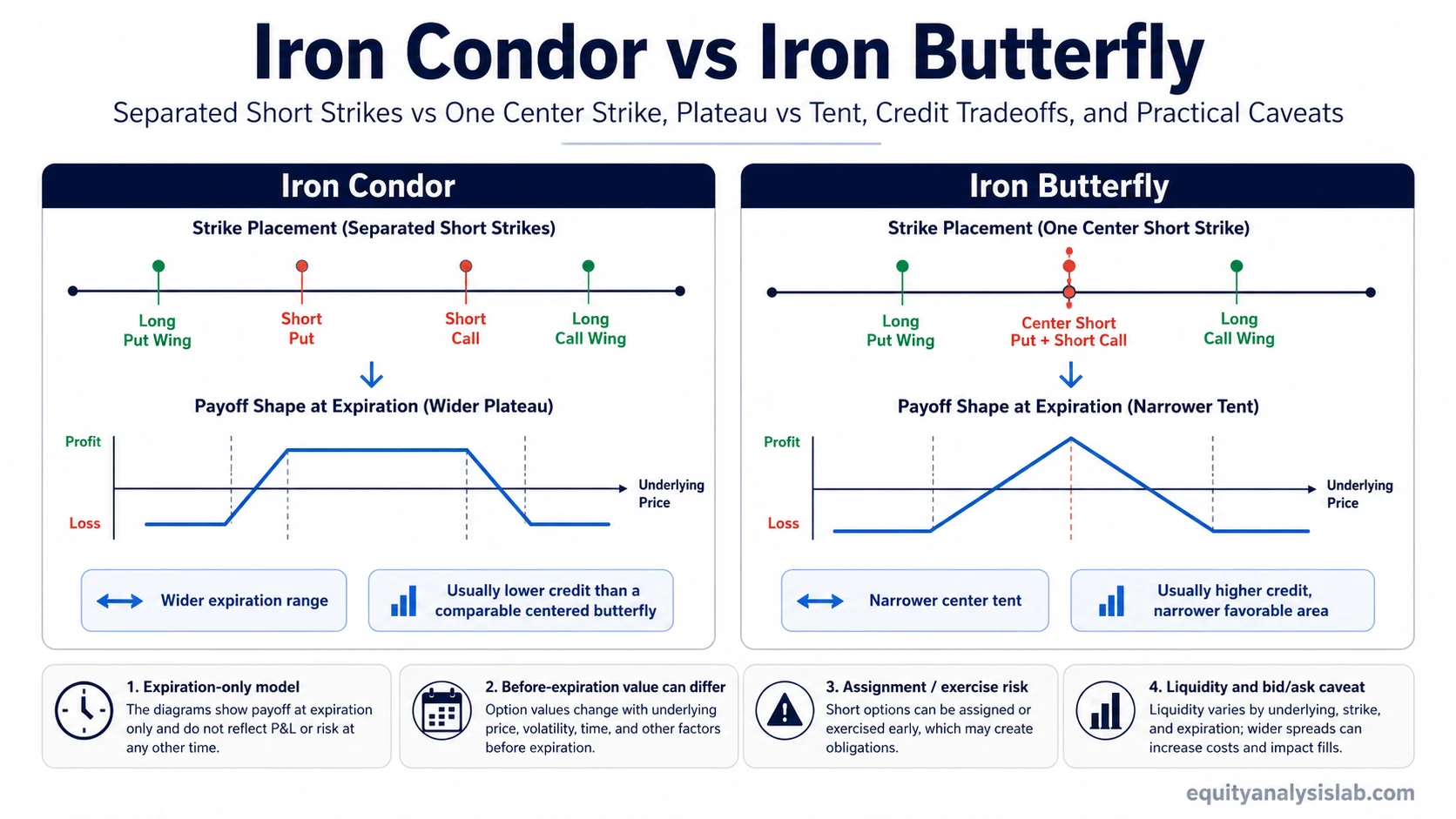

Iron condor vs iron butterfly compares two four-leg, defined-risk credit structures. An iron condor separates the short call and short put strikes to create a wider expiration range, while an iron butterfly places both short options at the same center strike, usually creating a narrower payoff tent and larger credit.

Both structures combine a short call spread and a short put spread around the same expiration. The difference is not that one is automatically better or safer. The difference is the question the structure asks: whether the underlying can remain inside a wider short-strike range, or whether it can settle near one center strike at expiration.

Payoff diagrams for both structures are simplified expiration views. Before expiration, option value can behave differently because implied volatility, time decay, option Greeks, liquidity, bid/ask spreads, and assignment or exercise risk can affect the live position value.

Key Points

- An iron condor uses separated short strikes, while an iron butterfly uses one center short strike for the short call and short put.

- The iron condor usually has a wider expiration range between the short strikes, while the iron butterfly usually has a narrower payoff tent around the center strike.

- The iron butterfly usually collects more credit because the short options are closer to the center of the price distribution, but that credit comes with a narrower favorable expiration area.

- The iron condor usually collects less credit but gives the underlying more room between the short strikes before expiration payoff begins to deteriorate.

- Static payoff maps are expiration-only models; live option value before expiration can change because of volatility, time value, liquidity, and short-option assignment or exercise risk.

Iron Condor vs Iron Butterfly: The Core Difference

The core difference is short-strike placement. An iron condor places the short put and short call at different strikes, with long wings farther outside those short strikes. This creates a defined-risk structure with a range between the short strikes where the expiration payoff is usually most favorable.

