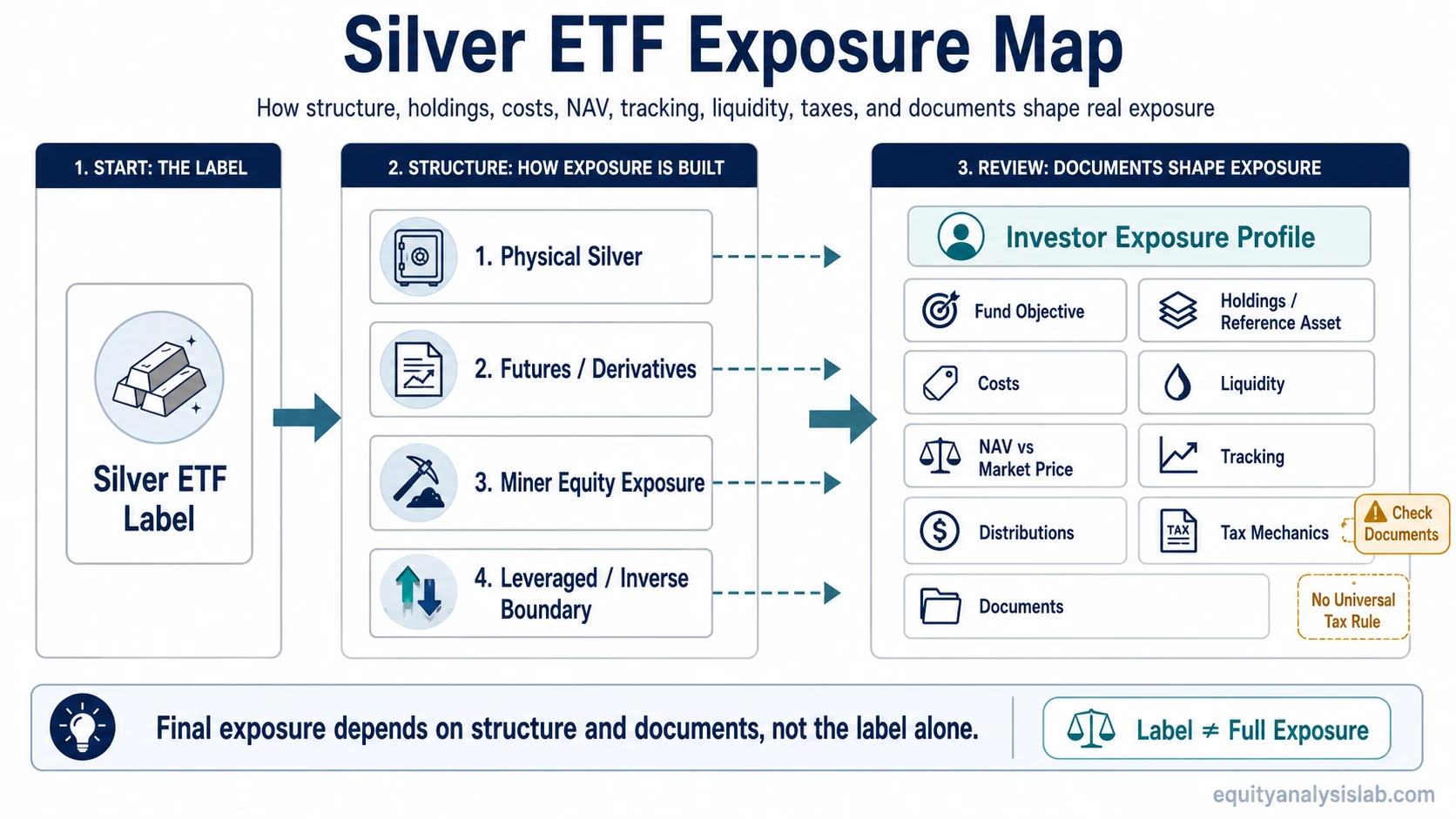

A silver ETF is not automatically the same practical thing as owning physical silver directly. It is an exchange-traded product that gives exposure to silver or silver-linked assets, while the actual investor experience depends on the fund’s structure, holdings or reference asset, costs, tracking behavior, liquidity, distributions, tax mechanics, and documents.

