Adding to a stock position means increasing an ownership stake after the stock is already in the portfolio. The decision is not justified only because the price is up, down, near a high, below a prior purchase price, or moving without the investor. It becomes more defensible when the thesis remains intact or stronger, valuation still supports the expected return, risk remains controlled, and the added capital improves the portfolio rather than magnifying emotion.

The useful question is not whether the stock has moved enough. The useful question is whether the forward case for owning more is stronger than the case for leaving the position unchanged.

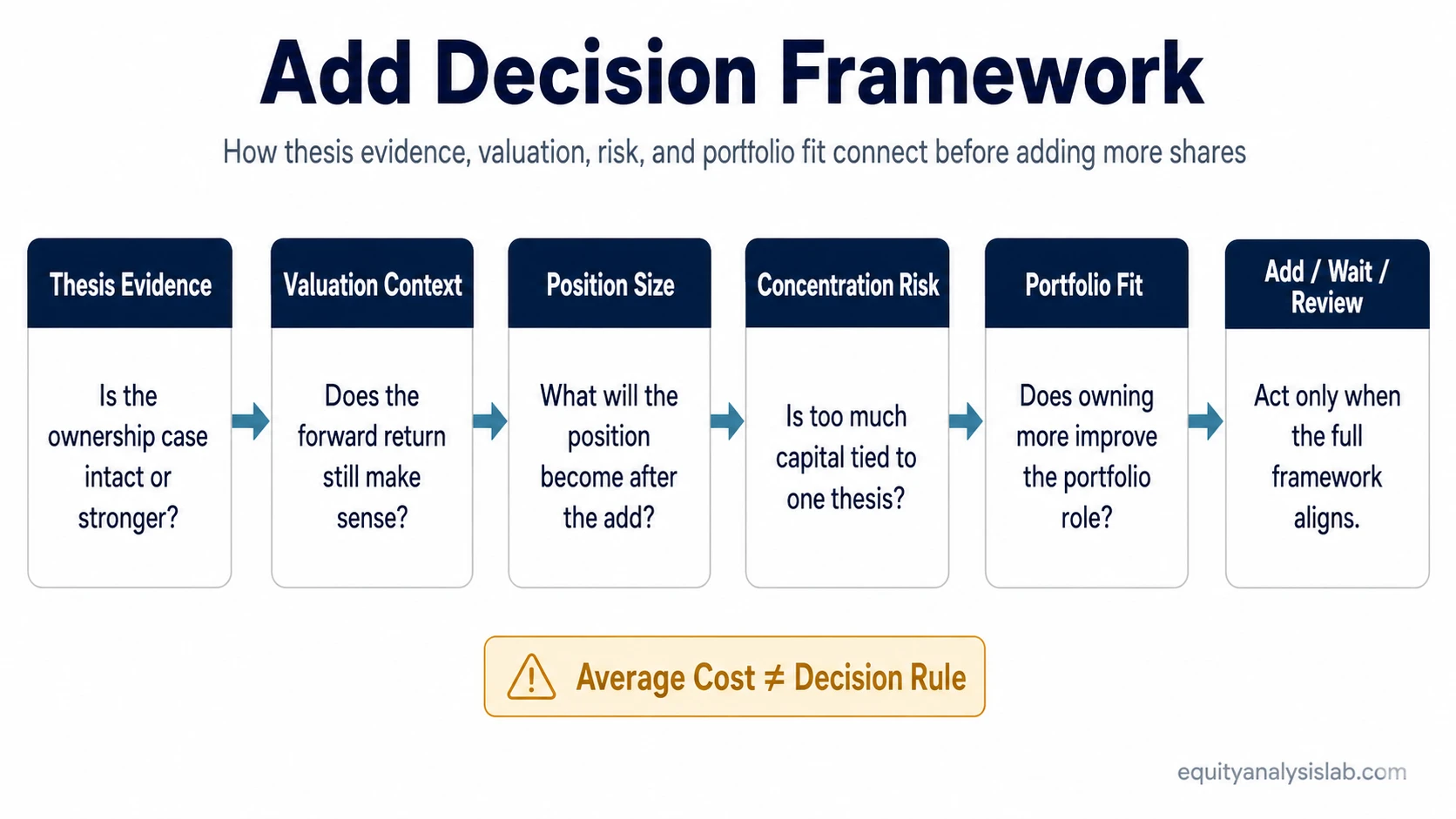

Key Points Before Adding More Shares

- Adding is a forward-looking decision, not a reward for being right or a repair tool for being wrong.

- The original thesis should still be valid, and new evidence should not weaken the reason for ownership.

