ETF qualified dividends are ETF dividend distributions that may be eligible for qualified-dividend tax treatment when the fund’s underlying income, distribution classification, and holding-period conditions support that result.

The ETF label does not make a dividend qualified by itself. Classification can be shaped by what the fund owns, how the income is reported, how long the fund and shareholder meet the relevant holding-period conditions, and where the ETF is held.

What ETF Qualified Dividends Mean

ETF qualified dividends are a subset of ETF dividends. They usually begin with income received by the ETF from underlying holdings, then pass through to shareholders with a reported tax character when the fund’s records and eligibility conditions support qualified-dividend treatment.

The key point is classification. An ETF can distribute income, but the tax character of that income is not determined only by the ETF’s yield, name, or distribution schedule.

Key Points About ETF Qualified Dividends

- ETF qualified dividends depend on the income the fund receives and reports.

- Qualified and nonqualified ETF dividends can appear in the same taxable year.

- Holding-period conditions can matter before qualified treatment is available.

- ETF tax efficiency does not mean every ETF distribution is tax-free or qualified.

Qualified vs Nonqualified ETF Dividends

Qualified and nonqualified ETF dividends are both cash or reinvested distributions from an ETF, but they are not treated the same for tax classification. The distinction matters most in taxable accounts, where dividend character can affect how the distribution is reported and reviewed.

| Dividend type | What it generally means | Why investors check it |

|---|---|---|

| Qualified ETF dividend | A dividend distribution that may be eligible for preferential tax treatment when the required conditions are met. | It can change the tax character reported for a taxable account. |

| Nonqualified ETF dividend | A dividend distribution that does not meet qualified-dividend treatment or is sourced from income that is not eligible for that treatment. | It may be reported differently from qualified dividend income. |

| Mixed distribution | A single ETF can report different dividend classifications across distributions or across the same tax year. | The investor should verify the reported classification instead of relying on the ETF category alone. |