The useful starting point is the wrapper, not the label. Two products can both use “silver” in their name while giving different exposure through physical bullion, futures, derivatives, mining-company equities, leverage, inverse objectives, currency terms, or document-specific rules. That is why silver ETF analysis should begin with the objective and fund documents before moving to cost or comparison screens.

Key Points

- A silver ETF gives exchange-traded exposure to silver or silver-linked assets.

- The fund label does not fully define what the investor owns, tracks, or experiences.

- Structure, holdings, reference asset, fees, NAV and market price behavior, tracking, liquidity, distributions, taxes, and documents can all affect results.

- Silver ETF shares are not always equivalent to direct personal ownership or custody of physical silver.

- Product comparison should start with documents and exposure mechanics, not rankings.

What Is a Silver ETF?

Silver ETF definition: A silver ETF is an exchange-traded fund or exchange-traded product designed to give investors market exposure to silver, silver-linked instruments, or in some cases companies connected to silver production.

In a broad ETF taxonomy, a silver ETF usually sits inside precious-metals or commodity exposure. The important distinction is that the ETF share is the listed security the investor buys and sells. The underlying exposure may come from physical silver held by a trust or fund, futures contracts, derivatives, an index strategy, or equity exposure to silver-mining businesses, depending on the product.

This makes “is there a silver ETF?” an exposure question rather than a single-product question. Silver-linked exchange-traded products exist in many markets, but each product has its own objective, structure, trading venue, document set, fees, liquidity profile, and tax treatment. The label can identify the broad category, but it cannot replace the prospectus, factsheet, and issuer documents.

How Silver ETF Exposure Works

Silver ETF exposure can be built in several ways. A physically backed product may seek to reflect the price of silver bullion after expenses. A futures-linked or derivative-linked product may track contracts or instruments tied to silver prices. A mining-company product may behave more like an equity portfolio because operating costs, reserves, management, balance sheets, and equity-market conditions can affect returns.

Some silver-linked products also use specialized objectives. Leveraged products may target a multiple of daily silver-linked movement. Inverse products may target the opposite direction of a benchmark over a stated reset period. Those structures are not just “stronger” or “bearish” versions of a plain silver ETF; their documents define a different objective, compounding behavior, and risk profile.

Another boundary is active management. A passive silver product usually follows a stated index, trust objective, or reference asset. An actively managed ETF may give the manager discretion over portfolio construction, instrument selection, risk controls, or exposure changes. That distinction matters because the label may still mention silver while the process is not purely mechanical.

| Exposure route | What it usually means | Main document question |

|---|---|---|

| Physical silver exposure | The product is designed around silver bullion or silver held through a trust or fund structure. | What does the fund actually hold, and what rights do shareholders have? |

| Futures or derivative exposure | The product uses contracts or instruments linked to silver rather than simple personal bullion ownership. | How does the strategy handle roll costs, collateral, tracking, and reset rules? |

| Silver mining equity exposure | The product owns companies connected to silver production, so equity and business risks matter. | Is the investor buying silver price exposure or mining-company equity exposure? |

| Leveraged or inverse exposure | The product targets a stated multiple or opposite direction over a defined period. | What is the reset period, and how can compounding affect longer holding periods? |

Silver ETF Document-Review Checklist

A silver ETF comparison should begin with documents because the most important differences are often structural. Fees matter, but they should be read after the investor understands the objective, holdings, benchmark or strategy, and trading mechanics.

