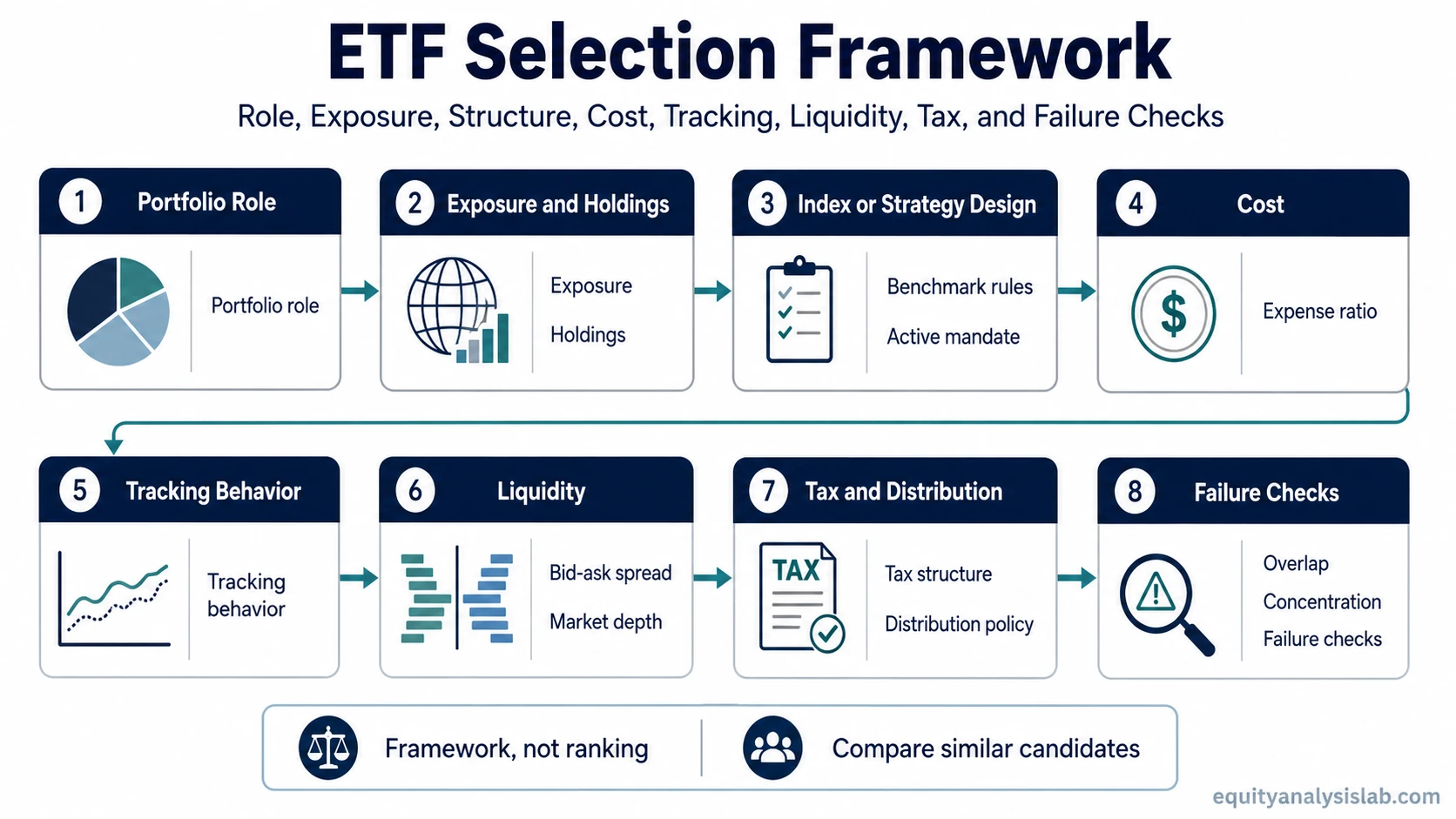

Choosing an ETF starts with the role the fund is meant to play, then moves through exposure, index or strategy design, cost, tracking behavior, liquidity, tax and distribution mechanics, and failure checks that can weaken an otherwise reasonable comparison.

A useful ETF selection process does not begin with the cheapest fund, the largest fund, or the fund with the strongest recent return. It begins with a specific portfolio job: broad market exposure, sector exposure, income exposure, factor exposure, inflation-sensitive exposure, currency-adjusted exposure, or another clearly defined role.

Framework: Choose an ETF by checking whether the fund gives the intended exposure, whether its structure supports that exposure, whether cost and tracking are acceptable for the role, whether liquidity is sufficient, and whether tax or distribution mechanics change the practical result.

Key Points

- ETF selection should start with portfolio role and exposure, not with recent performance or a product label.

- Holdings, benchmark rules, active or passive mandate, and concentration explain what the fund actually owns or follows.

- Cost, tracking behavior, liquidity, and tax mechanics can change the practical comparison between similar funds.

- A low fee or large asset base does not automatically make one ETF stronger if exposure, tracking, spreads, or account-level tax fit are weaker.

