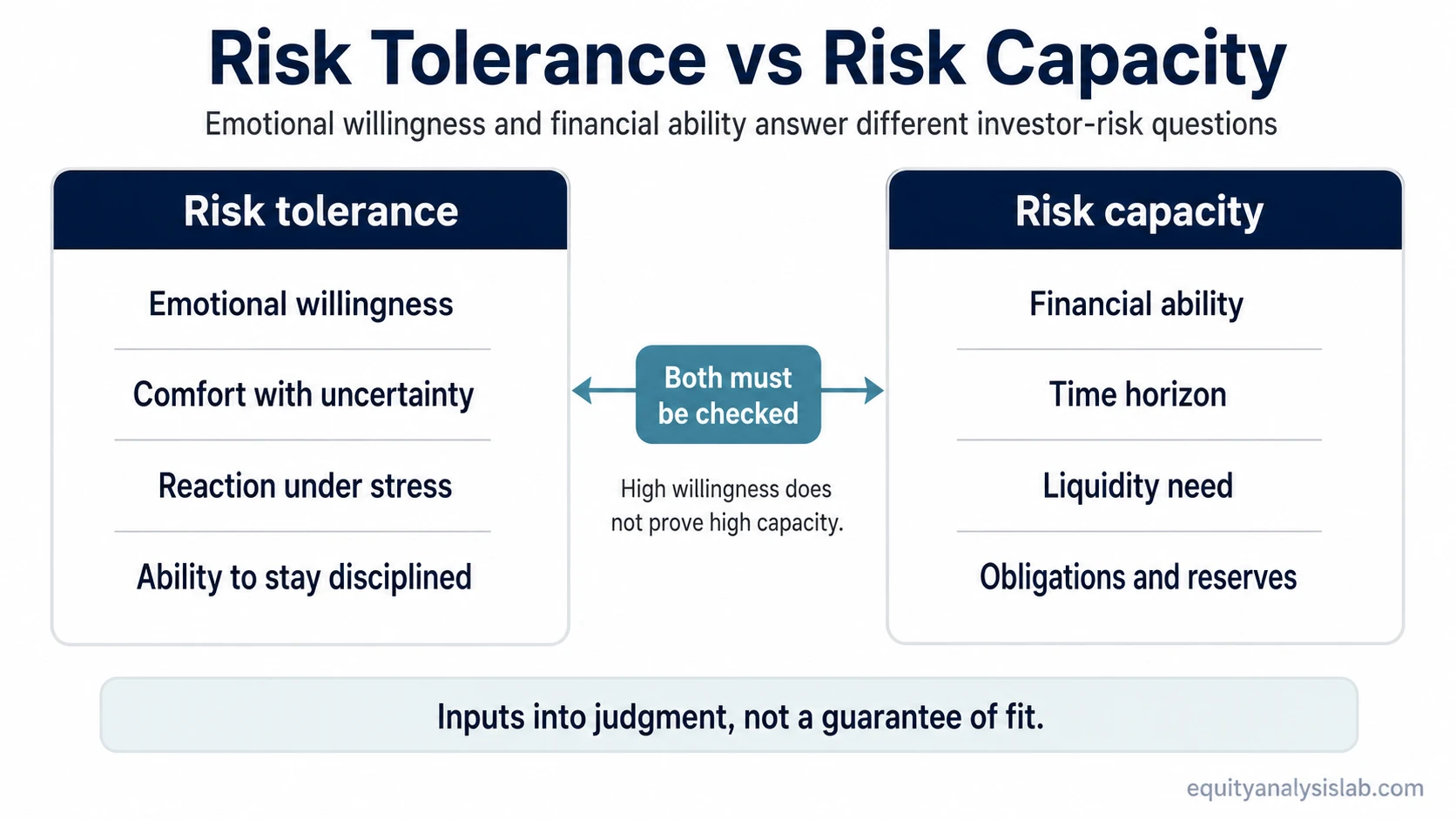

Risk tolerance and risk capacity are not the same part of an investor’s risk profile. Risk tolerance is the willingness to live with uncertainty. Risk capacity is the financial ability to absorb adverse outcomes without damaging the purpose of the capital.

Core distinction: tolerance asks, “Can I emotionally stay with this uncertainty?” Capacity asks, “Can my financial situation absorb this uncertainty if the outcome is unfavorable?”

The confusion matters because the two can point in different directions. An investor may feel comfortable with large price swings but still have limited capacity because the money is needed soon. Another investor may have strong finances but still be unable to stay calm when uncertainty rises.

Risk tolerance vs risk capacity: the core difference

Risk tolerance describes the emotional side of uncertainty. It reflects how much fluctuation, ambiguity, or temporary loss an investor believes they can accept without abandoning the plan.

