A core satellite portfolio separates a durable portfolio core from smaller satellite positions so each holding has a defined role. The core is meant to carry broad foundation exposure, while satellites add targeted exposure that the investor wants to monitor separately.

The approach becomes useful only when role, weight, overlap, and review discipline are explicit. A portfolio can use the core-satellite label and still become concentrated if the satellites duplicate the core, grow too large, or depend on the same outcome driver.

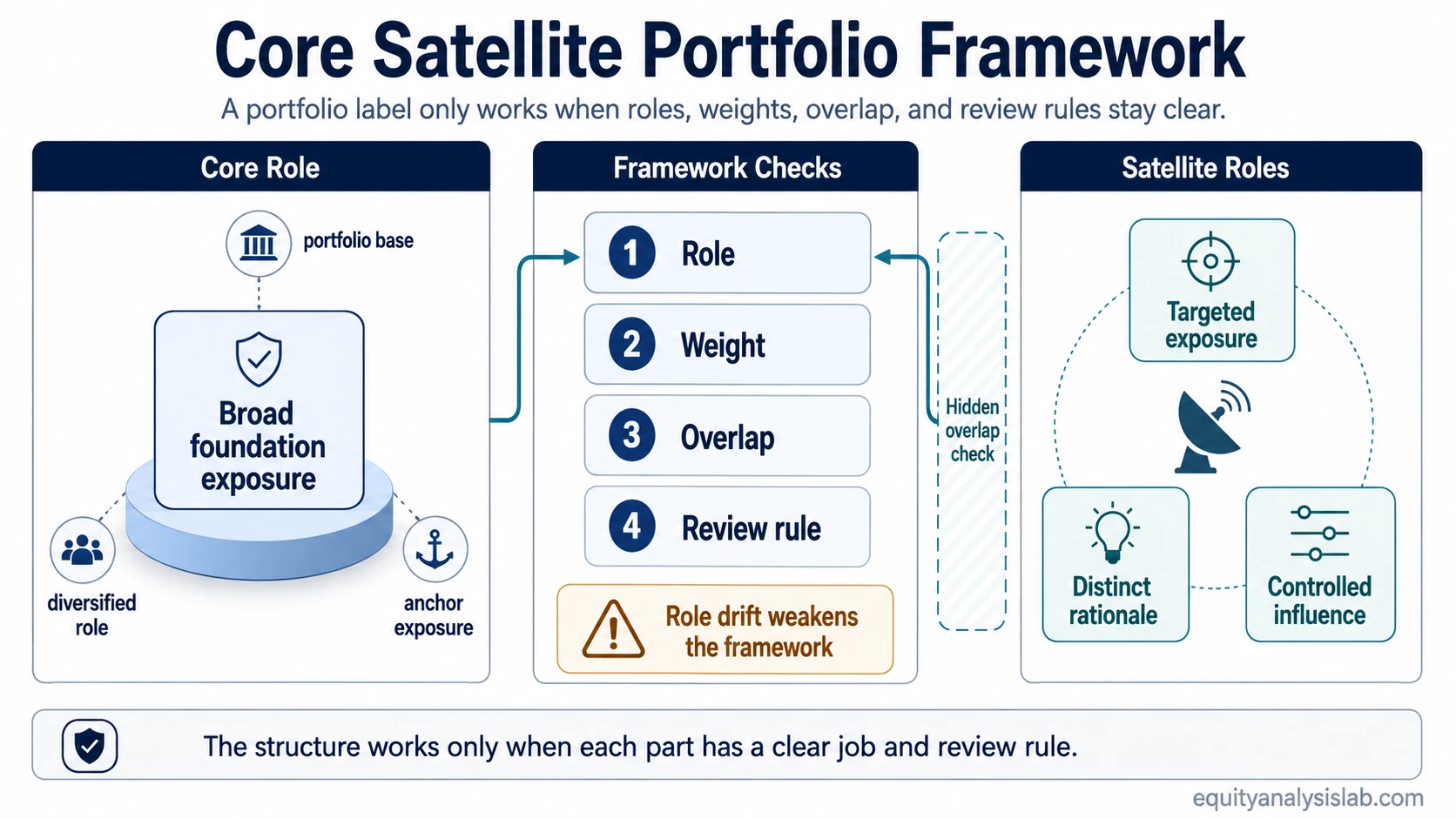

Definition: A core satellite portfolio is a portfolio construction framework that assigns holdings into a broad core and smaller satellite positions, then reviews whether the weights, exposures, and rebalancing rules still support those roles.

Key Points

- A core satellite portfolio is a role framework, not a fixed allocation rule.

- The core usually carries broad foundation exposure, while satellites add smaller targeted exposures.

- Holdings count alone can mislead when satellites overlap with the core.

- Rebalancing and review rules help prevent satellites from becoming the real portfolio driver.

- No portfolio structure guarantees lower risk, higher returns, or suitability for every investor.

What Is a Core Satellite Portfolio?

A core satellite portfolio divides portfolio holdings by job. The core is the broad foundation. Satellites are smaller positions used for specific exposures, themes, strategies, regions, sectors, or manager views that should not quietly dominate the whole portfolio.

The core is often built with broad, diversified vehicles. An index ETF can be one possible building block because it can provide diversified exposure in a simple structure, but the framework does not require any single product type.

The satellite side is not automatically more aggressive, more sophisticated, or more attractive. It is simply the part of the portfolio where the investor is choosing narrower or more specific exposure than the core provides.

