Tax efficient rebalancing only works as a portfolio maintenance process when lower taxable friction does not leave the portfolio with worse drift, concentration, overlap, or risk exposure.

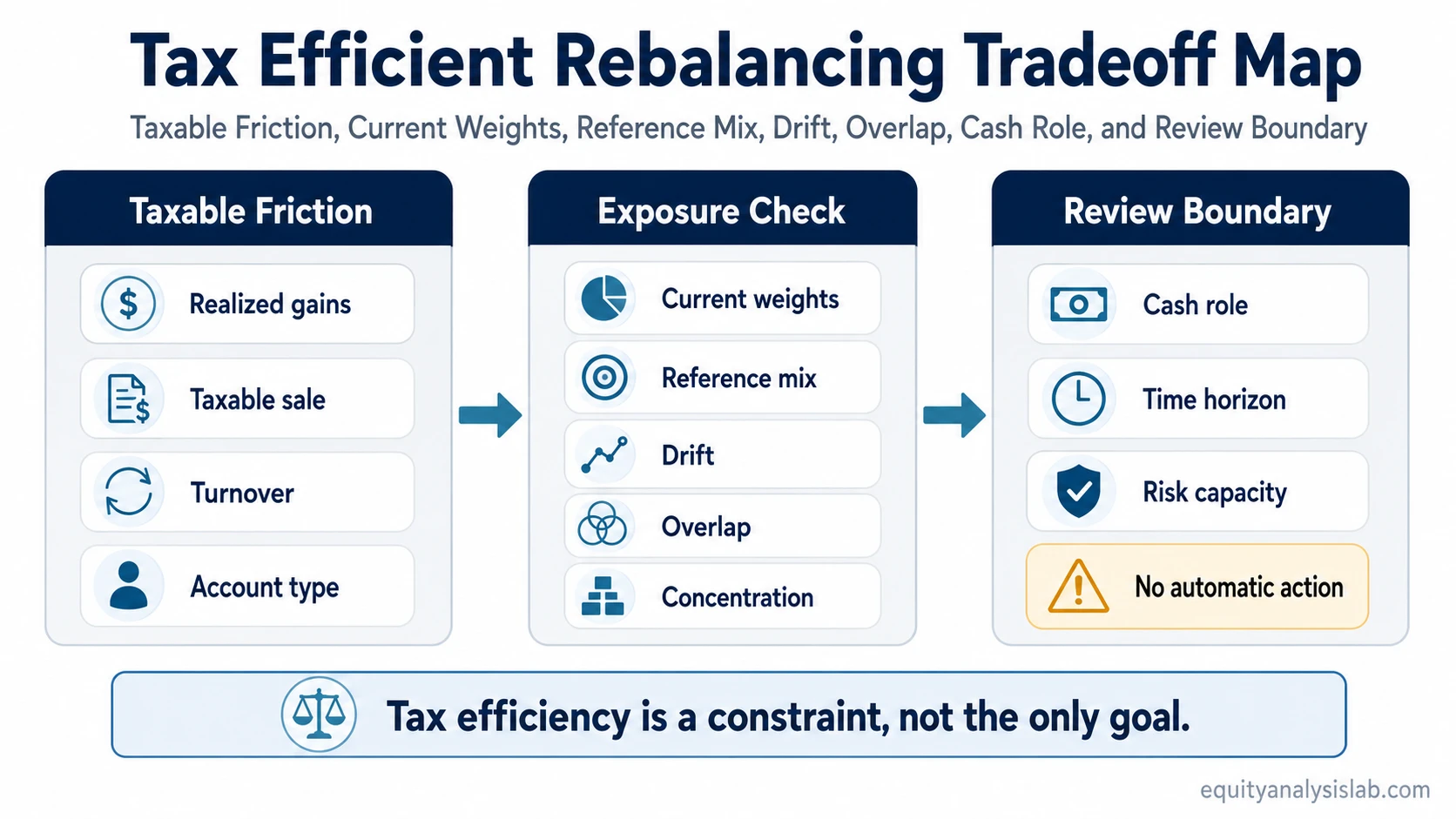

Tax efficient rebalancing is the process of adjusting a portfolio toward intended exposure while trying to reduce unnecessary taxable sales, realized gains, and turnover. The tax result is only one part of the decision. The portfolio still has to be checked against current weights, reference weights, cash role, account type, time horizon, and risk capacity.

