NAV and market price can appear together on an ETF quote, but they answer different questions. NAV estimates the per-share value of the fund’s holdings after liabilities, while market price is the exchange-traded price of the ETF share.

The difference matters because an ETF has two layers at the same time: a portfolio value inside the fund and a tradable share price in the market. Those two values are related, but they are not identical, and neither one should be treated as a standalone investment signal.

Key Points

- NAV estimates the ETF’s per-share fund value.

- Market price is the ETF share price formed on the exchange during market hours.

- The two can differ because market price moves intraday while official NAV is generally calculated after market close.

- Premiums and discounts need context; they are not automatic investment signals.

What Is the Difference Between NAV and Market Price?

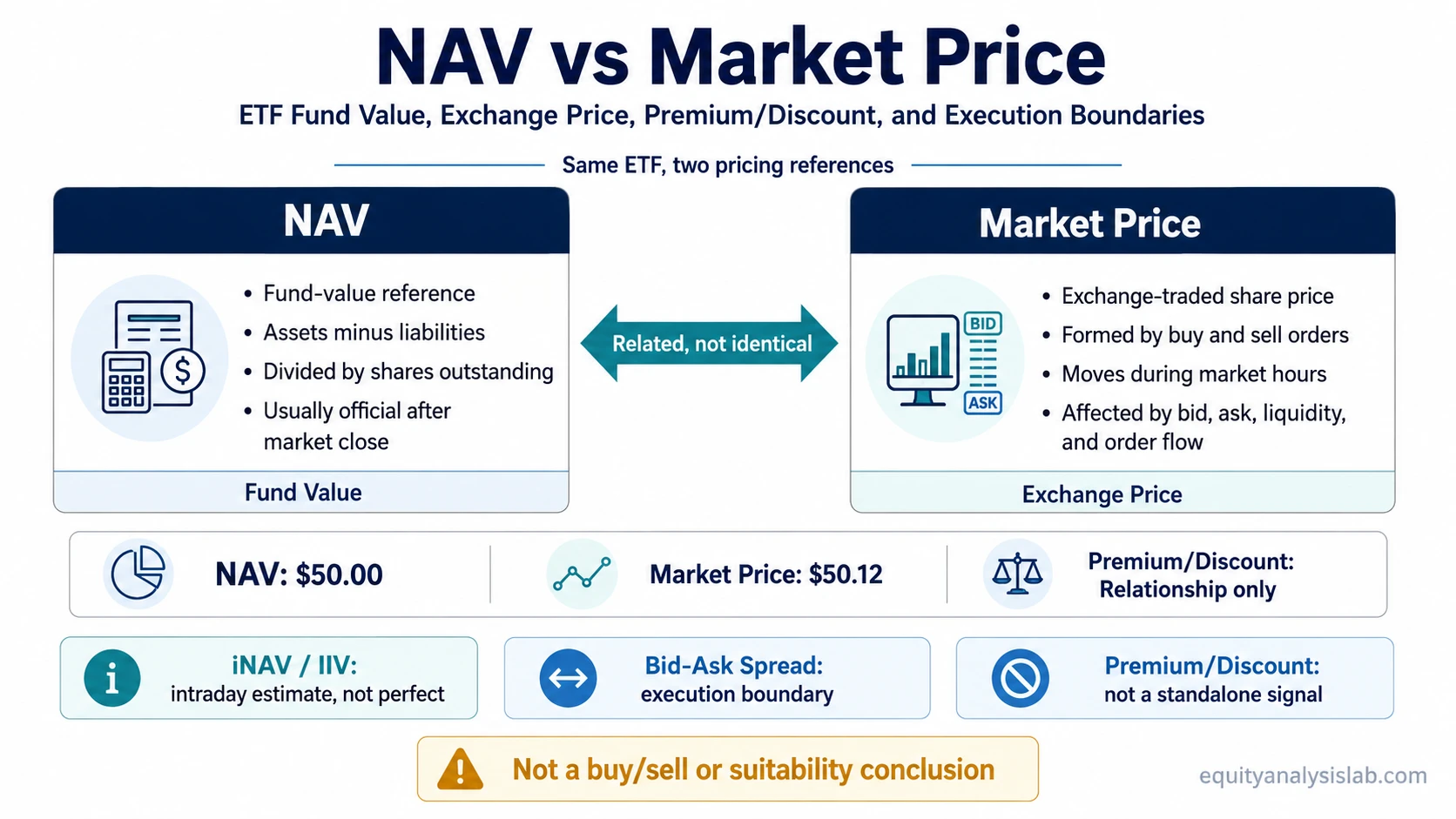

NAV is the fund-value side of the ETF. It is commonly calculated as the value of the ETF’s assets minus liabilities, divided by the number of ETF shares outstanding. In simple terms, it estimates what each ETF share represents in the underlying fund portfolio.

Market price is the exchange-price side of the ETF. It is set by buyers and sellers during trading hours, so it can move as orders, liquidity, sentiment, and intraday changes in the underlying holdings change.

