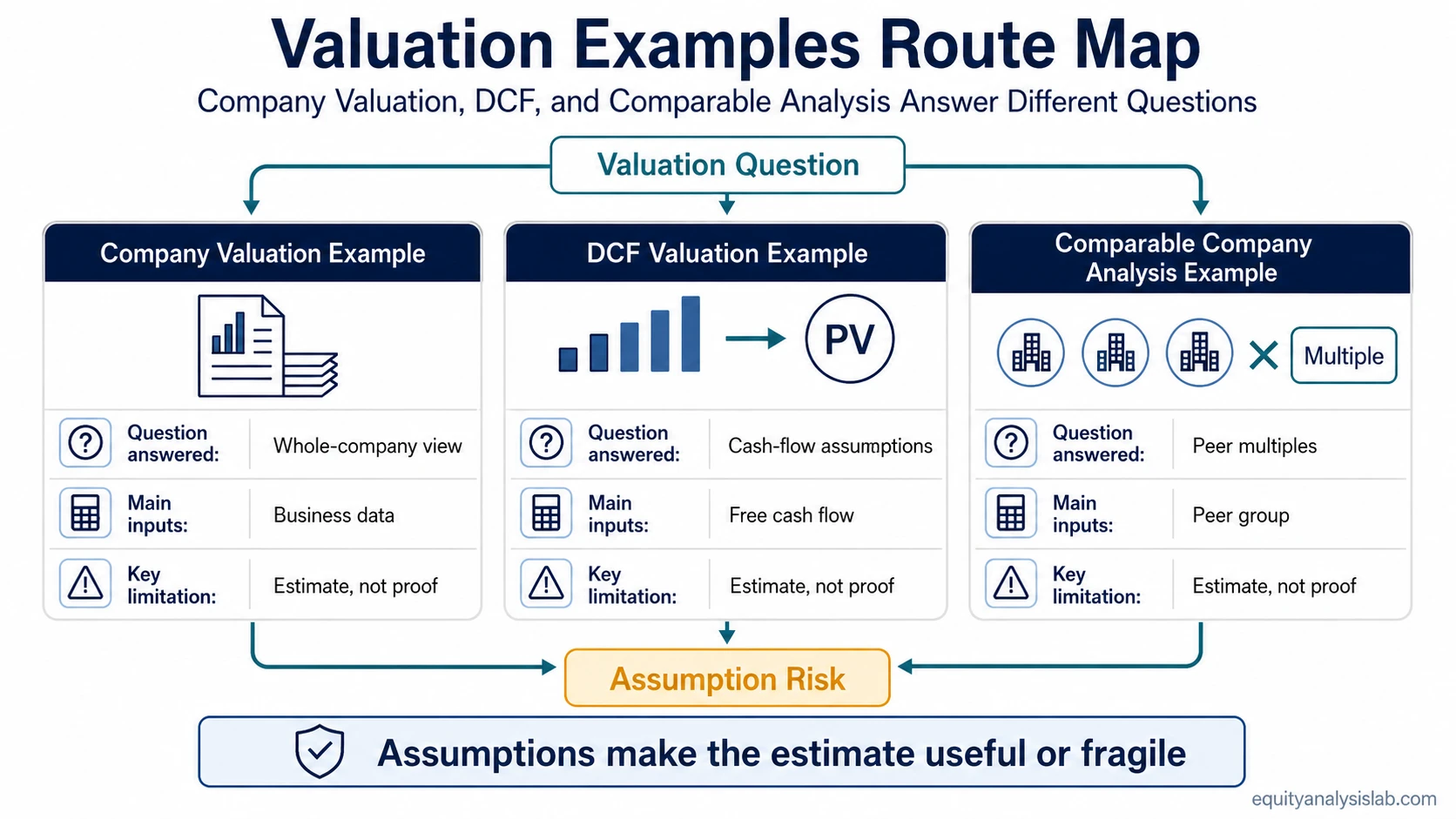

Which valuation example should you start with?

