Diluted EPS is earnings per share calculated after adjusting the share-count denominator for potential common shares that could reduce each existing share’s claim on earnings.

The numerator usually starts with earnings available to common shareholders, while the denominator expands from basic weighted-average shares to weighted-average diluted shares when instruments such as options, warrants, convertible securities, or stock-based compensation are dilutive.

Diluted EPS is a dilution-pressure metric, not a standalone verdict on business quality, valuation, or investment attractiveness. It works best when checked against filing assumptions, cash conversion, and earnings quality.

What Diluted EPS Means

Diluted EPS measures how much earnings would be available per common share after including potential shares that could dilute existing shareholders.

The metric answers a narrower question than overall earnings per share: what happens to per-share earnings if instruments that can become common shares are included in the share count?

A lower diluted EPS figure usually means the denominator is larger than the basic share count. The difference is a dilution signal first, not proof that the underlying business is weak.

Diluted EPS Formula

The common diluted EPS formula is:

Diluted EPS = Earnings available to common shareholders ÷ Weighted-average diluted shares

The formula is simple, but the diluted share count is where most interpretation risk sits. The denominator may include securities that could become common shares if their inclusion reduces EPS or increases loss per share in the accounting calculation.

| Formula part | What it represents | Why it matters |

|---|---|---|

| Earnings available to common shareholders | The earnings numerator after preferred dividends or other relevant adjustments where applicable | A distorted numerator can make per-share analysis look cleaner than the business economics support |

| Weighted-average diluted shares | The basic share count plus dilutive potential common shares | This is where dilution normally enters the calculation |

| Diluted EPS result | Earnings spread across a larger potential share base | Shows reported earnings power after possible ownership dilution is reflected |

How Potential Shares Change the Denominator

Diluted EPS focuses on potential common shares. These are instruments that are not always common shares today, but may become common shares or create a similar per-share dilution effect under the calculation.

| Potential dilution source | Possible denominator effect | Plain-English interpretation |

|---|---|---|

| Stock options | May increase diluted shares when exercise would add net shares | Employee or executive options can reduce per-share earnings if they are dilutive |

| Warrants | May add shares if assumed exercise creates dilution | Warrants can act like future share issuance embedded in the capital structure |

| Convertible debt | May increase shares under an if-converted style assumption | Debt that can convert into equity can change both share count and earnings adjustments |

| Convertible preferred stock | May increase common shares if conversion is dilutive | Preferred instruments can dilute common shareholders if they convert into common equity |

| Stock-based compensation | May expand diluted shares depending on award terms and assumptions | Equity compensation can create a recurring gap between basic and diluted share counts |

The key diagnostic is the gap between the basic share count and the diluted share count. A small gap may point to limited current dilution pressure. A large or growing gap can show that future ownership claims may spread across more shares.

Basic EPS vs Diluted EPS

Basic EPS uses the weighted-average common shares actually outstanding during the period. Diluted EPS uses a broader denominator when potential common shares are dilutive.

| Metric | Share-count denominator | Main use |

|---|---|---|

| Basic EPS | Weighted-average common shares outstanding | Shows per-share earnings using the current common share base |

| Diluted EPS | Weighted-average common shares plus dilutive potential common shares | Shows per-share earnings after possible dilution is reflected |

The gap between the two figures matters because the same earnings numerator can produce a lower per-share result when the denominator expands.

