How often should you rebalance your portfolio depends on whether the portfolio has drifted far enough from its intended exposure to justify action. Many investors review on a calendar schedule, such as annually or semiannually, but the actual rebalance decision should also consider weight drift, concentration, overlap, costs, taxes, time horizon, and risk capacity.

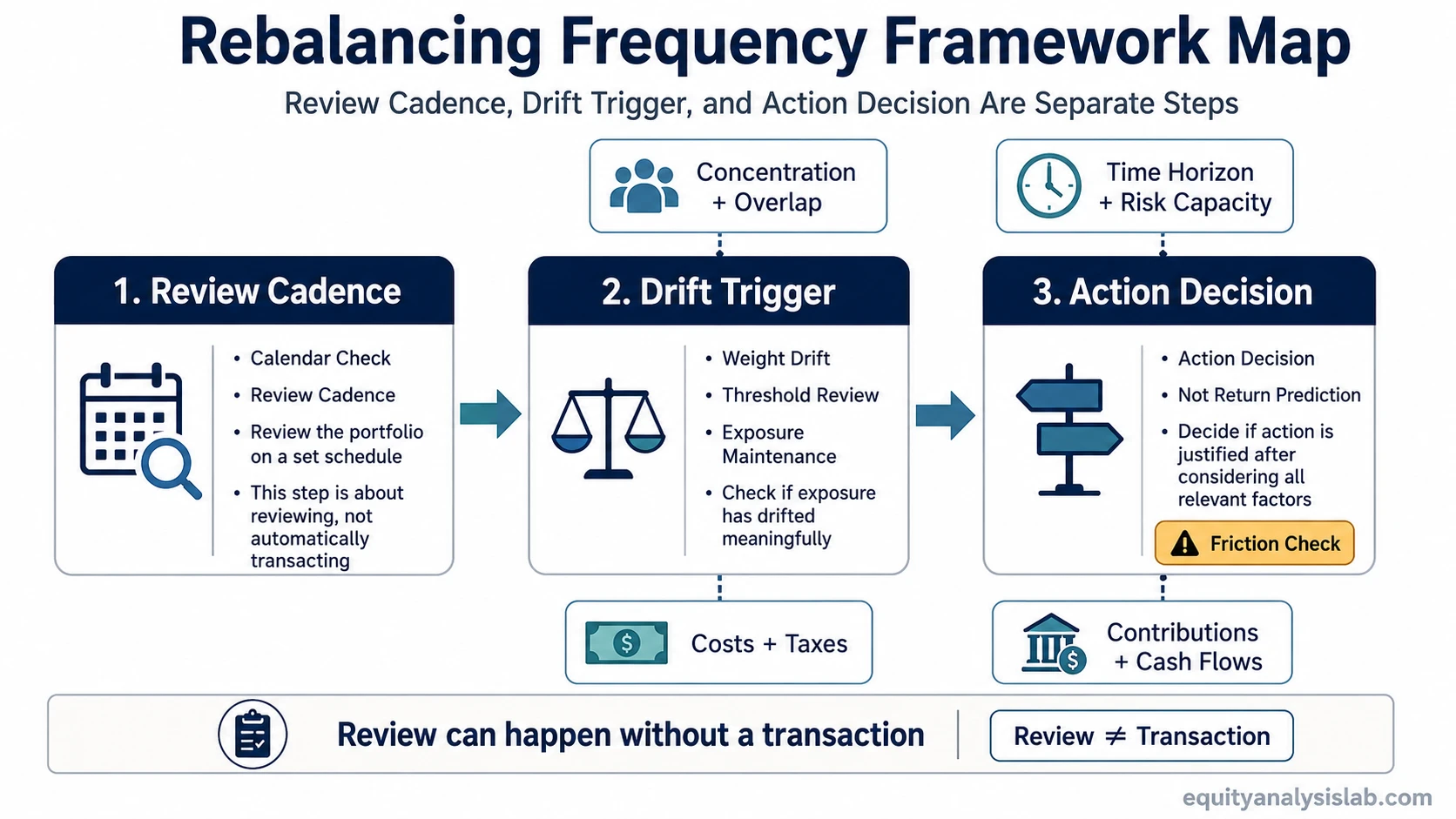

Rebalancing frequency is best separated into three decisions: when to check the portfolio, what level of drift is large enough to matter, and whether action is still justified after frictions and portfolio purpose are considered. A review can happen without a portfolio transaction. A drift signal can appear without requiring immediate action. A rebalance becomes more defensible only when the actual exposure has moved far enough away from the intended mix to change the portfolio’s risk profile.

Key Points

- Annual or semiannual review may be enough in some long-term portfolios when actual weights remain close to the intended mix, but the review date should not automatically force a rebalance.

