An income statement shows profitability under accrual accounting: revenue, expenses, and net income recognized for a period. A cash flow statement shows how cash actually moved through operating, investing, and financing activities. Investors need both because profit can appear before cash is collected, while cash flow can be affected by working capital, capital spending, or financing activity.

Core distinction: the income statement answers what profit the company recognized, while the cash flow statement answers what cash moved and where it moved.

Key Points

- The income statement measures accrual profitability through revenue, expenses, operating income, and net income.

- The cash flow statement tracks cash movement across operating, investing, and financing activities.

- Net income and cash flow can diverge because of non-cash charges, receivables, inventory, working capital, capital expenditures, or financing activity.

- Investors should read both statements together instead of treating either one as a standalone verdict on business quality, valuation, or future returns.

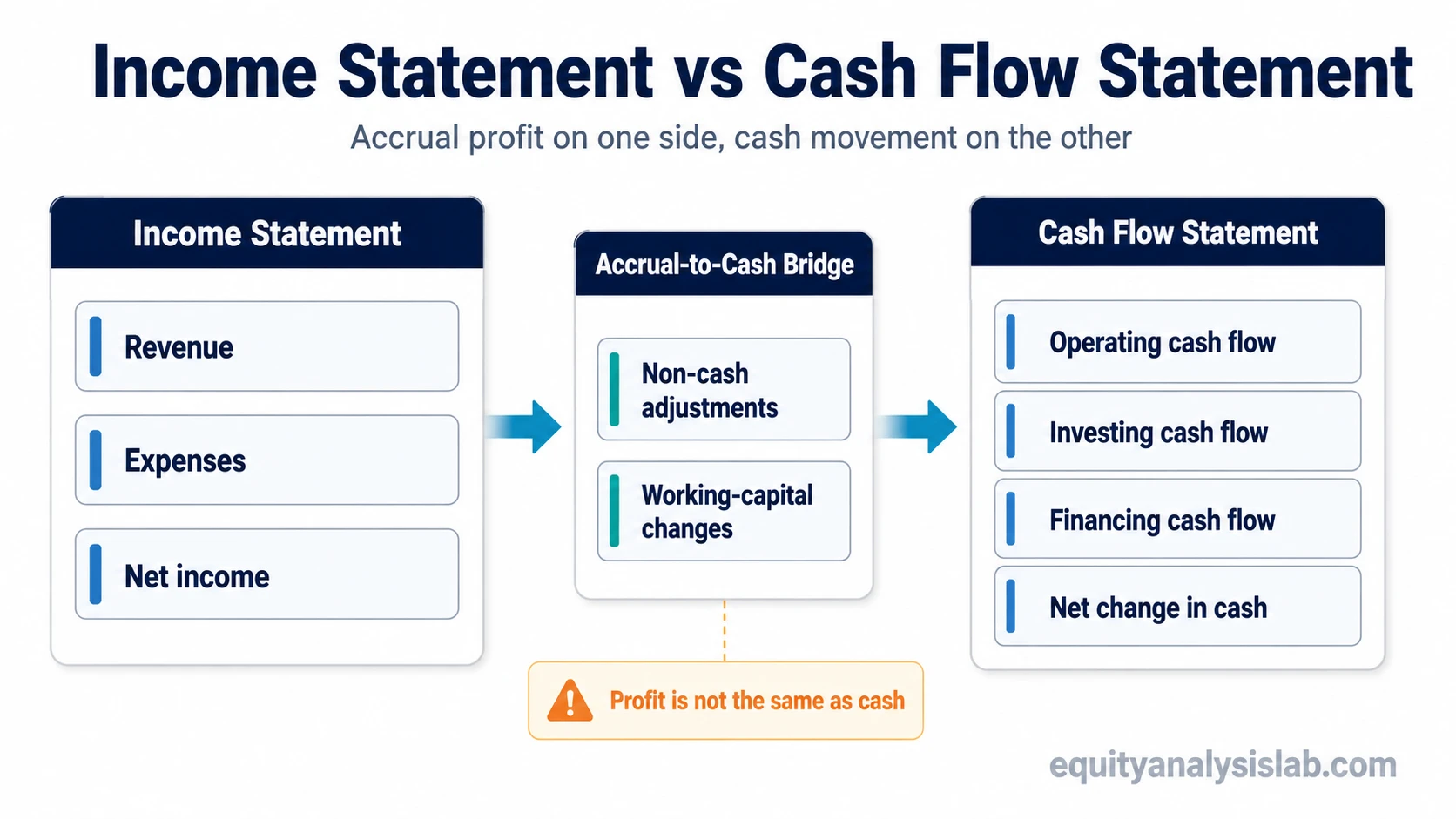

Income Statement vs Cash Flow Statement: The Core Difference

The income statement is built around accrual accounting. Revenue can be recognized when it is earned, and expenses can be matched to the period in which they relate, even if the related cash has not moved yet. This makes the statement useful for reading margins, expense structure, operating performance, and accounting profitability.

The cash flow statement is built around cash movement. It starts from the company’s cash activity and separates it into operating, investing, and financing sections. It helps investors test whether reported profit is converting into cash, whether working capital is absorbing cash, whether capital expenditures are heavy, and whether the company depends on financing activity.

Investor-use criterion: use the income statement to understand earnings performance; use the cash flow statement to test cash conversion and the sources or uses of cash behind that performance.

Key Differences Between the Two Statements

| Comparison point | Income statement | Cash flow statement |

|---|---|---|

| Accounting basis | Accrual-based recognition of revenue and expenses. | Cash-based movement through operating, investing, and financing activities. |

| Main question answered | Did the company recognize a profit or loss during the period? | Where did cash come from, where did it go, and how did cash change? |

| Important line items | Revenue, cost of revenue, gross profit, operating expenses, operating income, taxes, net income. | Cash from operations, cash from investing, cash from financing, capital expenditures, working-capital changes, net change in cash. |

| Investor use | Margin analysis, earnings trend, cost structure, operating leverage, profitability quality questions. | Cash conversion, working-capital pressure, capital intensity, financing dependence, liquidity movement. |

