Top down investing is an investment research approach that starts with broad economic, market, regional, sector, or industry conditions before narrowing toward individual companies or securities. It changes where the research process begins: broad context comes first, company-level analysis comes later.

The approach is useful because it can help an investor organize a large opportunity set. Instead of starting with one company and then asking whether the wider environment supports the thesis, a top-down process starts with the wider environment and asks which areas may deserve closer company-level review.

That does not make top down investing a standalone decision rule. A favorable macro view, sector view, or industry view can explain why something is worth studying, but it does not establish that a company, fund, ETF, sector, country, or allocation is attractive. Business quality, valuation, cash flow, balance-sheet risk, and thesis durability still need separate review.

What Is Top Down Investing?

Top down investing is a broad-to-specific research lens. It typically begins with questions about the economy, interest rates, inflation, policy conditions, market environment, regional exposure, sector strength, or industry trends. The investor then narrows the field toward companies, securities, funds, or other investable vehicles that may be affected by those broader forces.

The central idea is evidence order. A top-down investor does not ignore individual companies. The company review simply comes after the broader filter. The process might begin with a view that one industry has better demand conditions than another, but the final research still has to test whether any individual company has durable earnings, acceptable valuation, resilient cash flow, and manageable risk.

This is why top down investing should be treated as a research sequence, not as proof. The approach can help decide where to look first. It cannot replace the work needed to judge whether a specific investment candidate has enough quality, valuation support, and risk control to deserve further attention.

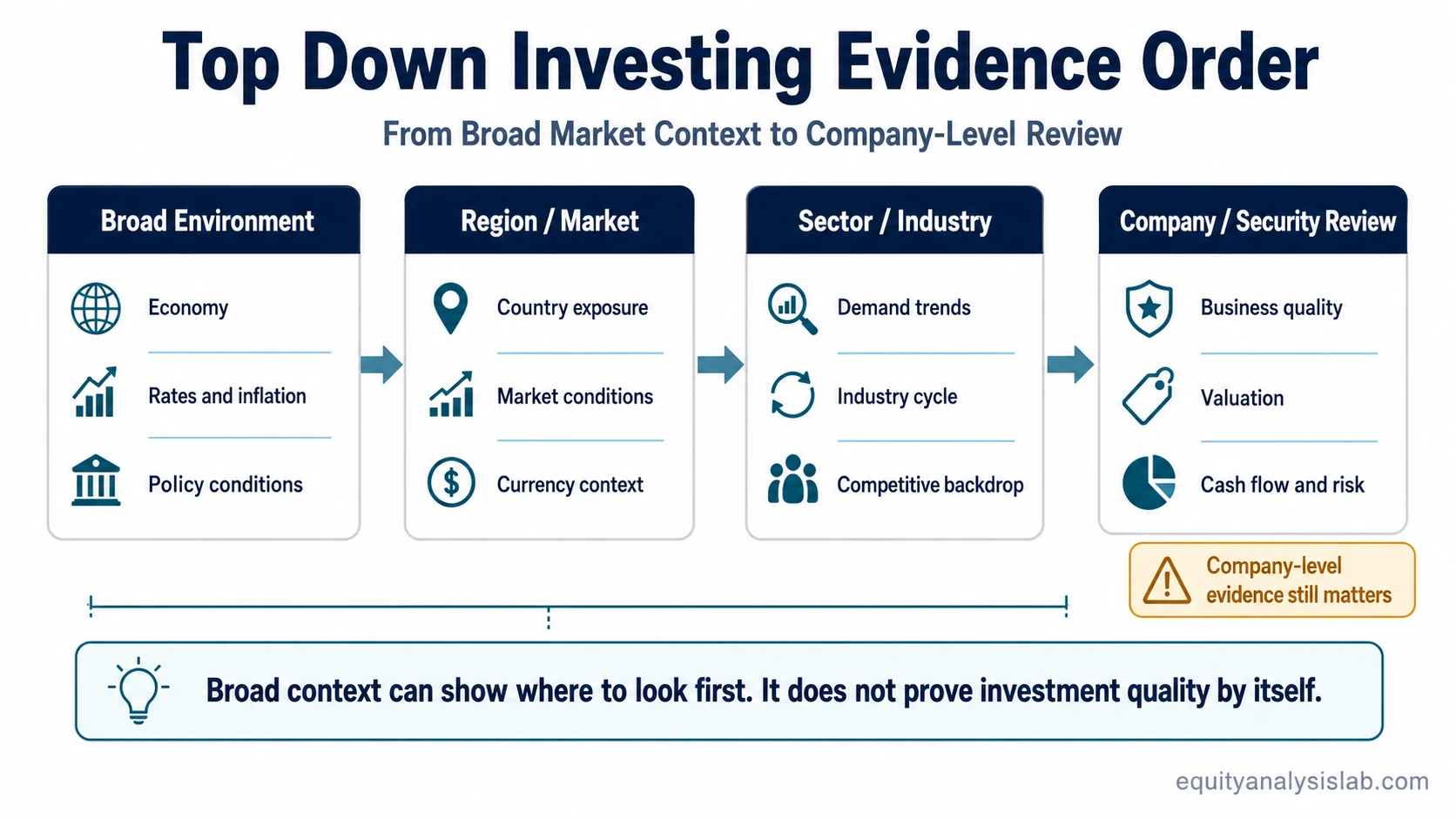

How the Top-Down Evidence Order Works

A top-down process usually moves from the largest context to the most specific evidence. The exact sequence can vary, but the structure is usually similar: first the broad environment, then the market or region, then the sector or industry, then the individual company or security.