Before comparing fees or rankings, classify the exposure route first: physical silver, futures or derivatives, mining-company equities, leveraged or inverse objectives, or another silver-linked structure.

| Checklist item | What to verify | Why it matters |

|---|---|---|

| Stated objective | Read the objective in the prospectus, factsheet, or issuer literature. | The objective defines what the product is trying to track or deliver. |

| Holdings or reference asset | Check whether exposure comes from bullion, futures, derivatives, miners, cash, collateral, or a mix. | The same silver label can produce different investor exposure. |

| Index, mandate, or strategy | Identify whether the product tracks an index, follows a trust objective, or uses manager discretion. | The strategy explains how exposure is selected and maintained. |

| Physical, futures, derivative, or miner exposure | Classify the actual exposure route instead of relying on the product name. | Each route has different tracking, cost, and risk mechanics. |

| Expense ratio or sponsor fee | Review the stated recurring cost and any structure-specific cost language. | Costs can reduce the return an investor receives relative to the reference asset. |

| NAV and market price | Compare how the issuer reports net asset value and how the shares trade in the market. | ETF shares may trade at prices that differ from NAV, especially under stressed or illiquid conditions. |

| Premium, discount, or tracking difference | Look for disclosures on tracking, premiums, discounts, and historical deviations where available. | Silver exposure is not always identical to the spot price an investor watches on a chart. |

| Liquidity and spread | Review trading volume, bid-ask spread behavior, and creation/redemption mechanics where disclosed. | Trading cost can be different from the headline management fee. |

| Distributions | Check whether the product expects to make distributions and what drives them. | A silver ETF should not be assumed to provide income unless the documents support that expectation. |

| Tax structure | Review tax sections and local rules rather than assuming standard equity-fund treatment. | Tax treatment can depend on structure, jurisdiction, account type, and investor circumstances. |

| Domicile, trust, ETF, or ETC status | Confirm the legal structure and domicile in the product documents. | Exchange-traded silver exposure is not structured identically across markets. |

| Currency hedged or unhedged terms | Check whether currency exposure is hedged, unhedged, or share-class specific. | Currency terms can change the investor’s realized return in local currency. |

| Prospectus and factsheet review | Use the latest issuer documents before comparing products. | The documents control the objective, risks, costs, and mechanics. |

What to Check Before Comparing Silver ETFs

The phrase “best silver ETF” can push investors toward rankings too early. A better first step is to identify the type of exposure being compared. A physically backed product, a futures-linked product, a miner-equity product, and a leveraged product do not solve the same problem even when each is silver-related.

Costs should also be read broadly. The expense ratio or sponsor fee is only one cost layer. Premiums and discounts, bid-ask spreads, tracking differences, taxes, and currency terms can also affect the result. A product with a low headline fee may still be unsuitable for a particular comparison if its structure or tracking objective does not match the investor’s intended exposure.

Income assumptions need separate review. Many investors associate ETFs with dividends or distributions, but a silver ETF should not be assumed to behave like bond ETFs, where income orientation is often central to the product category. Silver-linked products may or may not distribute cash depending on their structure, holdings, and document rules.

Illustrative scenario: Two silver-labeled products may look similar in a search result. One may be designed around physical silver exposure with a sponsor fee, while another may use futures or a broader strategy with different tracking behavior and currency terms. The product names alone do not show which one matches an investor’s intended exposure. The documents have to answer that question first.

Silver ETF vs Physical Silver, Silver Miners, and Gold ETFs

A silver ETF and physical silver can both be connected to the silver price, but they are not the same ownership experience. Direct physical silver ownership involves custody, storage, insurance, spreads, and personal control over the asset. A silver ETF involves shares in an exchange-traded vehicle, with rights, costs, redemption mechanics, and risks defined by the product documents.

A silver miner ETF is different again. Miner exposure is equity exposure. It may be influenced by silver prices, but it can also reflect company costs, mine quality, management decisions, debt, jurisdiction risk, dilution, operating leverage, and broader equity-market conditions. A silver miner ETF should not be treated as a simple substitute for direct silver price exposure unless the documents and holdings support that interpretation.