| Main limitation | Profit can be recognized before cash is collected, and non-cash items can affect earnings. | Cash flow can be temporarily helped or hurt by timing, working capital, asset sales, borrowing, or reduced investment. |

How the Two Statements Connect

The two statements are not separate stories. Under the indirect method, the cash flow statement usually begins with net income, then adjusts that accounting profit to explain cash from operating activities.

Accrual-to-cash bridge: net income is adjusted for non-cash items such as depreciation or amortization, then adjusted again for working-capital changes such as receivables, inventory, payables, and other operating balances. The result is operating cash flow, which can be higher or lower than reported net income.

This bridge is the reason investors often compare net income with operating cash flow. If earnings are rising but operating cash flow is consistently weak, the gap can point to timing differences, working-capital pressure, accounting effects, or earnings-quality questions that require deeper review.

Where Each Statement Fits in Company Analysis

The income statement is usually the better starting point when the main question is about profitability. It shows whether revenue is growing, whether gross or operating margins are changing, and whether expenses are rising faster or slower than sales.

The cash flow statement is usually the better starting point when the main question is about cash conversion. It shows whether operations are generating cash, whether the company is spending heavily on assets, whether debt or equity financing is supporting the business, and how the cash balance changed.

| Investor question | Start with | Then check |

|---|---|---|

| Are sales and profit improving? | Income statement | Revenue growth, margins, operating income, net income. |

| Is profit converting into cash? | Cash flow statement | Operating cash flow, working-capital changes, non-cash adjustments. |

| Is the business capital intensive? | Cash flow statement | Capital expenditures and investing cash flow. |

| Are margins improving or weakening? | Income statement | Gross margin, operating margin, expense ratios. |

| Is the company relying on outside capital? | Cash flow statement | Debt issuance, debt repayment, share issuance, buybacks, dividends. |

Why Net Income and Cash Flow Can Diverge

Net income and cash flow can move differently because accounting profit and cash movement are measured in different ways. A company may recognize revenue before receiving cash, record expenses that do not require immediate cash payment, or spend cash on assets that do not flow through the income statement all at once.

- Non-cash expenses: depreciation, amortization, and some stock-based compensation can reduce net income without using cash in the same period.

- Receivables: revenue may be recognized before customer cash is collected.

- Inventory: cash can be tied up in inventory before goods are sold.