The best starting point depends on the question. A full company example helps when the main issue is the overall valuation process. A DCF example is better when the main issue is cash-flow forecasting. A comparable-company example is better when the question is relative value versus peers.

| If your question is… | Start with… | What it clarifies | What it does not solve |

|---|---|---|---|

| How do investors move from company data to an estimated value? | company valuation example | The overall path from business data, financial statements and assumptions to a valuation view. | It does not isolate every DCF input or build a full peer-comparison model. |

| How do cash-flow forecasts, discount rates and terminal value affect the estimate? | DCF valuation example | The cash-flow-based path where assumptions drive most of the result. | It does not prove the estimate is correct if the forecasts are weak. |

| How does one company compare with similar public companies? | comparable company analysis example | The relative-valuation path using peer multiples and market comparisons. | It does not work well if the peer group is not genuinely comparable. |

| Why do two valuation methods give different answers? | Method comparison and assumption sensitivity | How input choices, business quality, capital structure and market multiples change the output. | It does not remove the need to judge which assumptions are most defensible. |

Company valuation examples

Company valuation examples are useful when the question is broad: how a business is analyzed as a whole before an estimate is formed. This path usually connects revenue, margins, cash flow, balance-sheet context, growth assumptions and comparable market evidence.

The goal is not to compress every valuation method into one place. The goal is to show the workflow: what the company earns, how durable those earnings appear, how cash flows convert, how the balance sheet changes the picture, and which valuation method fits the business.

Use this path when: a whole-company view is needed before going into a single model.

Watch the limitation: a company-level example can become too broad if it hides the assumptions behind the estimate.

DCF valuation examples

A DCF valuation example focuses on estimated future cash flows. The method usually becomes sensitive to forecast growth, margins, reinvestment needs, discount rate and terminal value. Small changes in those inputs can create materially different outputs.

This makes DCF examples useful for learning how assumptions flow through a valuation. It also makes them easy to misuse. A precise spreadsheet can still rest on uncertain forecasts, especially when most of the estimate comes from the terminal value rather than near-term cash flows.

DCF limitation: the model can look mathematically clean while depending heavily on assumptions that are difficult to know in advance.

Comparable company analysis examples

Comparable company analysis examples use market multiples from similar companies to frame relative value. The method can be useful when peer companies have similar business models, growth profiles, margins, capital intensity and risk characteristics.

The main risk is weak peer selection. If a company is compared with peers that have different economics, leverage, growth durability or accounting quality, the multiple may create a misleading shortcut rather than a useful valuation reference.

Use this path when: the valuation question depends on how the market prices similar companies.

Watch the limitation: a multiple is only as useful as the peer group and the metric behind it.

Why valuation examples can give different answers

Different valuation examples can produce different estimates because they answer different questions. A DCF model asks what future cash flows may be worth today. A comparable-company analysis asks how similar public companies are priced. A company valuation example may combine several views to understand the business from more than one angle.

The gap between methods is not automatically an error. It can reveal where the judgment sits. The important step is to identify which assumption is doing the most work.

| Input or judgment | How it changes the valuation example |

|---|---|

| Revenue growth | Higher or lower growth expectations can change future cash-flow estimates and market multiple interpretation. |

| Margins | Margin assumptions affect whether revenue growth converts into earnings and free cash flow. |

| Discount rate | A higher discount rate reduces the present value of future cash flows in a DCF framework. |

| Terminal value | Terminal value can dominate a DCF estimate if the model places too much weight on distant cash flows. |

| Peer group | Comparable-company analysis can mislead if the selected peers do not share similar economics or risk. |

| Balance-sheet context | Debt, cash, dilution and other claims can change the value available to common shareholders. |

Scope limits for valuation examples

Valuation examples in this context stay focused on investor and company-analysis questions. They do not address property appraisal, real-estate valuation, private business-sale advisory work, tax appraisal, legal valuation disputes, or professional appraisal reports.

They also do not provide target prices, buy/sell recommendations, return forecasts, full spreadsheet templates, or claims that one method reveals the exact true value of a company. The safer use is to inspect assumptions, compare methods and choose the valuation example that fits the question.

Next step: choose the company valuation path for a whole-business workflow, the DCF path for cash-flow assumptions, or the comparable-company path for peer-multiple analysis.

Valuation examples FAQ

What are valuation examples?

Valuation examples show how a valuation method turns company data into an estimated value. They usually clarify the method, inputs, assumptions and limitations behind the estimate.

Which valuation example should I start with?

Start with the example that matches the question. Use a company valuation example for the full workflow, a DCF example for cash-flow assumptions, and a comparable-company analysis example for peer multiple comparisons.

Why can DCF and comparable-company analysis give different values?

DCF depends on forecast cash flows, discount rate and terminal value. Comparable-company analysis depends on peer selection and market multiples. Because the inputs are different, the estimates can differ.

Does a valuation example prove what a company is worth?

No. A valuation example shows how an estimate is constructed. It does not prove exact value, remove uncertainty, or replace judgment about assumptions, business quality and risk.