Key Points

- Tax efficient rebalancing reduces unnecessary taxable friction, but it does not automatically improve portfolio alignment.

- Avoiding taxable sales can preserve drift, concentration, or overlapping exposures.

- Cash flows, dividends, interest, account type, and asset location can change the least disruptive adjustment path.

- The useful test is whether the portfolio moves closer to intended exposure without creating a larger hidden risk.

What Tax Efficient Rebalancing Means

Tax efficient rebalancing means restoring or improving portfolio exposure while considering the taxable cost of trades. It does not mean avoiding every taxable sale, and it does not mean choosing the lowest-tax action if that action leaves the portfolio poorly aligned.

The process starts with the same basic question as ordinary rebalancing: how far has the portfolio moved away from its intended mix? The tax-aware layer then asks which adjustment path creates less taxable friction while still addressing the exposure problem.

That distinction matters because a taxable account can make rebalancing feel expensive even when the exposure problem is real. A position may be overweight after large gains, a sector may dominate through overlapping holdings, or cash may accumulate while the portfolio becomes less invested than intended.

Why Tax Costs Can Change the Rebalancing Decision

Tax costs enter the rebalancing decision when selling appreciated holdings would realize gains or when frequent turnover would create avoidable taxable events. A tax-aware process may therefore look for lower-friction ways to reduce the imbalance before selling the most tax-sensitive position.

Common inputs include new contributions, dividends, interest, distributions, account type, asset location, and the use of high-basis lots where that information is available. Tax-loss harvesting can also be part of the analysis, but it remains only one input. It does not replace the portfolio exposure review.

A tax-aware adjustment can still be weak if it leaves the investor with the same concentration problem. Reducing tax friction is useful only when the resulting portfolio is closer to the intended risk and exposure profile.

Tax Cost vs Portfolio Drift

The main tension is between realizing a tax cost and allowing drift from target weights to remain unresolved. Delaying a sale may reduce taxable friction today, but the portfolio can stay overweight in the same asset, sector, factor, or theme.

This is why tax efficient portfolio rebalancing needs an exposure check before it becomes a tactic list. The question is not only whether a trade creates taxes. The question is whether the portfolio is still aligned after taxes, cash flows, and substitute adjustments are considered together.

| Tax-aware choice | Possible portfolio effect | Limitation to check |

|---|---|---|

| Use new contributions to underweight areas | Reduces the need to sell appreciated holdings | May be too small to correct a large overweight position |

| Redirect dividends, interest, or distributions | Gradually moves exposure toward the intended mix | Works slowly if the portfolio has significant drift |

| Sell higher-basis lots first | May reduce realized gain compared with selling low-basis shares | Does not solve concentration if too little exposure is reduced |

| Use cash as the adjustment source | Can rebalance without selling appreciated assets | May create or maintain too much idle cash if not sized deliberately |

| Delay a taxable sale | Avoids immediate taxable friction | Can preserve unwanted drift, overlap, or concentration |

Inputs to Check Before Making a Tax-Aware Adjustment

A useful tax-aware review separates the tax issue from the exposure issue. The tax issue asks what taxable event may occur. The exposure issue asks what the portfolio looks like if that action is taken, delayed, or replaced with a lower-friction alternative.