- Threshold-based rebalancing focuses on how far actual weights have moved from target weights.

- A hybrid method combines scheduled reviews with drift thresholds, so small market noise does not trigger unnecessary activity.

- Large weight drift, hidden overlap, rising concentration, changing risk capacity, taxes, and transaction costs can all change the answer.

- Rebalancing manages exposure drift. It does not predict returns, remove risk, or create a universal best schedule.

How Often Should You Rebalance Your Portfolio?

A practical starting point is to review the portfolio on a fixed schedule, then rebalance only if the actual exposure has moved meaningfully away from the intended mix. For some portfolios, that may mean an annual review with action only when weights cross a threshold. For portfolios with larger positions, concentrated holdings, volatile assets, or changing cash flows, more frequent review may be useful, but review frequency still does not equal a requirement to adjust the portfolio.

The intended mix comes from asset allocation. Rebalancing checks whether the portfolio still resembles that intended mix after price moves, contributions, withdrawals, dividends, or new purchases have changed the weights.

Rebalancing Frequency Is Not the Same as a Rebalancing Trigger

The most common mistake is treating the calendar as the decision. A calendar review only says when to look. A trigger says what has changed enough to deserve attention. The final action depends on whether the drift is material after costs, taxes, risk capacity, and portfolio role are considered.

| Decision layer | Question it answers | What to check | What it does not decide by itself |

|---|---|---|---|

| Review cadence | When should the portfolio be checked? | Annual, semiannual, quarterly, or event-based review dates | Whether a portfolio transaction is necessary |

| Trigger | Has exposure drifted far enough to matter? | Actual weights versus target weights, tolerance bands, concentration, and overlap | Whether the cost of acting is justified |

| Action | Should the portfolio actually be rebalanced? | Costs, taxes, account type, available cash flows, time horizon, and risk capacity | Future return direction or market timing |

This sequence keeps the decision focused on exposure maintenance. A portfolio can be reviewed frequently while being rebalanced rarely. It can also need attention before the next calendar date if a large holding or asset class has moved enough to change the portfolio’s behavior.

Calendar, Threshold, and Hybrid Rebalancing

Most rebalancing frequency decisions fit into three broad approaches: calendar review, threshold review, or a hybrid of both. The right framework depends less on finding a perfect date and more on matching review discipline to the way the portfolio can drift.

| Method | What it checks | When it helps | Main limitation |

|---|---|---|---|

| Calendar review | The portfolio is checked on a fixed schedule, such as annually, semiannually, or quarterly. | Useful when the portfolio is broadly diversified, trading costs matter, and the investor wants a simple review process. | A fixed date may lead to action even when drift is small, or miss meaningful drift between review dates. |

| Threshold trigger | The portfolio is checked against tolerance bands around target weights. | Useful when the investor wants action to depend on actual drift rather than the calendar alone. | Very tight thresholds can create unnecessary turnover when small price moves have little impact on portfolio role. |

| Hybrid method | The portfolio is reviewed on a schedule, but action is considered only when drift crosses a meaningful threshold. | Useful when the goal is to avoid both neglect and overtrading. | The thresholds still need to reflect portfolio size, tax friction, concentration, and risk capacity. |

A hybrid method often gives the cleanest decision structure because it separates observation from action. The calendar creates discipline. The threshold prevents small market movement from becoming unnecessary portfolio activity.

What Changes the Right Rebalancing Frequency?

The right rebalancing frequency changes when the portfolio’s actual exposure can move away from its intended exposure quickly or materially. A portfolio with a few large positions may need closer review than a broad index-style portfolio because one strong or weak holding can change the risk profile faster.

Concentration is one of the clearest examples. A position can become larger because it rises more than the rest of the portfolio, because new money keeps flowing into the same area, or because several holdings depend on the same underlying driver. That kind of portfolio concentration can change how often the weights deserve review.

Overlap matters as well. A portfolio can own many holdings while still depending on the same sector, factor, region, business model, or currency exposure. When several positions move together, the spread of exposure may be weaker than the holding count suggests.

Observable inputs before rebalancing:

- Target weights: the intended mix the portfolio is being checked against.

- Current weights: the actual weights after price movement, contributions, withdrawals, dividends, and new purchases.

- Tolerance bands: the amount of drift that is large enough to review seriously.

- Dominant holdings: positions that now drive more of the portfolio than intended.

- Hidden overlap: repeated exposure to the same sector, factor, country, currency, or business model.

- Account type and friction: trading costs, tax consequences, and whether action can be done through new contributions or cash flows.

- Time horizon and risk capacity: whether the portfolio can still tolerate the exposure it now carries.