Diluted EPS Calculation Example

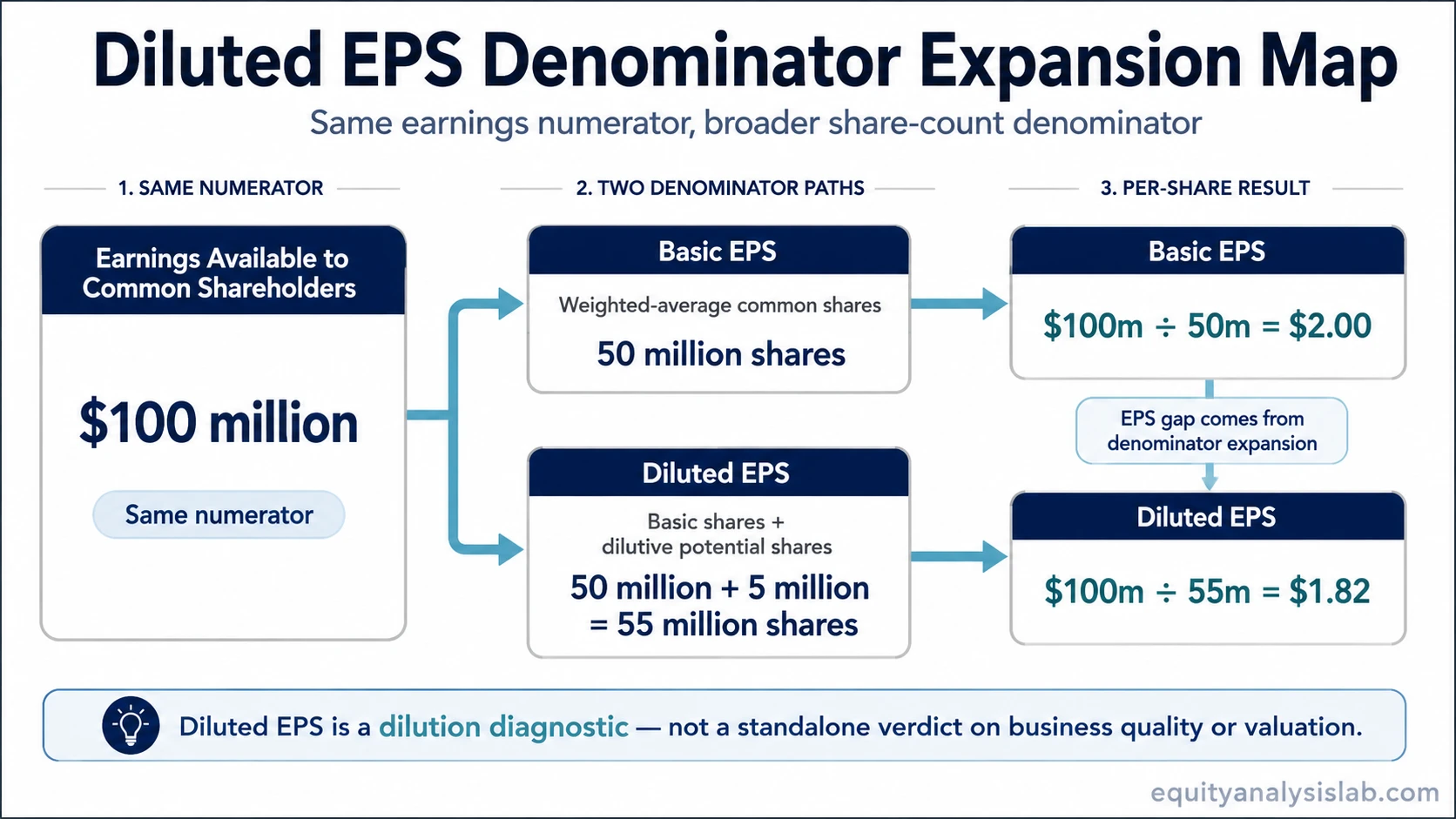

Assume a company reports $100 million of earnings available to common shareholders. Its basic weighted-average share count is 50 million shares. It also has options and convertible instruments that add 5 million dilutive potential shares under the diluted calculation.

| Calculation | Formula | Result |

|---|---|---|

| Basic EPS | $100 million ÷ 50 million shares | $2.00 |

| Diluted EPS | $100 million ÷ 55 million diluted shares | $1.82 |

The earnings numerator did not change in this simplified example. The lower diluted EPS comes from spreading the same earnings across a larger potential share base.

Why Anti-Dilution Matters

Not every potential common share is included in diluted EPS. A security may be excluded when its inclusion would increase EPS or reduce loss per share. In accounting terms, that treatment is anti-dilutive.

This is why diluted EPS is not always lower than basic EPS in every reported period. Some instruments may look dilutive in ordinary language, but the diluted EPS calculation includes them only when they are dilutive under the relevant method and period assumptions.

Anti-dilution is most important when a company has several potential share sources but only some appear in the reported diluted share count. Filing notes can clarify which instruments were included, excluded, or dependent on market price and conversion assumptions.

What Diluted EPS Can Hide

Diluted EPS adds the dilution view, but it does not explain whether the earnings behind the per-share number are durable, cash-supported, or comparable across periods.

| Hidden issue | Why it matters | What to check |

|---|---|---|

| Filing assumptions | The diluted share count depends on the instruments and methods used in the reporting period | EPS note, share-count note, convertible instrument disclosures |

| Stock-based compensation | Reported earnings may look stable while equity compensation increases future dilution pressure | Diluted shares, SBC expense, share repurchases, net issuance |

| Convertible securities | Potential conversion can affect both the denominator and the earnings numerator adjustment | Conversion terms, interest or preferred dividend adjustments, anti-dilutive exclusions |

| Buybacks | Repurchases can offset dilution, but the net share count may still rise if issuance is heavy | Basic shares, diluted shares, repurchase cost, net share change |

| Cash conversion | EPS can look healthy while cash flow support is weak | Operating cash flow, free cash flow, working capital movements |

| Period comparability | A diluted EPS change can reflect share-count timing rather than operating improvement | Weighted-average share count, issuance dates, option exercise assumptions |

A high diluted EPS figure carries more weight when earnings are cash-supported, repeatable, and not being protected by temporary share-count effects. A low or falling diluted EPS figure needs context before it is treated as a business-quality problem.

How to Interpret Diluted EPS

Diluted EPS connects income-statement performance with the share structure behind that performance.

A widening gap between basic EPS and diluted EPS can indicate that potential shares matter more than the basic share count suggests. That gap becomes more important when it persists across periods, rises alongside stock-based compensation, or appears while the company is also issuing shares.

Diluted EPS deserves less weight when the earnings numerator is low quality, nonrecurring, or weakly supported by cash flow. It also needs caution when large potential share pools are excluded as anti-dilutive, because those instruments may become dilutive in a later period if profitability, share price, or conversion economics change.

In multi-year analysis, EPS growth is cleaner when both the earnings numerator and the diluted share count are moving for understandable business reasons rather than temporary accounting or capital-structure effects.

Related Concepts

Basic EPS isolates per-share earnings before diluted potential shares are added to the denominator.

Earnings per share covers the broader per-share profit concept that both basic EPS and diluted EPS build from.

EPS growth adds the time dimension by comparing how per-share earnings change across periods.

FAQ

Is diluted EPS always lower than basic EPS?

Diluted EPS is usually lower when dilutive potential shares are included, but it is not automatically lower in every period. Instruments that would increase EPS or reduce loss per share may be excluded as anti-dilutive.

Why can diluted EPS change even if earnings are stable?

Diluted EPS can change because the denominator changes. New equity awards, option exercises, convertible instruments, buybacks, or weighted-average timing can affect diluted shares even when the earnings numerator is stable.

Does diluted EPS measure business quality?

Diluted EPS does not measure business quality by itself. It becomes more useful when combined with cash conversion, earnings quality, share-count trends, and the assumptions disclosed in company filings.