- The selection case weakens when the ETF’s role inside the portfolio cannot be explained clearly.

ETF Selection Framework

An ETF selection framework works best as a sequence, not as a single score. Each layer answers a different question: what the fund is supposed to do, what it actually holds, how it follows its benchmark or strategy, what it costs, how easily it trades, and what structural details can affect the investor’s result.

Selection sequence: portfolio role → exposure and holdings → index or strategy design → cost → tracking behavior → liquidity → tax and distribution constraints → failure conditions.

A fund can look attractive on one layer and still be weaker on another layer. A broad-market ETF may be low cost but concentrated in a few large holdings. A thematic ETF may match a narrative but hold companies with different business drivers. An income ETF may offer distributions but create tax or reinvestment questions that need separate review.

Start With Portfolio Role and Exposure

The first test is whether the ETF has a clear job. A fund used for core equity exposure should be judged differently from a fund used for a satellite sector tilt, income sleeve, commodity exposure, currency-hedged allocation, or factor strategy.

Exposure begins with the holdings, not the fund name. The same label can hide different weights, regional exposure, sector concentration, currency exposure, security-selection rules, or derivative use. The investor should check whether the holdings match the intended role and whether any concentration is acceptable for that role.

Passive funds often follow an index, so the benchmark rules matter. An index ETF should be evaluated through the index it tracks, the weighting method it uses, and the exposure that benchmark creates.

Active ETFs require a different review because the manager has more discretion. The relevant question is not only what the fund owns today, but how the mandate permits the portfolio to change. Active design can be useful in some contexts, but it also makes manager process, turnover, and portfolio discipline more important.

| Exposure question | What to check | Why it matters |

|---|---|---|

| Portfolio role | Core holding, satellite tilt, income sleeve, hedge, factor exposure, or thematic allocation | The same ETF can be reasonable for one role and less appropriate for another role. |

| Holdings | Top positions, sector weights, country weights, currency exposure, and concentration | The product label can be too broad to reveal the actual economic exposure. |

| Benchmark or mandate | Index rules, active mandate, rebalancing method, screening rules, and exclusions | The fund’s behavior depends on the rules behind the portfolio, not only the ETF name. |

| Overlap | Duplicate exposure with existing holdings or other ETFs | A new ETF may add concentration rather than diversification if it repeats what is already owned. |

Check Cost, Tracking, and Liquidity Together

Cost matters, but it should not be isolated from tracking and trading friction. The ETF expense ratio is the recurring fund-level cost, yet the practical holding experience can also be affected by tracking behavior, spreads, market depth, and portfolio turnover.

Tracking behavior shows whether the ETF has followed the intended benchmark or strategy closely enough for the role. A fund with low headline cost may still disappoint if the benchmark relationship is unstable, especially when the investor expects tight index exposure.

A tracking review should include the fund’s benchmark relationship, the size and consistency of return differences, and the conditions under which deviations become larger. That is where benchmark deviation consistency becomes more useful than a simple recent-return comparison.

Liquidity affects the practical cost of entering, adding to, trimming, or exiting an ETF position. ETF liquidity should be checked through trading volume, bid-ask spread behavior, market depth, underlying holdings liquidity, and whether the fund usually trades close to its underlying value.

Cost layer: lower stated cost can help, but it is not enough by itself.

Tracking layer: the fund should behave consistently relative to the benchmark or strategy it is supposed to represent.

Liquidity layer: trading friction can matter when spreads widen, depth is thin, or the underlying holdings are harder to trade.

Review Structure, Tax, and Distribution Constraints

ETF structure can affect how the investor experiences the fund. Domicile, distribution policy, use of derivatives, securities lending, replication method, currency hedging, and account type can all change the practical result, even when two ETFs appear to cover the same market.

Tax and distribution details should be handled as constraints, not as universal ranking factors. A distributing ETF may suit one account or investor process, while an accumulating structure may suit another. Withholding tax, domicile, fund wrapper, and local tax treatment can matter, but exact outcomes depend on jurisdiction and account context.

The practical tax review should focus on whether the ETF structure creates avoidable friction for the intended role. A fund’s tax and distribution efficiency can change the comparison, but it should not be treated as legal or tax advice without jurisdiction-specific review.

Limitation: tax treatment is jurisdiction-specific. A general ETF framework can identify tax and distribution questions, but it cannot determine the final after-tax result for every investor, account type, or country.