Common Mistakes When Deciding How Often to Rebalance

Mistake 1: Treating every review date as an action date. A scheduled review should identify whether anything has changed enough to matter. If drift is small and costs or taxes are meaningful, the review may end with no rebalance.

Mistake 2: Using holding count as a substitute for exposure review. A portfolio with many holdings can still be concentrated if the largest positions, sectors, or factors dominate the results.

Mistake 3: Rebalancing every small movement. Tight reactions to normal price movement can create unnecessary turnover without improving the portfolio’s exposure discipline.

Mistake 4: Ignoring new cash flows. Contributions, dividends, and withdrawals can sometimes reduce drift without selling existing positions.

Mistake 5: Treating rebalancing as a market forecast. Rebalancing can reduce unintended exposure drift, but it does not say which asset will outperform next.

When Less Frequent Rebalancing Can Be Reasonable

Less frequent rebalancing can be reasonable when the portfolio remains close to its intended weights, holdings are broadly spread across different exposures, trading costs or taxes are meaningful, and the investor’s time horizon has not changed. A long-term portfolio does not need to react to every small price movement if the actual risk profile remains close to the intended one.

Less frequent action does not mean ignoring the portfolio. The distinction is between checking and portfolio transactions. A review can confirm that the portfolio is still inside acceptable ranges, that no single exposure has become dominant, and that the cost of acting would outweigh the benefit of forcing the portfolio back to an exact target.

When More Frequent Review Can Be Useful

More frequent review can be useful when a portfolio has large single positions, volatile assets, concentrated sector exposure, changing cash flows, or a shorter time horizon than before. It can also be useful when risk capacity changes because the portfolio’s role has changed, the investor is closer to needing the funds, or a previously acceptable drawdown range no longer fits the situation.

More frequent review still does not mean automatic rebalancing. It simply means the portfolio has more ways to drift away from its intended exposure. The action decision remains conditional on the size of the drift, the reason for the drift, the cost of adjustment, and whether cash flows can reduce the imbalance without selling.

A Simple Drift Example

Consider a portfolio that starts with a 60% stock allocation and a 40% bond allocation. After a strong equity period, stocks rise to 68% and bonds fall to 32%. The calendar review identifies the change, but the action decision depends on the investor’s tolerance band, account type, tax friction, costs, time horizon, and whether new contributions can move the portfolio closer to the intended mix.

The 68/32 mix is not automatically a rebalance command. It is a drift signal that should be checked against the investor’s tolerance band, account type, tax friction, costs, time horizon, and risk capacity. If new contributions are still being added, part of the imbalance may be reduced by directing new cash toward the underweight side instead of immediately selling the overweight side.

When Rebalancing Too Often Can Create Problems

Rebalancing too often can turn a risk-control process into unnecessary portfolio activity. Small movements around target weights may not change the portfolio’s real behavior, especially when trading costs, bid-ask spreads, taxable gains, or administrative complexity are material.

Too-frequent rebalancing can also create false precision. A portfolio does not become safer simply because every weight is pushed back to an exact target after every movement. The better question is whether the drift has changed the portfolio’s role, risk exposure, concentration, or ability to tolerate drawdowns.

How Rebalancing Connects to Portfolio Exposure

Rebalancing frequency is one part of portfolio exposure control. The calendar answers when to check. The threshold answers whether the current mix has moved far enough to matter. The action decision answers whether adjusting the portfolio is worth the friction.

The strongest rebalancing process starts with the intended allocation, measures actual weights, checks for hidden concentration and overlap, then considers whether costs, taxes, cash flows, time horizon, and risk capacity justify action. That keeps rebalancing focused on exposure maintenance rather than prediction.

Limits of Rebalancing Frequency Rules

Rebalancing frequency rules are decision aids, not guarantees. They cannot predict which asset will perform best, remove market risk, prevent drawdowns, or create a universal schedule that fits every portfolio.

Tax treatment, account structure, transaction costs, liquidity, and personal constraints can materially change the decision. Any tax-specific or account-specific question needs separate review from an appropriate professional. The educational framework here is limited to portfolio exposure, drift, and review discipline.

FAQ

Is annual rebalancing enough?

Annual rebalancing review can be enough for some long-term portfolios if actual weights remain close to intended weights and no exposure has become dominant. Annual review should not automatically force a rebalance if drift is small or the cost of acting is high.

What is the difference between calendar and threshold rebalancing?

Calendar rebalancing checks the portfolio on a fixed schedule. Threshold rebalancing looks for drift beyond a chosen tolerance band. A hybrid method uses scheduled reviews but only considers action when drift is meaningful.

Can new contributions be used instead of selling?

New contributions, dividends, or cash flows can sometimes reduce drift by adding to underweight areas instead of selling overweight areas. Whether that is appropriate depends on the size of the drift, costs, taxes, and portfolio constraints.