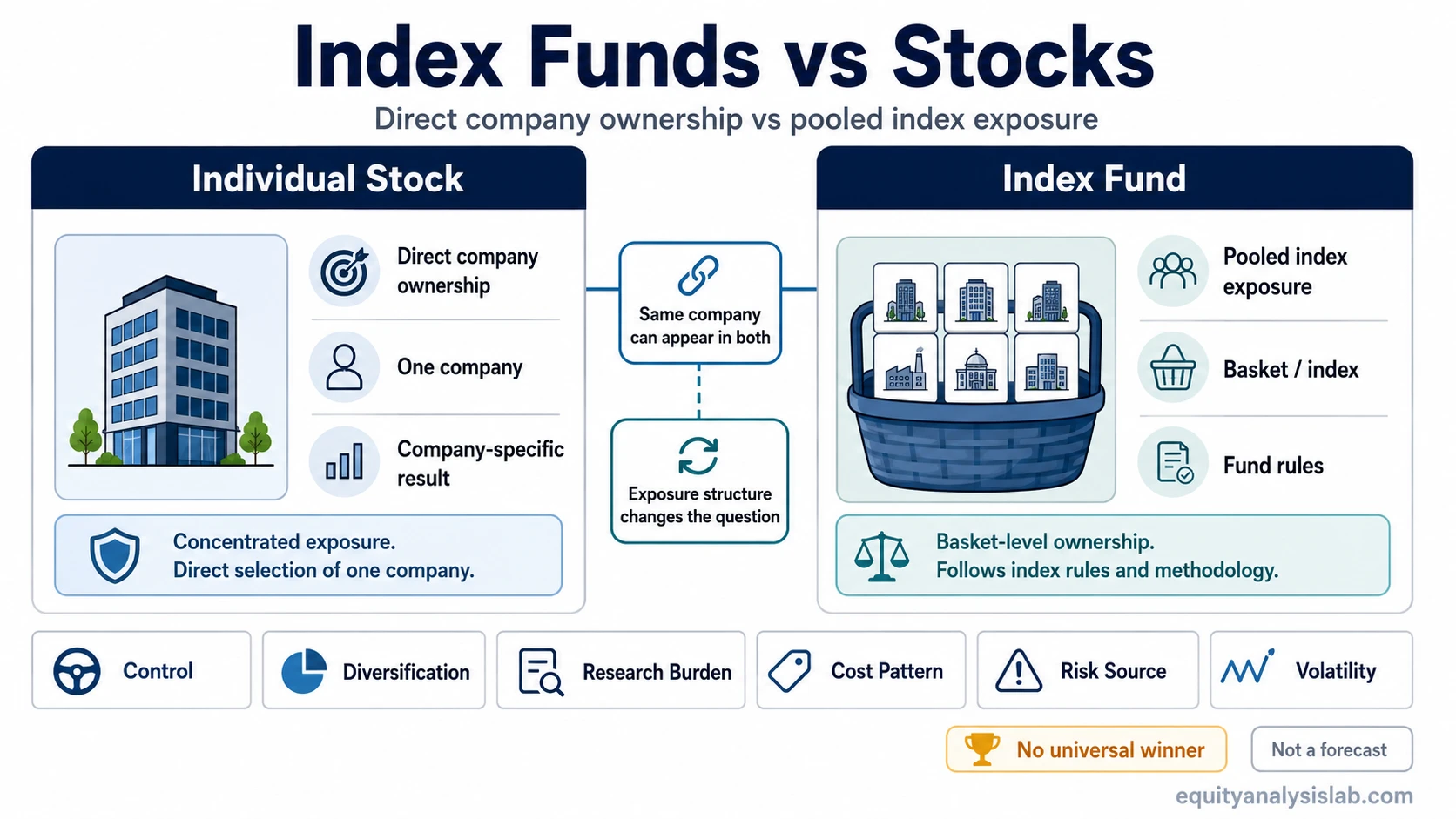

Index funds vs stocks is a comparison between direct ownership of individual companies and pooled exposure through a fund that tracks a basket, index, or market segment. The key distinction is not simply “riskier vs safer”; it is whether the investor wants company-specific exposure and control or broader rules-based exposure with less single-company dependence.