How the Core and Satellite Roles Interact

The useful question is not only what the portfolio owns. The stronger question is what each part is supposed to do, how large it is, what it overlaps with, and what would make the role invalid.

| Framework part | Portfolio role | What to check | Failure condition |

|---|---|---|---|

| Core | Broad foundation exposure | Whether it is diversified enough for the intended portfolio base | The core is narrow, concentrated, expensive, or dependent on one dominant driver |

| Satellite | Targeted exposure outside the broad foundation | Whether the satellite has a clear reason for being separate | The satellite is added because it sounds attractive, not because it has a defined role |

| Weight | Controls how much the role can affect the portfolio | Whether the size matches the intended importance of the role | Satellites become large enough to drive most outcomes |

| Overlap | Shows whether different labels create the same exposure | Whether satellites duplicate holdings, sectors, factors, or economic drivers already inside the core | The portfolio looks diversified by name but depends on the same exposure underneath |

| Review rule | Keeps the structure from drifting | Whether there is a repeatable process for checking weights and role changes | The portfolio changes shape without a deliberate decision |

Core-Satellite Framework Interaction Map: role comes first, weight gives the role influence, overlap tests whether the role is truly different, and review discipline checks whether the structure still matches its intended design.

Why Holdings Count Alone Can Mislead

A portfolio with many holdings can still be concentrated if those holdings respond to the same business cycle, interest-rate change, sector trend, currency move, or valuation pressure. The core-satellite label does not solve that problem by itself.

Diversification depends on exposure, not only on the number of positions. A broad core plus several satellites can still create hidden concentration when the satellite positions already sit heavily inside the core or lean toward the same driver.

Common mistake: treating every satellite as an independent idea. A satellite position may look separate in the holdings list but still increase the same exposure already carried by the core.

How Asset Allocation Shapes the Framework

Core-satellite construction sits inside the broader allocation structure. Asset allocation determines the broad mix of portfolio exposures, while the core-satellite framework assigns roles within that mix.

For example, the same framework can be applied inside an equity sleeve, a multi-asset portfolio, or a narrower portfolio segment. The key distinction is that asset allocation describes the broad exposure structure, while core-satellite construction describes how the foundation and targeted positions interact inside that structure.

That distinction prevents the framework from becoming a disguised model portfolio. The core is not automatically one allocation, and satellites are not automatically one percentage. The correct interpretation depends on the investor’s objectives, constraints, risk capacity, and review process.

Where the Core-Satellite Framework Can Weaken

The structure weakens when the labels remain but the roles disappear. A portfolio can still be called core-satellite even after the satellites have become the real driver of results.

When the framework becomes only a label:

- Satellites overlap heavily with the core.

- Satellites become too large relative to their intended role.

- The core is not actually broad or resilient enough to act as a foundation.

- No review or rebalancing rule exists.

- The satellite rationale is vague or trend-driven.

- One sector, factor, theme, currency, rate sensitivity, or economic driver dominates the portfolio.

The most important failure condition is role drift. Once a satellite position becomes large enough to drive the portfolio, it is no longer just a satellite in practical terms, even if the label has not changed.

How Rebalancing Keeps the Structure From Drifting

Portfolio weights change as holdings move differently over time. A satellite position can become larger after strong relative performance, while the core can become less influential than originally intended.

Portfolio rebalancing is the maintenance process that brings weights back toward the intended structure or forces a deliberate decision to change the structure. It does not guarantee risk control, but it helps separate planned exposure from accidental drift.

A useful review asks whether the core still carries the foundation, whether each satellite still has a distinct role, whether overlap has increased, and whether the portfolio now depends too much on one outcome.

Core Satellite Portfolio Example in Context

A portfolio may use a broad equity fund as the core and add several sector or thematic funds as satellites. The holdings list may look diversified because the positions have different fund names, but the actual exposure can still lean toward the same companies, sectors, valuation style, or economic driver already inside the core.

The framework is more coherent when the satellite positions have defined roles, limited weights, and a clear reason for being separate from the core. The framework is weaker when the satellites mostly repeat the core exposure and grow large enough to dominate portfolio behavior.

The diagnostic question is not whether the portfolio has a core and satellites by label. The diagnostic question is whether the core still anchors the portfolio and whether the satellites still add distinct, controlled exposure.

Benefits and Limits of a Core-Satellite Portfolio

The potential benefit of core-satellite construction is organizational clarity. It can separate broad foundation exposure from more targeted portfolio ideas and make review discussions more disciplined.

| Potential benefit | Why it can help | Important limit |

|---|---|---|

| Clearer role assignment | Each holding can be judged by its portfolio job | A label does not prove that the role is still valid |

| Better exposure review | Core and satellite weights can be checked separately | Overlap can hide inside different fund names or strategies |

| More disciplined maintenance | Rebalancing can identify drift before it becomes accidental concentration | Review rules do not remove market risk or suitability risk |

| Room for targeted ideas | Satellites can isolate narrower exposures from the foundation | Targeted exposure can increase dependence on one outcome driver |

The strongest version of the approach makes each role testable: what the core anchors, what each satellite adds, how much influence each role has, and what would make the portfolio too dependent on one driver.

FAQ

Is a core satellite portfolio the same as asset allocation?

No. Asset allocation describes the broad mix of exposures, while core-satellite construction assigns roles inside that mix. The two ideas can work together, but they answer different portfolio questions.

Does a core satellite portfolio require a passive core?

No. Many explanations use a passive core because it is simple to understand, but the framework is about role separation. The core must be suitable for the intended foundation role, not automatically passive by rule.

Can satellites make a portfolio less diversified?

Yes. Satellites can reduce diversification when they overlap with the core or concentrate the portfolio in the same sector, factor, theme, or economic driver.

Does core-satellite construction guarantee better returns?

No. The framework can organize portfolio roles and review discipline, but it does not guarantee returns, reduce all risk, or make an allocation suitable for every investor.