Risk capacity describes the financial side of uncertainty. It depends on whether the investor’s resources, time horizon, liquidity needs, obligations, and capital purpose can withstand an adverse outcome.

| Comparison point | Risk tolerance | Risk capacity |

|---|---|---|

| Question answered | How much uncertainty can the investor emotionally accept? | How much uncertainty can the investor financially absorb? |

| Main evidence source | Behavior, preferences, past reactions, and comfort with drawdowns. | Income stability, liquidity need, obligations, time horizon, and capital purpose. |

| Main constraint | Emotional ability to remain disciplined when outcomes feel uncomfortable. | Financial ability to avoid forced selling or damage to the capital’s intended use. |

| What can change it | Experience, market stress, personal confidence, family situation, or a painful prior loss. | Job security, debt, cash reserves, time horizon, near-term spending needs, or purpose of the funds. |

| Misuse risk | Assuming comfort with risk means the investor can afford the downside. | Assuming financial strength means the investor will emotionally tolerate uncertainty. |

How risk tolerance and risk capacity are measured

Risk tolerance is usually interpreted through willingness. Useful evidence includes how the investor reacts to uncertainty, whether temporary losses lead to panic, and whether the investor can follow a plan when the outcome is unclear.

Risk capacity is interpreted through observable constraints. Useful evidence includes income stability, emergency reserves, debt obligations, liquidity needs, time horizon, and whether the capital has a specific purpose that cannot be delayed.

| Input | What it tells you | Mostly tolerance or capacity? |

|---|---|---|

| Emotional response to drawdown | Whether uncertainty may cause the investor to abandon the plan. | Risk tolerance |

| Time horizon | How much time the capital may have before it is needed. | Risk capacity |

| Liquidity need | Whether the investor may need to access the capital under unfavorable conditions. | Risk capacity |

| Income stability | Whether outside cash flow can support the investor through uncertainty. | Risk capacity |

| Prior reaction to market stress | Whether stated comfort matches real behavior under pressure. | Risk tolerance |

Neither side should be reduced to a single score. A questionnaire may help organize preferences, but it cannot remove the need to compare stated comfort with real financial constraints.

Why the two can conflict

Risk tolerance and risk capacity can conflict because they answer different questions. Tolerance can be high when an investor feels confident, experienced, or comfortable with volatility. Capacity can still be low if the same investor has a short time horizon, unstable income, or a near-term liquidity need.

The reverse can also happen. An investor may have strong savings, stable income, and no immediate need for the capital, but still have low tolerance if uncertainty causes stress or impulsive decisions.

Investor-use boundary: risk tolerance and risk capacity can organize the decision process, but they do not determine a suitable allocation, product, or expected return by themselves. They are inputs into judgment, not a guarantee of fit.

Same investor, different reading

Illustrative scenario: An investor says they are comfortable with large portfolio swings because they understand that markets can be uneven. On the tolerance side, that may suggest a willingness to accept uncertainty.

The same investor also expects to use part of the capital for a major expense within the next year. On the capacity side, that near-term need may reduce the room to absorb an adverse outcome, even if the investor feels emotionally comfortable with volatility.

The distinction is not that one side is “right” and the other is “wrong.” The useful reading is that emotional willingness and financial ability are separate constraints. A stronger decision process checks both before treating risk exposure as sustainable.

Common mistake: treating willingness as capacity

Common mistake: treating high risk tolerance as proof of high risk capacity.

An investor may be willing to tolerate uncertainty but still lack the financial room to absorb it. Confidence does not create liquidity, extend a short time horizon, remove debt obligations, or change the purpose of the capital.

The opposite mistake is assuming that high risk capacity guarantees emotional discipline. Financial strength can create room to absorb uncertainty, but it does not guarantee that the investor will stay calm, avoid impulsive changes, or remain aligned with the plan under stress.

Risk tolerance and risk capacity in investor decisions

Risk tolerance and risk capacity work best as separate checks inside a broader investor decision process. The investor first clarifies the purpose of the capital, then checks whether the emotional and financial constraints support the same level of uncertainty.

That broader purpose belongs with investment objectives. An objective helps define what the capital is supposed to do, while tolerance and capacity help test whether the uncertainty attached to the approach is realistic for the investor.

A separate evidence boundary can also affect the decision. An investor may be willing and financially able to accept uncertainty, but still need to ask whether the investment is understandable enough to evaluate. That boundary is closer to the circle of competence than to a simple risk-score label.

Practical interpretation: when tolerance and capacity point in different directions, the conflict is the review point. It means the investor has not found a clean match between emotional willingness, financial constraints, and capital purpose.

FAQ

Is risk capacity the same as risk tolerance?

No. Risk tolerance is emotional willingness to accept uncertainty. Risk capacity is the financial ability to absorb adverse outcomes without damaging the purpose of the capital.

Which matters more, risk tolerance or risk capacity?

Neither is universally more important. They answer different questions, and a sound interpretation separates both instead of replacing one with the other.

Can an investor have high risk tolerance but low risk capacity?

Yes. An investor may feel comfortable with volatility but still have low capacity because of a short time horizon, liquidity need, debt obligation, or unstable income.