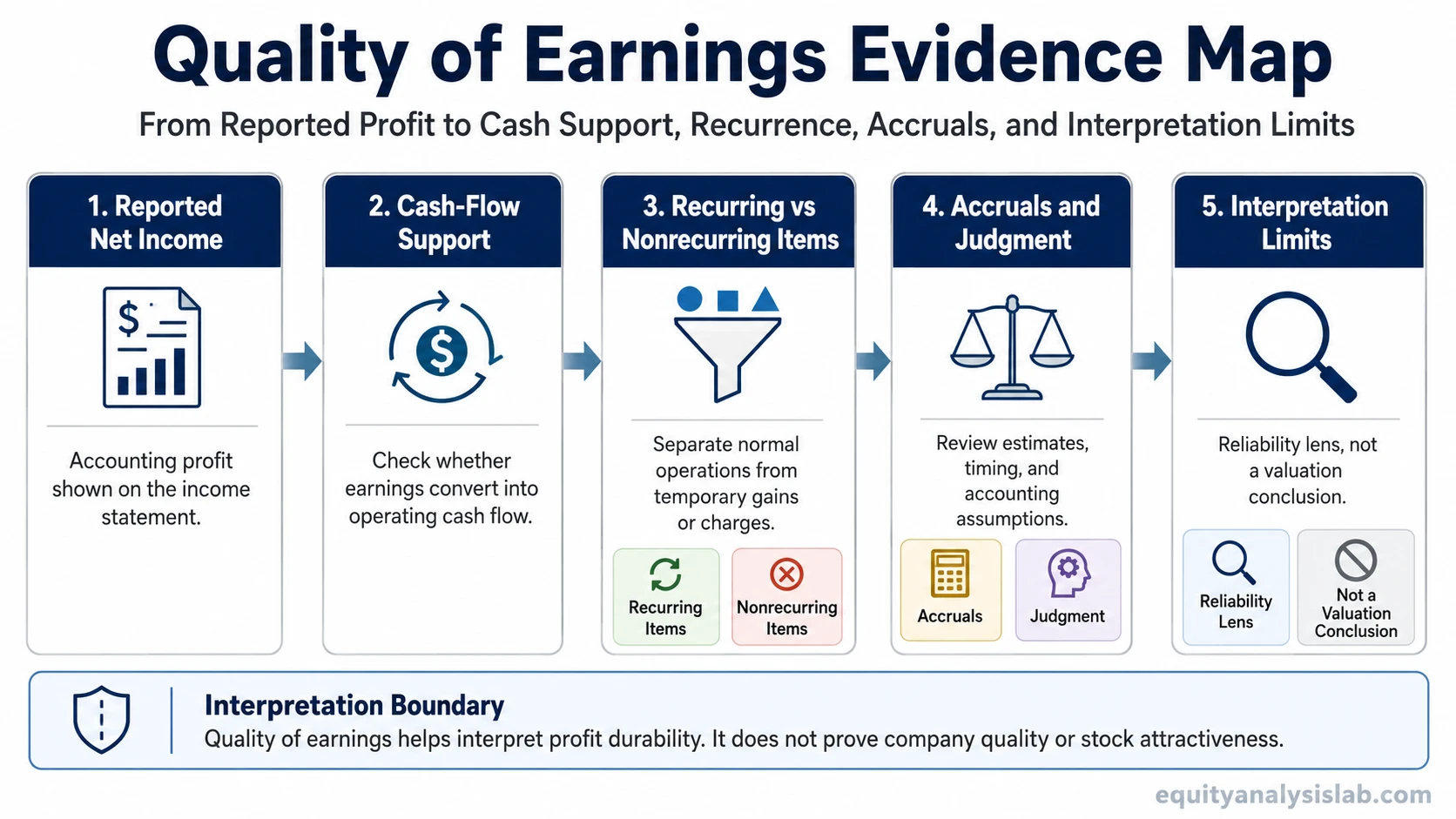

Quality of earnings evaluates how reliable and sustainable reported profit is after checking cash support, recurring and nonrecurring items, accruals, and accounting judgment. It is not the same as high EPS, a strong valuation, business quality, or a stock recommendation.

Quality of earnings is a financial-statement interpretation concept that asks whether reported earnings are supported by repeatable operations, cash generation, and accounting assumptions that appear reasonable for the business.

A company can report positive net income while the quality of that income is weaker than the headline number suggests. The difference can come from one-time gains, revenue timing, aggressive estimates, unusual expense classification, working-capital strain, or earnings that do not convert into operating cash flow.

What Quality of Earnings Means

Quality of earnings focuses on the reliability of profit, not only the size of profit. Stronger earnings quality usually means that reported earnings are tied to normal operations, supported by cash collection, and less dependent on unusual or temporary items.

| What it is | What it is not |

|---|---|

| A check on whether reported profit is repeatable, cash-supported, and less dependent on accounting noise. | A claim that the company is automatically attractive, undervalued, or financially superior. |

| A way to compare accounting profit with operating cash flow, recurring activity, and judgment-heavy estimates. | A replacement for valuation, business model analysis, balance-sheet review, or portfolio risk assessment. |

| A lens used by investors, analysts, and due-diligence teams to interpret the durability of earnings. | A guarantee that future earnings, cash flow, or stock returns will improve. |

Quality of Earnings vs Reported Net Income

Reported net income is the accounting profit shown on the income statement. Quality of earnings asks whether that profit reflects durable economic performance or whether the number depends heavily on temporary, non-cash, or judgment-sensitive items.

Net income can be useful and still need quality checks. A profitable company may show weak earnings quality if cash collection lags, receivables rise faster than revenue, one-time gains lift profit, or expense timing makes one period look stronger than the underlying business trend.

