Basic EPS and diluted EPS both measure earnings per common share, but they answer different share-count questions. Basic EPS uses the current weighted-average common-share count. Diluted EPS includes potential shares from dilutive securities when those shares would reduce EPS.

The difference matters because the numerator may be similar while the denominator changes. A company can report the same earnings available to common shareholders, yet diluted EPS can be lower because the calculation spreads those earnings across a larger possible share base.

For the standalone calculation, see basic EPS. For the potential-share version, see diluted EPS.

Basic EPS vs Diluted EPS: The Core Difference

Basic EPS focuses on the common shares currently outstanding on a weighted-average basis. Diluted EPS asks what EPS would look like if dilutive potential common shares were included in the share count.

| Criterion | Basic EPS | Diluted EPS | Investor interpretation |

|---|---|---|---|

| Share base | Weighted-average common shares | Weighted-average common shares plus dilutive potential common shares | The main difference is usually the denominator, not the profit figure itself. |

| Securities included | Common shares already in the basic share count | Options, warrants, convertible debt, convertible preferred shares, and relevant equity compensation when dilutive | Diluted EPS reflects possible ownership dilution from instruments that could become common shares. |

| Formula denominator | Current weighted-average common shares | Weighted-average common shares adjusted for dilutive potential shares | A wider denominator can lower per-share earnings even when earnings are unchanged. |

| Capital structure fit | Most straightforward for companies with simple share structures | More relevant when options, warrants, convertibles, or stock-based compensation are material | The more complex the capital structure, the more useful the diluted comparison becomes. |

| Typical value relationship | Usually higher than or equal to diluted EPS | Usually lower than or equal to basic EPS | Diluted EPS is normally lower than or equal to basic EPS because anti-dilutive instruments are excluded. |

| Main use | Shows earnings per current common share | Shows earnings per share after considering dilutive potential shares | Comparing both numbers helps separate current per-share profit from possible dilution pressure. |

| Main limitation | Can look stronger when potential dilution is meaningful | Can still exclude instruments that are anti-dilutive in the current period | Neither number proves business quality without checking cash flow, share count, and earnings durability. |

| What it can hide | Future dilution from securities not included in the basic share count | Potential dilution that is currently anti-dilutive or not included under the calculation | An identical basic and diluted EPS figure does not always mean there are no potential shares. |

Basic EPS and Diluted EPS Formula Compared

Basic EPS: Basic EPS = (net income – preferred dividends) / weighted-average common shares.

Diluted EPS: Diluted EPS = adjusted earnings available to common shareholders / weighted-average common shares plus dilutive potential common shares.

The formula contrast mainly comes from the denominator. Basic EPS uses the current weighted-average common-share base. Diluted EPS expands that base when securities such as options, warrants, convertible debt, convertible preferred shares, RSUs or other equity compensation are included when they are dilutive under the applicable EPS calculation.

Accounting note: Some instruments are excluded from diluted EPS when including them would increase EPS instead of reducing it. That anti-dilutive treatment is why diluted EPS is normally lower than or equal to basic EPS, not always lower.

The broader earnings per share concept is still the starting point. The basic-versus-diluted comparison narrows the question to which share count is being used.