| Input | What it shows | Why it matters |

|---|---|---|

| Current holdings | Which positions and funds create exposure | Overlap may hide concentration across different holdings |

| Current weights | How much each holding or category now represents | Weights show whether the portfolio has moved away from its reference mix |

| Reference weights | The intended mix used for comparison | Without a reference, tax efficiency can become detached from portfolio purpose |

| Cash flows | New contributions, withdrawals, dividends, and interest | Cash flows may reduce the need for taxable selling |

| Account type and asset location | Where the asset is held | Taxable and tax-advantaged accounts may create different adjustment options |

| Time horizon and risk capacity | How much exposure mismatch can be tolerated | Large drift may matter more when the portfolio is near a liquidity need or risk boundary |

The useful comparison is not “tax cost or no tax cost.” It is whether the lower-friction path leaves the portfolio acceptably close to its reference mix after weights, cash, overlap, and concentration are checked together.

The Cash Role in Tax Efficient Rebalancing

Cash can make tax-aware rebalancing less disruptive when it is used deliberately. Contributions, dividends, interest, and distributions can be directed toward underweight areas instead of selling appreciated positions first.

The same cash choice can create a separate problem if the portfolio cash position becomes larger than the investor’s intended liquidity buffer. Cash can reduce turnover, but it also changes the denominator of the portfolio and may lower the intended exposure to risk assets.

This is where tax efficiency and cash drag can overlap. Holding cash to avoid taxable sales may be reasonable in some situations, but idle cash still needs a role, a size, and a review trigger.

A Common Mistake: Avoiding Taxes While Keeping the Same Risk

Common mistake: treating a lower-tax choice as a better portfolio choice before checking what exposure remains after the decision.

For example, a portfolio can become overweight in one asset category after several years of gains. Selling part of the overweight position may create taxable gains, so the sale is delayed. That may reduce taxable friction in the short term, but the portfolio is still overweight unless new cash, dividends, other account adjustments, or a phased reduction actually reduce the imbalance.

The same issue can appear through overlapping funds. Several holdings may look diversified by name but still share similar underlying exposure. In that case, avoiding taxable sales can preserve a larger concentration than the top-level holding list suggests.

What Tax Efficient Rebalancing Does Not Prove

Limitation: tax efficient rebalancing does not prove that the portfolio is safer, better diversified, or better aligned. It only describes the attempt to reduce unnecessary taxable friction while making a maintenance decision.

A low-tax adjustment can still leave too much exposure in one company, sector, fund family, factor, country, or asset class. A higher-tax adjustment may still enter the review when the exposure problem is large, but that kind of tradeoff depends on individual tax facts and cannot be resolved by a generic rule.

The practical boundary is simple: tax efficiency is a constraint, not the only goal. The final portfolio shape still has to be evaluated on weights, overlap, concentration, liquidity needs, time horizon, and risk capacity.

How to Read Tax-Efficient Rebalancing Strategies

Tax-efficient rebalancing strategies are better understood as adjustment paths, not automatic recommendations. New cash, dividends, high-basis lots, tax-loss harvesting, charitable giving, and phased sales may all appear in the discussion, but each one changes the portfolio differently.

The safer reading is diagnostic. First identify the exposure problem. Then identify which taxable event the adjustment might create. Then compare whether lower-friction alternatives move the portfolio close enough to the intended mix without creating a larger drift or concentration problem.

When the tax facts are specific, the educational framework stops at the process level. Jurisdiction, account structure, tax lots, holding period, income situation, and charitable intent can materially change the result.

FAQ

Can tax efficient rebalancing leave a portfolio poorly aligned?

Yes. Avoiding taxable sales can preserve an overweight position, overlapping exposure, or unintended drift. A lower-tax path is useful only if the resulting portfolio remains close enough to the intended exposure.

Is tax-loss harvesting the same as tax efficient rebalancing?

No. Tax-loss harvesting can be one tax-aware input, but tax efficient rebalancing is broader. It compares tax friction with the portfolio’s current weights, target mix, cash flows, concentration, and risk boundaries.