The practical distinction is this: NAV helps describe fund value, while market price describes the secondary-market price. A quote may show both values, but the trade itself is not automatically executed at NAV.

NAV vs Market Price Comparison

| Comparison point | NAV | Market price |

|---|---|---|

| What it measures | Estimated per-share value of the ETF’s net assets. | Exchange-traded price of the ETF share. |

| Basic calculation or source | Fund assets minus liabilities, divided by shares outstanding. | Determined by buy and sell orders on the exchange. |

| When it updates | Usually calculated after market close for the official daily NAV. | Moves throughout the trading day while the exchange is open. |

| Who or what determines it | Fund accounting process based on the value of the underlying portfolio. | Market participants trading ETF shares in the secondary market. |

| How investors use it | As a reference point for fund value and premium/discount analysis. | As the exchange price reference for ETF trades, alongside the current bid and ask. |

| Main limitation | Can be stale during the trading day or less precise when holdings are hard to price. | Can be affected by liquidity, order flow, and the bid-ask spread. |

| Common confusion | Treating NAV as the guaranteed execution price. | Treating market price as proof that the fund’s holdings changed by the same amount. |

Why NAV and Market Price Can Differ

NAV and market price can differ because they update through different mechanisms. Official NAV is tied to fund accounting, while market price changes through exchange trading. During the trading day, the secondary-market price may move before the official NAV is recalculated.

When market price is above NAV, the ETF is commonly described as trading at a premium. When market price is below NAV, it is commonly described as trading at a discount. A premium or discount is a relationship between two values, not a complete conclusion by itself.

ETF creation and redemption can help explain why large gaps often face pressure. Authorized participants can create or redeem large blocks of ETF shares with the issuer, usually using a basket of securities, cash, or both. That mechanism can help connect ETF shares with the underlying portfolio value, but it does not mean every premium or discount disappears instantly or without trading frictions.

Example: Same ETF, Different NAV and Market Price

Suppose an ETF’s official NAV was $50.00 per share after the previous close, and the same ETF trades at $50.12 during the next session.

In that same quote environment, the two numbers do different jobs. The $50.00 NAV is the fund-value reference. The $50.12 market price is the quoted trading price at that moment. The difference may reflect intraday changes, trading demand, spreads, liquidity, or timing differences in how the holdings are valued.

The example does not mean the ETF is automatically attractive or unattractive. It only shows why fund value and exchange price can sit close together without being the same number.

Common Mistakes When Comparing NAV and Market Price

- Assuming NAV is the execution price: NAV is a fund-value estimate, not a guarantee that an investor can trade at that number.

- Assuming market price proves the holdings changed: market price can move because of order flow, liquidity, and trading conditions, not only because the underlying assets changed.

- Calling every discount an opportunity: a discount may reflect timing, liquidity, stale pricing, or market stress, not necessarily a mispriced bargain.

- Calling every premium overvaluation: a premium may reflect intraday demand, hard-to-price holdings, or market access conditions, not a complete valuation judgment.

- Ignoring spread and liquidity: a narrow premium or discount can be less important than poor execution conditions if the quoted spread is wide.

NAV, iNAV, Bid-Ask Spread, and Execution Limits

Official NAV is usually a point-in-time value. For ETFs holding international securities, bonds, less-liquid assets, or fast-moving instruments, the official NAV can lag the live market environment. That is one reason a small gap between NAV and market price should be interpreted with caution.

Some ETF data sources show an intraday indicative value, often called iNAV or IIV. This can provide a live estimate of portfolio value during the trading session, but it is still an estimate. It may not perfectly capture every holding, every liquidity condition, or every pricing delay.

The bid and ask matter because market price is not a single frictionless number. An investor looking at an ETF quote may see a last traded price, a bid, an ask, NAV, and sometimes iNAV/IIV at the same time. Those values help describe different parts of the pricing picture.

What NAV vs Market Price Does Not Tell You

NAV versus market price does not determine whether an ETF is suitable, cheap, liquid, tax-efficient, diversified, or likely to perform well. It only explains the relationship between fund value and exchange price.

A careful interpretation also needs fund structure, underlying holdings, trading volume, spreads, creation/redemption mechanics, and the pricing quality of the assets inside the ETF. Without that context, a premium or discount can be easy to overread.

FAQ

Is NAV the price I pay for an ETF?

No. NAV estimates the ETF’s per-share fund value, while an ETF trade happens at a market price on the exchange. The two values are related, but they are not automatically the same.

Why can an ETF trade above or below NAV?

An ETF can trade above or below NAV because market price moves during the trading day while official NAV is generally calculated after market close. Liquidity, order flow, pricing delays, and creation/redemption mechanics can all affect the gap.

Is market price more important than NAV?

Market price is important for execution because it is the price investors can trade at. NAV is important as a fund-value reference. The stronger interpretation comes from comparing both values rather than treating one as universally more important.

What is iNAV or IIV?

iNAV or IIV is an intraday indicative estimate of an ETF’s portfolio value. It can help during the trading day, but it is not a perfect real-time substitute for official NAV or actual execution price.