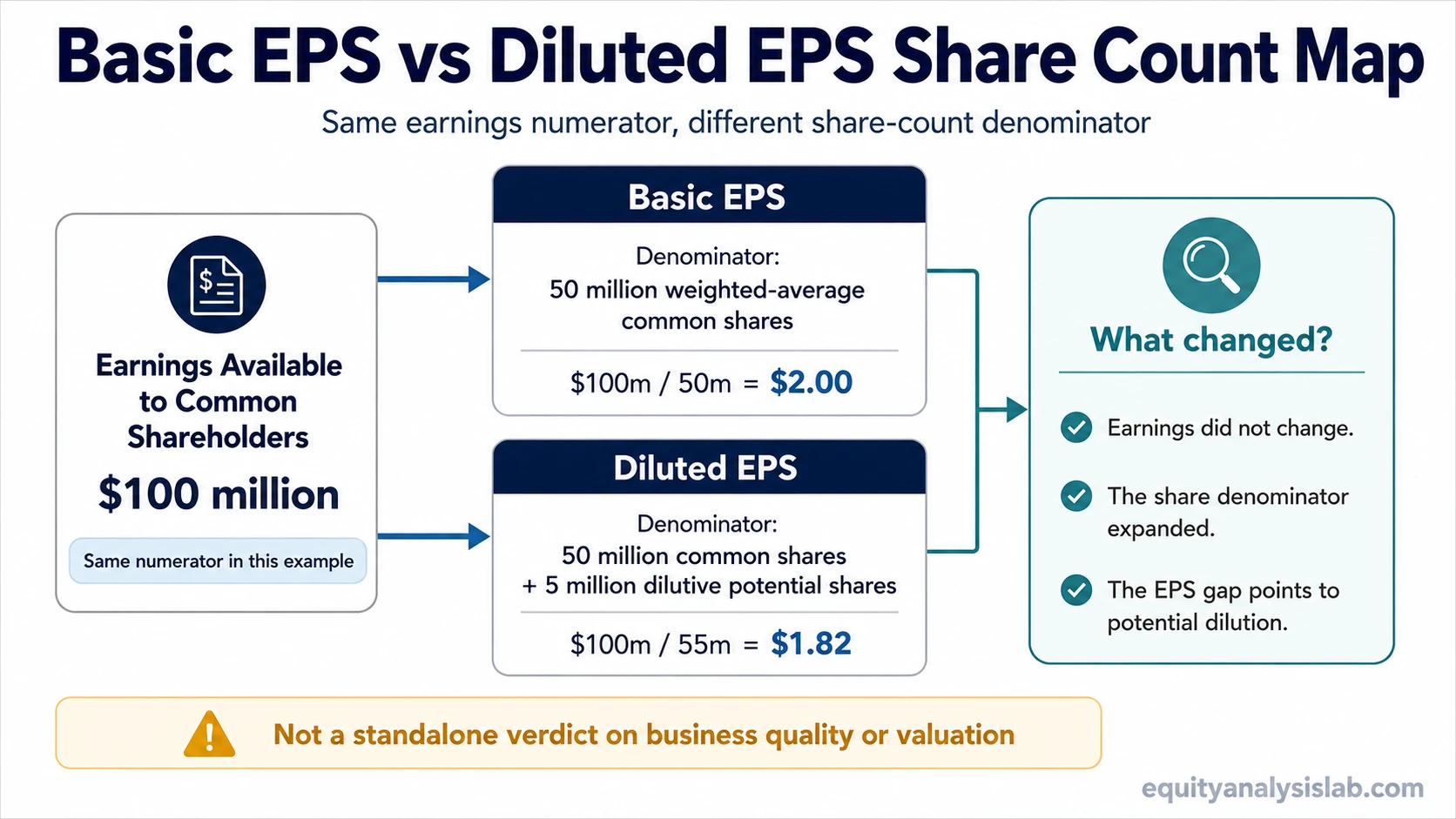

Basic EPS vs Diluted EPS Example

Consider a hypothetical company with $100 million of earnings available to common shareholders after preferred dividends. It has 50 million weighted-average basic shares and 5 million potential dilutive shares.

| Input or result | Basic EPS | Diluted EPS |

|---|---|---|

| Earnings available to common shareholders | $100 million | $100 million |

| Share denominator | 50 million shares | 55 million shares |

| EPS calculation | $100 million / 50 million | $100 million / 55 million |

| Reported EPS result | $2.00 | $1.82 |

Interpretation: The company did not earn less money in the diluted calculation. The per-share figure changed because diluted EPS used a larger denominator. The EPS gap points to potential dilution from the share structure, not automatically to weaker operations.

Why Diluted EPS Can Be Lower Than Basic EPS

Diluted EPS can be lower because the same earnings are divided by a larger possible share count. That larger share base can come from instruments that may become common shares or settle in shares under relevant conditions.

Common sources of dilution include:

- employee stock options;

- warrants;

- convertible debt;

- convertible preferred shares;

- RSUs and other equity compensation where relevant.

A lower diluted EPS figure is not automatically negative. It may reflect compensation design, acquisition financing, convertible capital, or growth-stage funding choices. A company with lower diluted EPS can still have durable per-share economics if dilution is controlled and cash generation supports the share base.

Common Mistakes When Comparing Basic EPS and Diluted EPS

Mistake 1: Treating diluted EPS as always lower. Diluted EPS is normally lower than or equal to basic EPS, but anti-dilutive instruments are excluded from the diluted calculation.

Mistake 2: Treating higher basic EPS as proof of quality. Basic EPS can look stronger simply because it ignores potential common shares. Earnings quality still depends on cash conversion, recurring earnings power, and accounting reliability.

Mistake 3: Ignoring the share-count trend. A small EPS gap in one year can become more important if stock compensation, convertibles, or buybacks change the share base over time.

Mistake 4: Reading the EPS gap as a valuation conclusion. The gap is a diagnostic clue, not a standalone signal that a stock is cheap, expensive, high quality, or low quality.

How Investors Should Use Basic EPS and Diluted EPS

Basic EPS is useful for understanding earnings per current common share. Diluted EPS is useful for testing how much the per-share figure changes after considering dilutive potential shares.

The comparison becomes more useful when it is checked against the company’s share-count history, stock-based compensation, convertible securities, buybacks, and free cash flow. A stable or shrinking share count can support per-share earnings. A rising diluted share count can offset earnings growth if the business does not generate enough cash to absorb dilution.

Neither EPS number should be used alone. The EPS gap should be read alongside dilution trend, capital allocation, cash generation, valuation context, and quality of earnings.

What to Check in a Filing

When comparing basic EPS and diluted EPS in a company filing, look for the figures and notes that explain the denominator rather than only the final EPS line.

- basic EPS;

- diluted EPS;

- weighted-average basic shares;

- weighted-average diluted shares;

- stock-based compensation notes;

- convertibles, warrants, or options;

- share-count trend over multiple reporting periods.

Limitation: A lower diluted EPS does not automatically mean the business is weak. A higher basic EPS does not automatically mean earnings quality is strong. The gap is a diagnostic clue that should be checked against dilution trend, cash flow, earnings quality, and valuation context.

Basic EPS vs Diluted EPS FAQ

Is diluted EPS always lower than basic EPS?

No. Diluted EPS is normally lower than or equal to basic EPS because anti-dilutive instruments are excluded from diluted EPS.

Which EPS number should investors use?

Investors usually compare both. Basic EPS shows the current common-share base, while diluted EPS shows the effect of dilutive potential shares.

Why are basic EPS and diluted EPS sometimes the same?

They can be the same when a company has no dilutive potential shares, or when potential shares are anti-dilutive and excluded from diluted EPS.

Does lower diluted EPS mean a company is worse?

No. Lower diluted EPS can reflect potential dilution, but business quality still depends on cash flow, earnings durability, capital allocation, and valuation context.