A stock gives direct exposure to one company. An index fund can hold many stocks, but the fund structure turns individual company ownership into basket exposure. That difference affects concentration, research work, costs, control, and the source of risk being accepted.

Key Points

- A stock gives direct exposure to one company’s business results.

- An index fund gives pooled exposure to a basket or index.

- Index funds can hold stocks, but buying a fund is not the same as buying one stock.

- The useful comparison is control, diversification, research burden, cost, and risk source, not a universal winner.

Index Funds vs Stocks: The Core Difference

Buying a stock means choosing direct ownership in a specific business. The investor’s result depends heavily on that company’s revenue, margins, balance sheet, management choices, valuation, and future business outcomes. This is the direct ownership side of equity investing.

Buying an index fund means owning shares of a pooled vehicle that follows a defined index or basket. The investor may still be exposed to many individual companies, but the main evaluation shifts to the basket, index rules, fund structure, and market segment rather than one company alone. An index ETF is one common structure used for index-based exposure.

Simple distinction: a stock asks whether the investor wants direct exposure to a specific company. An index fund asks whether the investor wants rules-based exposure to a basket, index, or market segment.

Key Criteria That Separate Stocks and Index Funds

The comparison becomes clearer when each vehicle is judged by the question it creates. Stocks require company selection. Index funds require fund and index selection. Both can involve risk, cost, and judgment, but the source of those tradeoffs is different.

| Criterion | Stocks | Index funds |

|---|---|---|

| Ownership | Direct company ownership. | Pooled fund ownership. |

| Exposure | Company-specific exposure. | Basket or index exposure. |

| Diversification | Depends on the number and mix of holdings the investor owns. | Built into the fund’s basket, but it varies by index, weighting method, and concentration. |

| Control | The investor selects the companies directly. | The fund rules or index methodology determine the holdings. |

| Research burden | Higher company-specific research burden. | Lower single-company research burden, but the fund and index still need review. |

| Cost | Trading costs, bid-ask spreads, and tax considerations can affect the net result. | Expense ratio, tracking difference, bid-ask spread, liquidity, distributions, and tax treatment can affect the net result. |

| Risk source | Company-specific risk can dominate the outcome. | Single-company risk is diluted, but market, index, sector, and fund-structure risk remain. |

| Volatility | Price movement can be heavily affected by one company’s news, valuation, and business results. | Price movement reflects the fund’s basket and may still be volatile when the market, sector, or index declines. |

| Return path | Depends heavily on the selected companies. | Depends on the basket or index performance minus fund effects. |

| Fit question | “Do I want this company-specific exposure?” | “Do I want broad rules-based exposure to this basket?” |

Risk and volatility should not be treated as the same idea. Volatility describes price movement. Risk source describes what can drive loss, uncertainty, or disappointment. A single stock may be dominated by company-specific risk, while an index fund may reduce that one-company dependence without removing market-level or fund-structure risk.

Same Company, Different Exposure

A company can appear in both structures. An investor could own that company directly through its stock, or own an index fund where the same company is one holding inside a larger basket.

Illustrative example: imagine a large public company included in a broad market index. Buying the company’s stock creates direct exposure to its revenue growth, margins, management choices, valuation, and company-specific risks. Buying an index fund that includes the same company still creates some exposure to that business, but the company is only one part of the fund’s broader holdings.

The difference is not whether the company exists in the portfolio. The difference is how much the company can drive the result. Direct ownership concentrates the outcome around that business. Index-fund ownership spreads the company’s influence across the fund’s broader basket.

The Main Confusion Trap

The common mistake is saying that index funds and stocks are separate categories as if index funds do not own stocks. Many index funds do hold stocks. The real distinction is between direct company ownership and ownership of a fund that packages many holdings under a rule set.

Common mistake: treating “index fund” as the opposite of “stock.” A stock is an ownership interest in a company. An index fund is a pooled vehicle that may contain many stocks, bonds, or other holdings depending on the index and fund design.

This matters because the same underlying company can create a different investment question depending on how it is owned. Direct stock ownership asks whether that company is attractive on its own. Fund ownership asks whether the whole basket, weighting method, cost structure, and exposure profile make sense.

When Stocks May Fit the Investor Question

Stocks may fit the question when the investor is intentionally evaluating a specific company and is willing to accept the research burden that comes with direct ownership. That usually means analyzing business quality, financial statements, competitive position, management choices, valuation, and company-specific risk.