The distinction matters because accounting profit and cash generation do not always move together. The income statement shows recognized revenue and expense, while the cash-flow statement helps test whether those earnings are turning into operating cash flow.

What Strong and Weak Quality of Earnings Can Reveal

A quality-of-earnings review usually compares the reported number with the source and durability of that number. The goal is not to accuse a company of weak reporting, but to separate recurring earnings power from items that may not repeat.

| Reported item | Quality check | What it can reveal | What it cannot prove |

|---|---|---|---|

| Net income | Compare profit with normal operations and period-to-period consistency. | Whether headline profit appears tied to the core business. | It cannot prove the company is a good investment. |

| Operating cash flow | Compare earnings with cash generated by operations. | Whether profit is supported by cash conversion. | It cannot prove future cash flow will remain strong. |

| Revenue recognition | Check whether recognized revenue appears consistent with collection and delivery economics. | Whether revenue timing may be inflating current-period profit. | It cannot prove improper recognition without deeper evidence. |

| One-time gains or expenses | Separate recurring operating profit from unusual gains, charges, or temporary effects. | Whether earnings are repeatable or unusually boosted. | It cannot prove that adjusted earnings are the correct valuation base. |

| Accruals and estimates | Review judgment-heavy items such as allowances, reserves, capitalization, and depreciation assumptions. | Whether accounting judgment has a large effect on profit. | It cannot prove aggressive accounting by itself. |

| Share-count or EPS presentation | Separate earnings reliability from per-share calculation mechanics. | Whether EPS movement may reflect share count as well as profit. | It cannot prove the underlying earnings are high quality. |

Cash Flow, Accruals, and Nonrecurring Items

Cash-flow support is one of the clearest quality checks because it compares recognized profit with actual operating cash generation. Earnings supported by recurring customer collections usually carry a different interpretation from earnings that depend heavily on non-cash accruals, delayed collections, or temporary working-capital effects.

Accrual accounting is not automatically a weakness. Many normal businesses recognize revenue and expenses before cash changes hands. The quality question is whether those accruals remain proportionate, consistent, and supported by later cash conversion.

Nonrecurring items can also change the reading. An asset sale, legal settlement, restructuring charge, inventory write-down, tax benefit, or unusual classification shift may affect one period without representing the company’s normal earnings base. Strong quality-of-earnings analysis separates those temporary effects from recurring operating performance.

Audit boundary: A clean audit opinion and high earnings quality are related but not identical. Financial statements can follow accounting rules and still require interpretation around sustainability, cash conversion, nonrecurring items, and judgment-heavy estimates.

Simple Quality of Earnings Example

Hypothetical example: Company A reports $100 million of net income. Operating cash flow is only $35 million. A large portion of the profit comes from a one-time asset sale, and receivables rise faster than revenue.

That pattern does not prove the company is poor, fraudulent, or unattractive. It shows why the reported profit needs quality checks. The analyst would separate recurring operating income from the asset sale, compare revenue growth with cash collection, and ask whether working-capital changes are temporary or structural.

A different company could report lower net income but stronger earnings quality if profit comes mainly from recurring operations, operating cash flow tracks earnings closely, and unusual adjustments are small. The quality reading depends on the relationship between profit, cash, recurrence, and accounting judgment.

Quality of Earnings Is Not the Same as EPS

EPS measures profit on a per-share basis. Quality of earnings asks whether the underlying profit deserves confidence before the per-share number is interpreted. A company can show rising per-share earnings while earnings quality weakens if the increase depends on nonrecurring gains, lower share count, or accounting estimates rather than stronger recurring operations.

Basic EPS uses the profit available to common shareholders and the weighted average common shares outstanding. That calculation can be accurate while still leaving a separate question: whether the earnings numerator is durable, cash-supported, and recurring.

A diluted EPS calculation adds another boundary by considering potential share dilution. Dilution analysis can change the per-share reading, but it still does not answer whether the reported earnings themselves are high quality.

Quality of Earnings Reports and Investor Use

A quality of earnings report is a formal due-diligence document commonly used in transaction settings. It applies the same core idea in more detail by testing whether reported earnings are recurring, cash-supported, and affected by unusual or non-operating items. The formal report is one application of the concept, not the whole concept.

For investors reading public filings, the same logic can be applied more simply: compare income statement profit with operating cash flow, identify unusual items, review accrual-heavy areas, and avoid treating the headline earnings number as complete evidence by itself.

What Quality of Earnings Cannot Prove

Quality of earnings is a diagnostic lens, not a conclusion. Stronger earnings quality can support confidence in reported profit, but it does not prove that a stock is undervalued, that a company has a durable moat, or that future returns will be attractive.

Weak earnings quality also does not automatically mean fraud or permanent business decline. It may reflect seasonality, investment cycles, temporary working-capital movements, acquisition effects, accounting timing, or a legitimate one-time event.

The most useful interpretation combines earnings quality with business model analysis, balance-sheet risk, capital allocation, valuation, and the company’s industry context. Quality checks improve the reliability of the earnings base, but they do not replace the rest of the investment process.

FAQ

What is quality of earnings?

Quality of earnings is the reliability and sustainability of reported profit after checking cash support, recurring items, accruals, and accounting judgment. It asks whether earnings reflect durable business performance or temporary accounting and nonrecurring effects.

Is quality of earnings the same as net income?

No. Net income is the reported accounting profit. Quality of earnings evaluates how much confidence that profit deserves by comparing it with cash flow, recurrence, accounting estimates, and unusual items.

What is a quality of earnings report?

A quality of earnings report is a formal due-diligence analysis that examines whether reported earnings are recurring, cash-supported, and adjusted for unusual or non-operating items. It is common in transaction settings, but the concept also helps investors interpret public financial statements.