ETF Selection Criteria Checklist

The checklist below organizes the main evidence layers without turning the process into a mechanical score. A strong ETF candidate should pass the layers that matter for its intended role, while any weak layer should be investigated before the fund is compared with alternatives.

| Selection layer | What to check | What can mislead | Related review area |

|---|---|---|---|

| Portfolio role | Core exposure, satellite exposure, income, hedge, factor tilt, or thematic use | A fund can look attractive without solving a defined portfolio need. | Investment objective and portfolio allocation review |

| Exposure and holdings | Underlying securities, weights, sectors, regions, currencies, and concentration | The ETF name may not reveal the dominant holdings or hidden overlap. | Holdings and exposure review |

| Index or strategy | Benchmark rules, active mandate, weighting method, rebalancing process, and selection rules | Two ETFs with similar labels may follow different rules. | Index or active mandate review |

| Cost | Expense ratio, turnover, and other fund-level costs where disclosed | The cheapest fund may not be the strongest match if tracking, exposure, or liquidity is weaker. | Cost and fee analysis |

| Tracking behavior | Return difference versus benchmark or stated strategy over multiple periods | Recent outperformance can hide an unstable benchmark relationship. | Tracking and benchmark behavior review |

| Liquidity | Bid-ask spreads, average volume, market depth, premium/discount behavior, and underlying holdings liquidity | Large assets or popular branding do not automatically guarantee tight trading conditions. | Liquidity and trading-friction review |

| Tax and distribution mechanics | Domicile, distribution policy, withholding-tax exposure, accumulation/distribution treatment, and account fit | Pre-tax comparisons can ignore after-tax or cash-flow differences. | Tax and distribution review |

| Failure conditions | Unclear role, hidden concentration, weak tracking, poor liquidity, tax mismatch, or unresolved overlap | A single strong feature can distract from a material weakness in another layer. | Full selection framework review |

Example of a Basic ETF Selection Reading

Two ETFs may both claim broad developed-market equity exposure. One has a lower expense ratio and larger asset base, but its top holdings are more concentrated than the label suggests and its spreads widen more noticeably outside normal conditions. The other costs slightly more, yet its benchmark captures a broader holdings set and its distribution policy fits the intended account use more cleanly.

The lower-cost ETF is not automatically weaker or stronger. If the portfolio job is low-cost exposure to the largest companies in the benchmark, it may still be a reasonable candidate. If the job is broader developed-market exposure with less concentration and more consistent trading conditions, the second fund may deserve closer review.

The diagnostic point is that cost answers only one part of the selection question. Exposure, benchmark design, tracking behavior, liquidity conditions, and tax or distribution mechanics need to be checked together before similar ETF candidates can be compared usefully.

What Weakens an ETF Selection Case

An ETF selection case weakens when one attractive feature hides an unresolved problem in the fund’s role, exposure, structure, tracking, liquidity, or tax treatment.

Common mistake: choosing the fund that looks cheapest or most popular before checking whether the ETF actually gives the intended exposure and whether its tracking, liquidity, and tax mechanics fit the role.

| Weakening condition | Why it matters | More useful review question |

|---|---|---|

| The ETF label hides different holdings | Similar product names can contain different sectors, countries, weights, or security types. | What economic exposure does the fund actually create? |

| Low cost is offset by tracking or spread issues | The stated fee is only one part of the practical holding cost. | Does the fund follow the intended benchmark closely enough after costs and trading friction? |

| Liquidity looks adequate but spreads or depth are weak | Trading volume alone may not show how easily shares can be traded under less stable conditions. | How do spreads, depth, and underlying holdings liquidity behave when conditions are less calm? |

| Tax or distribution mechanics conflict with account use | The pre-tax fund comparison may not match the investor’s practical outcome. | Do domicile, distributions, withholding, and account type change the comparison? |

| The portfolio role is unclear | A fund without a defined role can add overlap, concentration, or unnecessary complexity. | What problem does this ETF solve inside the portfolio? |

How to Compare Similar ETF Candidates

Once the framework removes funds that do not match the intended role, the remaining comparison becomes more useful. Similar ETF candidates can then be separated by exposure precision, benchmark design, cost level, tracking consistency, liquidity quality, tax structure, and whether the fund’s portfolio role can be stated clearly.

A practical comparison should avoid treating any single layer as decisive. Low cost helps only if the exposure is correct. Strong liquidity helps only if the fund holds the desired market. Tax efficiency helps only if the structure fits the investor’s account and jurisdiction. Tracking consistency helps only if the benchmark itself is the right benchmark for the portfolio role.

Selection boundary: ETF selection is a framework for narrowing and checking candidates. It does not prove that a fund will outperform, that a holding is suitable for every investor, or that one fund is the right choice in every account.

FAQ

What is the first thing to check when choosing an ETF?

The first check is the ETF’s intended portfolio role. The investor should know whether the fund is meant to provide core exposure, a satellite tilt, income, a hedge, a factor exposure, or another defined function before comparing fees or past performance.

Can a lower expense ratio settle the ETF choice?

No. A lower expense ratio can help, but exposure fit, tracking behavior, liquidity, tax structure, and portfolio role can change the comparison. A low-cost ETF can still be a weak match if it does not provide the intended exposure.

Should ETF selection be based on past performance?

Past performance should not be the main selection rule. It can provide context, but the more durable checks are exposure, benchmark or strategy design, cost, tracking behavior, liquidity, structure, and whether the fund fits a defined portfolio role.

When does an ETF selection case become weak?

The case weakens when the ETF’s role is unclear, the holdings do not match the label, the low fee is offset by tracking or trading friction, liquidity is shallow, or tax and distribution mechanics conflict with the intended use.