| Evidence layer | What it helps answer | What it cannot prove |

|---|---|---|

| Macro environment | Whether broad conditions may support or pressure risk assets, industries, or investor appetite. | It cannot prove that any individual company is high quality or attractively valued. |

| Region or country | Whether a geographic market may have stronger or weaker policy, currency, growth, or demand conditions. | It cannot prove that all companies in that market share the same risk and opportunity profile. |

| Sector or industry | Whether a group of companies may benefit from a theme, cycle, demand trend, or structural change. | It cannot prove that every company in the sector has strong margins, cash flow, or balance-sheet quality. |

| Company or security | Whether the specific candidate has business quality, valuation support, cash-flow strength, and thesis durability. | It cannot remove uncertainty or turn a broad theme into a guaranteed outcome. |

The useful part of the sequence is discipline. Broad evidence narrows the research universe. Company evidence tests whether the narrowed list still holds up. If the broad filter replaces the company review, the process becomes weaker rather than stronger.

What Top Down Investing Can and Cannot Prove

Top down investing can help clarify where the research process should begin. It can highlight sectors, industries, regions, or themes that may deserve attention. It can also help an investor avoid studying every company in the market with the same level of effort.

Its limit is proof. A broad theme can be directionally useful and still be too general. Sector strength can hide weak companies. A strong industry trend can already be priced into valuations. A favorable macro view can be offset by poor balance-sheet quality, weak cash conversion, dilution, management execution risk, or fragile margins.

Core limitation: top down investing changes the order of review, not the standard of proof. The final judgment still depends on company-level evidence, valuation context, cash-flow durability, balance-sheet risk, and the assumptions behind the thesis.

This distinction matters because a top-down label can sound more complete than it is. A macro or sector view may explain why a candidate enters the research list, but it should not be treated as a shortcut around business analysis. The stronger use is to combine broad filtering with specific evidence, not to let broad filtering replace it.

Where Top Down Investing Fits in Stock Selection

In stock selection, top down investing can work as an early screening lens. An investor may begin by asking which parts of the market have better demand conditions, stronger earnings revisions, more favorable policy exposure, or less pressure from financing costs. That can produce a narrower field for deeper review.

The next step is not automatic selection. The investor still needs to ask whether a specific company has a business model that can benefit from the broader theme, whether margins are durable, whether cash flow supports reported earnings, whether debt or dilution changes the risk profile, and whether valuation already reflects the positive case.

A useful top-down process therefore separates three questions. First, what broad environment may matter? Second, which sector or industry is most exposed to that environment? Third, which company-level evidence confirms or weakens the case? The third question is where many broad themes become more complicated.

A Simple Top-Down Research Scenario

A generic top-down review might begin with the view that one industry has improving demand conditions. That view can narrow the research universe from the whole market to a smaller group of companies. The next step is to compare those companies on revenue quality, margin durability, free cash flow, leverage, valuation, and management execution risk.

In that scenario, the industry view only creates a candidate universe. It does not decide the outcome. One company may have better cash conversion, another may have more debt, and another may already trade at a valuation that assumes the favorable industry trend continues. The same broad theme can therefore lead to very different company-level conclusions.

Top Down vs Bottom-Up Investing

Top down investing starts with broad context before narrowing toward companies. Bottom-up investing starts with company-specific evidence before giving more weight to the broader environment.

The difference is not that one method always matters more than the other. The difference is the starting point. A top-down lens asks which environments, sectors, or industries may deserve attention first. A bottom-up lens asks which individual companies look strong enough on their own merits first.

The comparison should stay narrow because the main distinction is research order. Top down investing starts with broad context and then tests company-level evidence, while bottom-up investing starts with company evidence and then checks whether the broader setting supports or weakens the thesis.

Common Misuse of Top Down Investing

A common misuse is treating top down investing as a macro prediction engine. Broad economic or sector evidence can be helpful, but it can also be early, late, incomplete, or already reflected in prices. A correct broad theme can still lead to weak investment conclusions if the company-level evidence is poor.

Another misuse is treating sector strength as a substitute for valuation work. A company can operate in a favorable sector and still be overvalued, highly levered, cash-flow weak, or exposed to risks that are not visible at the sector level. The broad lens should guide the research path, not erase the need for deeper analysis.

The approach also becomes weaker when every company inside a theme is treated as interchangeable. Companies in the same sector can have different cost structures, capital intensity, pricing power, balance-sheet strength, and earnings quality. Those differences often determine whether the broad theme has real company-level relevance.

Related Investment Style Lenses

Top down investing is one way to organize research evidence. It can sit beside other investment style lenses that start from different questions.

A GARP investing approach focuses on the balance between growth evidence and reasonable valuation.

A growth-focused analysis starts with evidence about expansion, reinvestment, and future earnings potential.

Those lenses can overlap, but they should not be collapsed into one another. Top down investing mainly defines where research begins. Other styles may define what kind of company evidence receives the most attention. Keeping those roles separate helps avoid turning a broad market view into a complete investment thesis.

The Practical Limit of Top Down Investing

Top down investing begins with the broad environment and narrows toward company or security analysis. Its strength is research organization: it can help identify where to look first. Its limitation is proof: broad macro, regional, sector, or industry evidence cannot replace business quality, valuation, cash flow, balance-sheet, and risk analysis at the company level.