- Payables: delaying supplier payments can temporarily support operating cash flow.

- Capital expenditures: cash can leave the business for long-term assets even when the income statement spreads the cost over time.

- Financing activity: borrowing, debt repayment, share issuance, dividends, or buybacks can change cash without directly reflecting operating profit.

Common mistake: a gap between net income and cash flow is not automatically good or bad. The reason for the gap matters more than the gap itself.

Same Company, Different Reading

A company can report rising net income while operating cash flow weakens. That can happen if sales are recognized but customers have not paid yet, if inventory is building, or if working capital absorbs cash. The income statement may show better profitability, while the cash flow statement shows that cash conversion is not keeping pace.

Example scenario: a company reports higher revenue and net income, but accounts receivable rises sharply and operating cash flow falls. The income statement shows stronger reported profit. The cash flow statement raises a follow-up question: is the company collecting cash efficiently, or are reported earnings running ahead of cash receipts?

The opposite can also happen. A company may report weak net income because of a large non-cash expense, while operating cash flow remains healthy. In that case, the cash flow statement helps separate accounting charges from cash generated by the business.

Where to Look in Company Filings

In annual and quarterly reports, the income statement and cash flow statement usually appear near the balance sheet and notes to the financial statements. The exact labels vary by company and reporting standard, but the investor’s reading task is the same: connect reported profit with cash movement and balance-sheet changes.

| Filing area | What to inspect | Why it matters |

|---|---|---|

| Income statement | Revenue, gross profit, operating income, net income. | Shows the period’s accrual profitability and margin structure. |

| Operating cash flow section | Net income reconciliation, non-cash adjustments, working-capital changes. | Shows how accounting profit converted into operating cash. |

| Investing cash flow section | Capital expenditures, acquisitions, asset purchases, asset sales. | Shows how cash was used for investment or recovered from assets. |

| Financing cash flow section | Debt issuance, debt repayment, share issuance, repurchases, dividends. | Shows whether cash changed because of financing decisions. |

| Notes and management discussion | Revenue recognition, working-capital explanations, capital spending plans. | Provides context for gaps between profit and cash flow. |

How Investors Should Read the Two Together

Start with the income statement to understand the company’s earnings performance. Then use the cash flow statement to test whether those earnings are turning into cash and where the cash is being used. The strongest analysis usually compares both statements across several periods rather than relying on one quarter or one year.

- Check revenue, margins, operating income, and net income.

- Compare net income with cash from operations.

- Review working-capital changes for receivables, inventory, and payables.

- Check capital expenditures and investing cash flow.

- Review financing cash flows for borrowing, repayment, share issuance, buybacks, or dividends.

- Compare the pattern across multiple periods and against the company’s business model.

This sequence keeps the analysis balanced. Profitability without cash conversion can require caution, but cash flow without earnings quality can also be misleading if it depends on temporary timing, underinvestment, borrowing, or asset sales.

Limits of the Comparison

The income statement vs cash flow statement comparison is a starting point, not a final verdict. A single-period mismatch between net income and cash flow may reflect normal timing. A persistent mismatch may require deeper work on revenue recognition, weakening cash collection, inventory pressure, or a more serious earnings-quality issue.

Interpretation limit: the comparison does not prove whether a stock is attractive, whether a company is high quality, or whether future returns will be strong. The income statement helps investors read earnings performance; the cash flow statement helps test cash conversion and cash movement. Both need context from the company’s filings and business model.

FAQ

What is the main difference between an income statement and a cash flow statement?

The income statement shows accrual profitability for a period, including revenue, expenses, and net income. The cash flow statement shows actual cash movement through operating, investing, and financing activities.

Can a company be profitable but have negative cash flow?

Yes. A company can report net income while cash flow is weak or negative if cash is tied up in receivables, inventory, capital expenditures, or other timing differences.

Is the cash flow statement more important than the income statement?

Not universally. The income statement is better for analyzing profitability and margins, while the cash flow statement is better for analyzing cash conversion, capital intensity, and financing activity. Investors usually need both.

Why do investors compare net income with operating cash flow?

Investors compare net income with operating cash flow to see whether reported profit is converting into cash from the core business. A persistent gap can point to working-capital pressure, non-cash accounting effects, or earnings-quality questions.