Gold ETFs and silver ETFs are neighboring precious-metal products, not interchangeable products. Gold and silver can respond differently to industrial demand, monetary conditions, investor flows, and product structure. A broader commodity ETF may include silver as only one part of a wider basket, so its return can be driven by energy, agriculture, metals, or index-weighting rules rather than silver alone.

| Comparison | Core difference | Common mistake |

|---|---|---|

| Silver ETF vs physical silver | ETF shares are listed securities; physical silver is directly owned metal. | Assuming ETF shares equal personal custody of bullion. |

| Silver ETF vs silver miner ETF | Silver-linked exposure differs from equity exposure to mining companies. | Assuming miner stocks track silver prices one-for-one. |

| Silver ETF vs gold ETF | Both are precious-metal categories, but the underlying metal and demand drivers differ. | Assuming all precious-metal ETFs behave the same way. |

| Silver ETF vs broad commodity ETF | A commodity basket may dilute silver-specific exposure. | Assuming commodity exposure always means meaningful silver exposure. |

Common Mistakes When Reading Silver ETF Labels

- Assuming the label tells the full structure: The label can identify a silver theme, but the documents explain the objective, holdings, and risks.

- Assuming tracking is perfect: Fees, spreads, premiums, discounts, roll effects, liquidity, and market price behavior can create differences from the reference asset.

- Assuming tax treatment is universal: Tax mechanics can depend on product structure, investor location, account type, and local rules.

- Assuming distributions are guaranteed: Distribution policy depends on the product design and should be checked directly.

- Assuming ETF exposure equals physical custody: A silver ETF share is not automatically the same thing as personally storing silver bullion.

Silver ETF Limitations

Silver ETF exposure still carries commodity-price risk. Silver can be volatile, and an exchange-traded wrapper does not remove the underlying exposure risk. The wrapper can make trading and portfolio access easier, but it does not turn silver into a stable or income-guaranteed asset.

Tracking and liquidity are also limitations. A product may not match spot silver perfectly, and share prices can be affected by premiums, discounts, trading spreads, market stress, or instrument-level mechanics. Futures-linked and leveraged products require particular caution because reset periods, compounding, and roll mechanics can change longer-period interpretation.

Tax and structure are document-dependent. A silver-linked product may be organized as a trust, ETF, ETC, fund, or another exchange-traded structure depending on jurisdiction. Investors should not assume that every silver product receives the same tax treatment or gives the same legal rights.

Related ETF Concepts

A silver ETF is easiest to understand when it is placed inside the wider ETF structure map. The neighboring concepts below help separate silver exposure from management style, income-oriented ETF categories, and broader commodity baskets.

| Related concept | Why it helps |

|---|---|

| actively managed ETF | Shows how ETF exposure can depend on manager discretion rather than only passive tracking. |

| bond ETF structure | Helps separate commodity-linked exposure from income-oriented fixed-income ETF mechanics. |

| commodity ETF structure | Places silver exposure inside the broader commodity ETF category without assuming silver is the only driver. |

FAQ

What is a silver ETF?

A silver ETF is an exchange-traded product that gives exposure to silver or silver-linked assets. The exact exposure depends on the product’s objective, holdings, reference asset, structure, costs, tracking behavior, liquidity, tax mechanics, and documents.

Is a silver ETF the same as owning physical silver?

No. A silver ETF share is an exchange-traded security, while physical silver is directly owned metal. Some products may be backed by silver bullion, but shareholder rights, custody, redemption mechanics, costs, and risks are controlled by the product documents.

Can a silver ETF hold silver mining stocks?

Some silver-related ETFs may focus on silver mining companies, but that is different from direct silver price exposure. Mining-company exposure includes equity-market and business risks, not only silver price movement.

How should investors compare silver ETFs?

Comparison should start with the stated objective, holdings or reference asset, structure, fees, NAV and market price behavior, tracking, liquidity, distributions, tax mechanics, currency terms, and issuer documents. Rankings alone do not show whether two products provide the same exposure.

Do silver ETFs always track silver prices perfectly?

No. Fees, spreads, premiums, discounts, futures mechanics, liquidity, market price behavior, and product structure can create differences between the ETF return and the silver price or reference benchmark.