The advantage is control. The investor can choose which companies to own and which ones to avoid. The tradeoff is that a small number of holdings can dominate the outcome. A concentrated position can benefit from a strong company-specific result, but it can also suffer if the company disappoints, the valuation compresses, or a business risk becomes more important than expected.

Decision boundary: a stock choice should not be reduced to whether the broad market is attractive. It is also a company-specific question about business quality, valuation, durability, and risk.

When Index Funds May Fit the Investor Question

Index funds may fit the question when the investor wants exposure to a broader basket instead of making each company selection directly. The fund’s construction, index rules, weighting method, costs, liquidity, and holdings still matter, but the investor is not making a separate thesis for every company in the fund.

The advantage is built-in diversification relative to a single stock. The tradeoff is less direct control. The investor receives the index or basket exposure as designed, including companies or sectors they might not have chosen individually.

Decision boundary: an index fund can reduce single-company dependence, but it does not remove market risk, valuation risk, sector concentration, tracking differences, or fund-specific costs.

Cost, Control, and Research Burden

Stocks and index funds both have costs, but the cost pattern differs. A stock investor may review trading costs, bid-ask spreads, possible tax effects, and the time needed for company research. An index-fund investor may review expense ratio, tracking difference, bid-ask spread, liquidity, distributions, and how closely the fund matches the intended exposure.

Research burden also differs. Direct stock ownership requires more company-specific work because each company can materially change the result. Index funds reduce the need to analyze every holding individually, but they do not remove the need to understand what the fund owns and how the index is built.

Over long periods, return accumulation can be affected by reinvestment, time, costs, and market path. That makes compounding over time relevant to both structures, but it does not make either structure automatically superior.

Where the Comparison Becomes Misleading

The comparison becomes misleading when it turns into a universal answer. “Index funds are safer” is too broad because fund holdings, weighting, sector concentration, liquidity, and market exposure can vary. “Stocks are better for higher returns” is also too broad because stock selection can help or hurt depending on the companies chosen and the prices paid.

Limitation: diversification can reduce dependence on one company, but it does not guarantee a positive result. Control can allow more precise selection, but it does not guarantee better selection. The useful comparison is the type of exposure and responsibility each vehicle creates.

Another misleading shortcut is treating the choice as active versus passive in every case. Some investors hold a small number of stocks with low turnover. Some index funds track narrow, concentrated, or factor-based baskets. The label alone does not explain the actual exposure.

A Neutral Way to Compare the Two

A neutral way to compare index funds vs stocks is to start with the exposure question. If the analysis depends on one company’s business quality, valuation, and risks, the investor is dealing with a stock-specific question. If the analysis depends on a basket, index methodology, fund cost, and broad exposure profile, the investor is dealing with a fund-structure question.

Stock question: Do I want direct exposure to this company’s specific business results?

Index-fund question: Do I want rules-based exposure to this basket, index, or market segment?

Neither question proves suitability. The comparison only clarifies what must be evaluated: company-specific exposure on one side and fund-based basket exposure on the other.

FAQ

What is the main difference between stocks and index funds?

The main difference is direct company ownership versus pooled basket exposure. A stock gives direct exposure to one company. An index fund gives exposure to a fund that tracks an index, basket, or market segment.

Are index funds safer than individual stocks?

Index funds can reduce single-company dependence because they usually hold a basket of securities. That does not make them risk-free. Market risk, sector concentration, fund design, liquidity, tracking difference, and valuation risk can still matter.

Can an index fund contain the same stock I could buy directly?

Yes. A company can be one holding inside an index fund while also being available as a direct stock purchase. The exposure is different because direct ownership concentrates the company-specific result, while fund ownership spreads that company across a broader basket.

Can an investor own both stocks and index funds?

Yes. The two structures are not mutually exclusive by definition. The important question is what role each holding plays, how much concentration it creates, and whether the investor understands the risks and costs of each exposure.

Is stock picking the same as buying individual stocks?

Stock picking usually refers to choosing individual companies rather than accepting a fund’s predefined basket. Buying a stock creates direct company-specific exposure, so the investor needs a reason for selecting that business rather than relying only on broad market exposure.