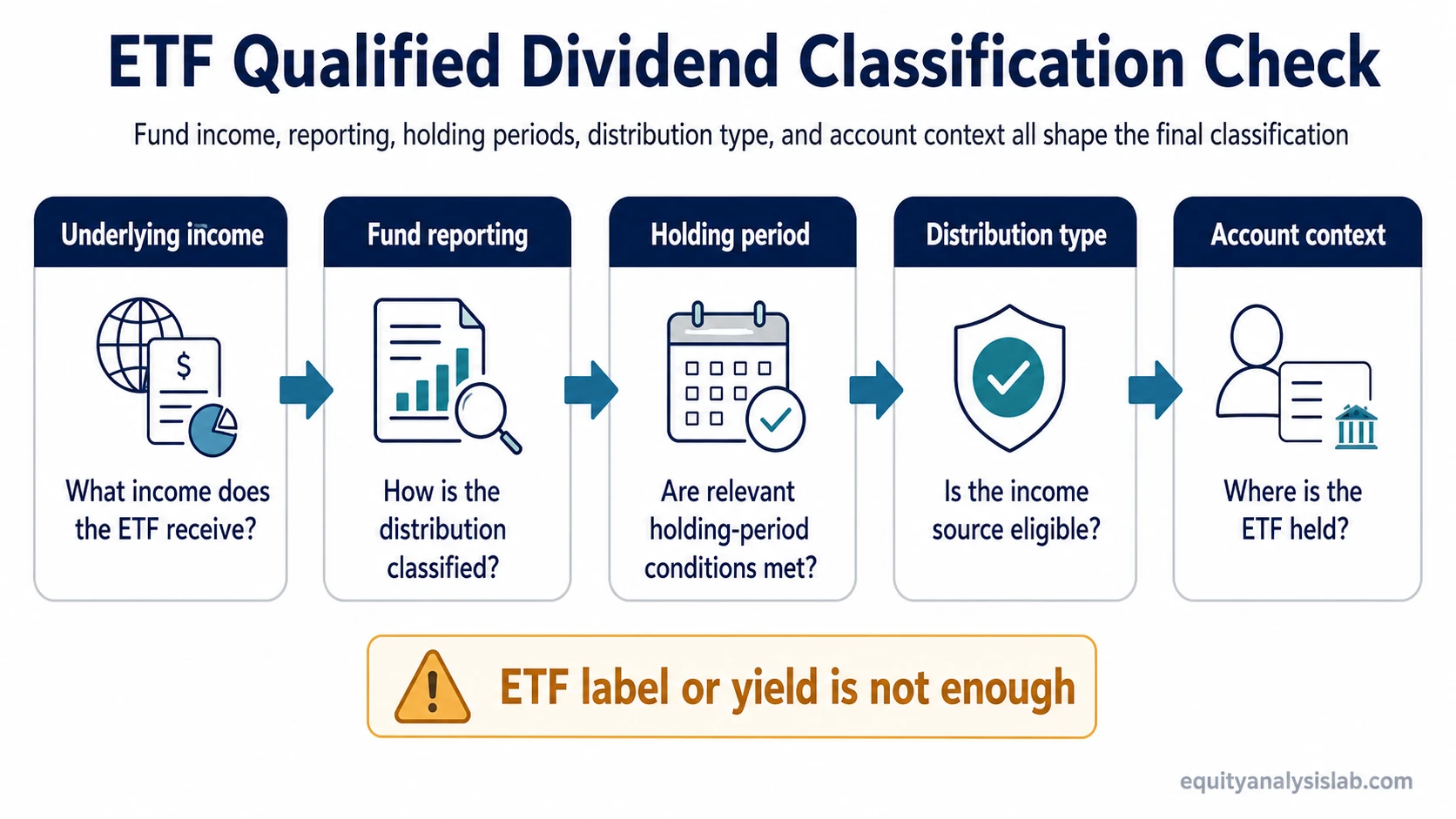

What Determines Whether ETF Dividends Are Qualified

ETF qualified-dividend treatment is best reviewed as a condition chain rather than a simple label. The investor is checking the income source, fund reporting, holding-period requirements, distribution type, and account setting before relying on the qualified classification.

| Condition | What to check | Why it matters |

|---|---|---|

| Underlying income | Whether the ETF receives dividend income that can be eligible for qualified treatment. | The tax character starts with the type of income generated by the fund’s holdings. |

| Fund classification | How the ETF provider reports the distribution in tax documents or tax-center materials. | Fund reporting is the practical source for how the distribution is classified. |

| Holding-period requirements | Whether the relevant holding-period requirements are satisfied for the fund’s income and the shareholder’s ETF holding period. | A dividend may lose qualified treatment if the required holding-period context is not met. |

| Distribution type | Whether the distribution comes from common stock dividends, interest income, REIT income, commodity-linked income, currency exposure, or another source. | Not every income stream inside an ETF is eligible for qualified-dividend treatment. |

| Account context | Whether the ETF is held in a taxable account, tax-deferred account, or tax-exempt account. | The practical tax relevance of qualified-dividend classification can differ by account type, especially between taxable and tax-advantaged accounts. |

Why ETF Tax Efficiency Does Not Make Every Dividend Qualified

ETF tax efficiency usually refers to structural features that can reduce some taxable distribution pressure, especially around portfolio turnover and capital-gains realization. Qualified-dividend classification is a different question.

An ETF can be tax-efficient in one respect and still distribute dividends that are partly or fully nonqualified. Tax efficiency does not convert interest income, certain REIT distributions, commodity-linked income, or other nonqualified income into qualified dividends.

Common Mistakes When Reading ETF Qualified Dividends

- Assuming every dividend ETF pays qualified dividends: A dividend strategy may hold securities or structures that produce different income classifications.

- Using yield as the tax answer: A high yield says little about whether the distribution is qualified, nonqualified, return of capital, or another reported category.

- Assuming every equity ETF distribution qualifies: Equity exposure can help, but fund reporting and holding-period context still matter.

- Confusing ETF tax efficiency with tax-free income: ETF structure may reduce some capital-gains distributions, but dividend income classification remains a separate issue.

- Ignoring account type: Qualified-dividend classification is usually most relevant in taxable accounts, while retirement-account treatment follows different account rules.

A Simple ETF Qualified Dividend Scenario

A generic equity ETF may receive dividend income from several companies during the year. Some of that income may be reported as qualified dividend income, while another portion may be reported differently because of the income source, fund activity, or holding-period context.

The useful question is not whether the ETF is called a dividend ETF. The useful question is whether the provider’s tax reporting and the investor’s account records support qualified-dividend treatment for the specific distribution.

Where to Verify ETF Qualified Dividend Information

ETF qualified-dividend information should be checked through reporting sources rather than assumed from the fund name or distribution yield.

- Form 1099-DIV: Shows how dividend distributions are reported for the account.

- ETF provider tax center: May publish qualified dividend income percentages or year-end tax details.

- Prospectus and tax supplement: Can describe the types of income the fund may generate and how distributions may be treated.

- Account records: Help connect distribution dates, holding periods, and account type to the reported tax character.

- Tax review: Useful when account-level reporting, holding periods, or distribution character are unclear.

ETF Qualified Dividends FAQ

Are all ETF dividends qualified dividends?

No. ETF dividends may be qualified, nonqualified, or reported in another distribution category depending on the fund’s income sources, reporting classification, holding-period context, and account setting.

Can the same ETF pay both qualified and nonqualified dividends?

Yes. An ETF can report different portions of its income differently, especially when the fund receives more than one type of income or when eligibility conditions differ across distributions.

Does a dividend ETF label guarantee qualified dividends?

No. A dividend ETF label describes the fund’s investment focus, not the final tax classification of every distribution. Provider tax documents and Form 1099-DIV are more relevant than the label.