- Valuation matters because a better business outlook can offset a higher price, while a lower price can still be unattractive if fundamentals deteriorate.

- Position size and concentration should be checked before more capital is committed.

- Average cost is accounting history. Thesis quality, valuation, risk, and portfolio fit should drive the decision.

What It Means to Add to a Stock Position

To add to a stock position is to buy additional shares after an investor already owns the company. That makes it different from the first purchase. The investor is no longer deciding whether the stock deserves a place in the portfolio; the investor is deciding whether the stock deserves a larger role than it already has.

That distinction changes the review. A first purchase asks whether the company, valuation, risk, and portfolio role are attractive enough to begin ownership. An add decision asks whether the existing ownership case has improved enough, or remained attractive enough, to justify increasing exposure.

It should also be separated from short-term trading scale-in mechanics. Adding to an investment position is not about entries, exits, stops, or intraday execution. It is a capital-allocation decision inside an existing portfolio.

The Core Framework for Adding to an Existing Position

An add decision works best when several conditions align at the same time. A stronger thesis with weaker valuation may not be enough. Better valuation with a weaker business case may not be enough. A high-conviction company can still become too large if one position starts controlling portfolio risk.

| Decision check | What it asks | Add becomes more defensible when | Add weakens when |

|---|---|---|---|

| Thesis evidence | Is the reason for ownership still valid? | Business drivers, financial evidence, and competitive position remain aligned with the original case or have improved. | New evidence weakens the business case, reduces confidence in the thesis, or changes the reason for owning the stock. |

| Valuation context | Does the forward return still make sense? | Earnings, cash flow, or business quality expectations support the price being paid for additional shares. | The stock price has risen faster than the business value, or the lower price reflects deteriorating fundamentals. |

| Risk and downside | What happens if the thesis is wrong? | Downside remains tolerable after the add, and the risk is not hidden by recent price strength. | The position would create an unacceptable loss if the thesis breaks or expectations reset. |

| Position size | How large will the position become? | The post-add weight still fits the investor’s planned size boundary. | The add turns a reasonable position into a portfolio-dominating exposure. |

| Concentration | Is one thesis becoming too important? | The portfolio can absorb company-specific disappointment without one stock controlling total results. | The addition increases company-specific exposure beyond the investor’s comfort or process. |

| Portfolio role | Does owning more improve the portfolio? | The larger stake strengthens the portfolio’s intended exposure without duplicating risk already held elsewhere. | The add mainly increases the same risk already present in related holdings. |

| Discipline and emotion | Is the decision driven by evidence or feeling? | The choice follows a consistent process, not FOMO, regret, or anchoring. | The investor is reacting to a recent move, trying to protect average cost, or trying to force confidence back into a weakened idea. |

Thesis Evidence Comes Before Price Movement

Adding to a position should reaffirm the investment thesis. The reason to own more should be stronger than “the stock went up” or “the stock got cheaper.” Price movement can create urgency, but it does not confirm business quality by itself.

A stronger add case usually starts with evidence that the original thesis still works. Revenue drivers may be tracking as expected. Margins may be stabilizing. Free cash flow may be improving. Balance-sheet risk may be lower than feared. Management execution may be more consistent than the market previously assumed.

The opposite also matters. If the company’s competitive position is weakening, financial quality is deteriorating, or the original reason for ownership no longer holds, a lower price does not automatically create a better opportunity. It may simply reflect a weaker case.

Valuation Can Improve or Worsen After the Stock Moves

A common mistake is treating price movement as the whole valuation story. A stock can rise and still become more attractive if the business outlook improves faster than the share price. A stock can fall and still become less attractive if earnings quality, cash flow durability, or balance-sheet strength deteriorates faster than the price.

The valuation check does not need to become a full model every time. The investor still needs to ask whether the new purchase price leaves enough expected return for the risks being taken. That requires comparing the price with updated expectations, not with the investor’s original purchase price.

When valuation is unclear, adding usually deserves more caution. Unclear valuation does not mean the stock must be avoided, but it weakens the case for increasing exposure before the thesis and expected return are better defined.

Illustrative Example: Price Up, But Two Different Add Cases

Consider a stock that has risen since the first purchase. In one scenario, the price is higher, but earnings expectations, cash-flow quality, and business visibility have improved even more. The position may still deserve review for a possible add because the forward value case may have improved.

In a second scenario, the price is higher mainly because sentiment expanded while the business evidence stayed flat. The investor may feel pressure to add because the stock is “working,” but the expected return may be weaker than it was before.

The same price direction can produce different conclusions. The stronger case depends on updated thesis quality and valuation context, not on the fact that the stock has already gone up.