An iron butterfly places the short put and short call at the same center strike, with a long put wing below and a long call wing above. This creates a more concentrated expiration payoff shape, where the most favorable simplified expiration outcome is centered near that shared short strike.

The shared category can make the two structures look similar. Both use four option legs, both have defined maximum loss in the standard short-credit construction, and both are often shown with payoff diagrams. The structural difference changes the payoff shape, the credit profile, the breakeven logic, and the type of price behavior the expiration model is describing.

Iron Condor vs Iron Butterfly Comparison Table

| Comparison point | Iron condor | Iron butterfly |

|---|---|---|

| Short strike placement | Short put and short call are placed at different strikes. | Short put and short call are placed at the same center strike. |

| Long wing placement | Long put is below the short put; long call is above the short call. | Long put is below the center strike; long call is above the center strike. |

| Payoff shape at expiration | Wider plateau between the two short strikes. | Narrower tent centered on one short strike. |

| Net credit profile | Usually lower credit than a comparable centered iron butterfly. | Usually higher credit because the short options are concentrated near the center strike. |

| Expiration range tolerance | Usually wider, because the underlying can finish between separated short strikes. | Usually narrower, because the simplified best expiration area is concentrated near one strike. |

| Main tradeoff in the model | More room, usually less credit. | More credit, usually less room. |

Same Underlying, Different Strike Placement

Both structures are often built on the same underlying asset and the same expiration date. The difference is how the strikes are distributed around the current price or selected reference area.

In a standard short iron condor, the short put is below the short call. The long put is farther below the short put, and the long call is farther above the short call. The distance between the short strikes creates the central range in the simplified expiration payoff map.

In a standard short iron butterfly, the short put and short call share one center strike. The long put sits below that center strike, and the long call sits above it. The structure is still defined risk, but the simplified expiration payoff becomes more concentrated around the center.

Simple distinction: the iron condor spreads the short strikes apart; the iron butterfly concentrates both short options at one center strike.

Payoff Range, Credit, and Expiration Boundary

The payoff range is the most visible difference. An iron condor usually produces a flatter expiration plateau between the short put and short call. If the underlying finishes inside that range at expiration, the simplified payoff model usually shows the position near its most favorable area.

An iron butterfly usually produces a narrower tent. The highest simplified expiration payoff is centered near the shared short strike, while payoff declines as the underlying finishes farther away from that center, until the long wings define the outer risk boundary.

The credit difference comes from strike placement. Because the iron butterfly sells both short options at the center strike, it usually receives more credit than an otherwise comparable iron condor. That higher credit is not a free advantage. It normally comes with a narrower favorable expiration area.

The iron condor usually receives less credit because the short strikes are farther apart, but the structure gives the underlying more room before the expiration payoff begins to deteriorate. This is why the comparison is better framed as a range-versus-credit tradeoff, not as a ranking of one structure over the other.

Before-Expiration Caveats

Static payoff diagrams can be useful, but they are not full live-position models. A payoff diagram usually shows a simplified expiration result. Before expiration, option prices still contain time value and can respond to implied volatility, skew, interest rates, dividends where relevant, and changing supply and demand for the contracts.

Greeks can also make the live position behave differently from the final expiration shape. Delta, gamma, theta, and vega can shift as price, time, and volatility change. A structure that looks simple on an expiration diagram can therefore have a different mark-to-market value before expiration.

Liquidity matters as well. Wide bid/ask spreads, uneven open interest, and poor execution quality can affect the practical value of either structure. Assignment and exercise mechanics can also matter when short options are in the money, near expiration, or affected by dividend or early-exercise considerations.

Limitation: the comparison describes structural payoff logic, not a recommendation to use either structure. Real option pricing and position management depend on contract selection, timing, liquidity, volatility, and account-level constraints.

Common Confusion

A common confusion is to treat both structures as interchangeable because both combine a call spread and a put spread. The shared four-leg construction matters, but the short-strike location changes the economic shape of the position.

The iron condor is better understood as a structure with separated short strikes and a wider central expiration range. The iron butterfly is better understood as a structure with one center short strike and a narrower, more concentrated expiration tent.

Another confusion is to read the higher credit of an iron butterfly as automatically superior. In the simplified model, higher credit is paired with less room around the center strike. The better comparison is how the payoff shape changes, not whether one label sounds more attractive.

Related Structures

Both structures belong to a broader group of multi-leg options spreads. A credit spread explains the simpler two-leg building block behind one side of the position, while a debit spread shows the opposite premium-flow version of a defined-risk spread.

The comparison also connects to options spread structure more broadly, because both examples show how combining multiple option legs can reshape payoff boundaries, premium exposure, and expiration outcomes.

FAQ

Is an iron condor the same as an iron butterfly?

No. Both are four-leg, defined-risk credit structures in their standard short forms, but an iron condor uses separated short strikes while an iron butterfly uses the same center short strike for the short call and short put.

Why does an iron butterfly usually collect more credit?

An iron butterfly usually collects more credit because the short call and short put are both placed at the center strike, often closer to the underlying price. That higher credit is paired with a narrower simplified expiration payoff area.

Why does an iron condor usually have a wider expiration range?

An iron condor usually has a wider expiration range because the short put and short call are placed at different strikes. In the simplified expiration model, the structure is usually most favorable when the underlying finishes between those short strikes.

Do payoff diagrams show live option value before expiration?

No. Payoff diagrams usually simplify the structure at expiration. Before expiration, option value can change because of price movement, implied volatility, time decay, Greeks, liquidity, bid/ask spreads, and short-option assignment or exercise risk.