Average Cost Should Not Control the Add Decision

Average cost is accounting history. It records where earlier shares were bought. It does not determine whether additional shares offer an attractive forward return.

This matters because many add decisions are distorted by anchoring. An investor may avoid adding to a strong company because the new shares would raise the average cost. Another investor may add after a decline because the lower price feels like a discount to the original purchase. Both reactions can be incomplete.

Raising the average cost can be acceptable if the thesis has improved, valuation remains reasonable, and the position still fits the portfolio. Lowering the average cost can be risky if the thesis has weakened or the position is already too large.

Should You Wait for a Dip Before Adding?

Waiting for a pullback can be reasonable when valuation is stretched, uncertainty is high, or the position is already large enough. But waiting for a dip is not a complete decision process. A pullback only matters if the business case remains intact and the lower price improves the forward return.

A dip can also be a warning. If the price falls because new information weakens the thesis, the lower price may not improve the add case. It may reveal that the previous assumptions were too optimistic.

The cleaner distinction is confirmation versus price comfort. Adding after confirmation can feel uncomfortable because the stock may already be higher. Adding after a dip can feel safer because the price is lower. Neither is automatically better. The add becomes more defensible when evidence, valuation, risk, and portfolio fit align.

Position Size and Concentration Set the Boundary

A strong thesis can still become a weak portfolio decision if the position becomes too large. The post-add weight matters because every additional share increases exposure to the same company-specific risks.

The portfolio-fit test is simple in concept: after the add, the investor should know how much of the portfolio depends on this company, what downside would mean for total capital, and whether the same business or sector exposure already appears elsewhere. A clear position sizing boundary keeps the add decision from becoming open-ended.

Concentration is not automatically wrong. Some investors intentionally hold concentrated portfolios. The risk appears when position size grows without a clear boundary, when conviction is treated as a substitute for downside review, or when one thesis begins to dominate decisions that should remain portfolio-level decisions.

Common Mistakes When Adding to a Position

- Adding only because the stock is down: a lower price helps only if the thesis remains valid and valuation improves relative to the updated facts.

- Adding only because the stock is up: momentum in the position can create confidence, but price strength does not prove that the forward return is still attractive.

- Protecting average cost: refusing to add only because it raises the average cost can make accounting history more important than expected return.

- Ignoring concentration: a good company can still become too much of the portfolio if the add pushes exposure beyond the investor’s process.

- Treating a pullback as proof of opportunity: a lower price needs context. The reason for the decline matters.

- Treating a winner as automatically safer: a rising stock can become more expensive, more crowded, or more dependent on high expectations.

When Not to Add to a Stock Position

Not adding can be the disciplined choice when the evidence is mixed. A sound investment discipline should prevent more capital from being used to repair a weak thesis, chase a recent move, or increase exposure before the investor understands what changed.

- The original thesis has weakened or no longer explains the business.

- Valuation no longer supports the expected return.

- The position is already large enough for the investor’s risk limits.

- The decision is driven by FOMO, regret, or fear of missing a move.

- The investor is averaging down to avoid admitting that the original thesis may be wrong.

- The risk/reward has deteriorated even though the stock remains popular.

- New information creates uncertainty that deserves review before more capital is committed.

Add, Wait, or Review

The decision does not need to end in a yes-or-no answer. A disciplined process can produce three different outcomes.

Add: the thesis remains strong, valuation still supports the expected return, the position remains within planned size, concentration risk is acceptable, and the larger stake improves portfolio quality.

Wait: the company remains attractive, but valuation, uncertainty, or current position size does not justify committing more capital yet.

Review: the thesis, valuation, or risk profile has changed enough that the investor should reassess the position before deciding whether to add, hold, reduce, or exit.

FAQ

Is it better to add after a pullback or after confirmation?

Neither is automatically better. A pullback can improve valuation if the thesis remains intact, but it can also reflect new risk. Confirmation can make the thesis clearer, but the higher price may reduce expected return. The better add case depends on thesis quality, valuation, risk, and portfolio fit together.

Is averaging up a mistake?

Averaging up is not automatically a mistake. It can be reasonable when the business case has improved, valuation still supports the expected return, and the larger position remains controlled. It becomes weaker when the investor adds only because the stock has risen.

Should average cost affect the decision to add?

Average cost should not be the decision center. It can help track past purchases, but the add decision should focus on forward expected return, thesis quality, valuation, risk, position size, and portfolio fit.

When should an investor not add to a winning stock?

An investor should be cautious about adding to a winning stock when valuation has become stretched, the thesis is less clear, the position is already large, or the decision is driven mainly by FOMO. A winning stock is not automatically safer just because earlier shares performed well.