A poor man’s covered call is an options structure that combines a longer-dated in-the-money call with a shorter-dated out-of-the-money short call, creating covered-call-like exposure without buying the underlying shares.

The long call can substitute for part of the stock exposure, while the short call brings in premium, caps upside above the short-call strike, and creates assignment or exercise review. The structure is not the same as owning stock because the long call has an expiration date, time value, implied-volatility exposure, and option-liquidity risk.

What a poor man’s covered call means

A poor man’s covered call is commonly described as a long-call diagonal spread. It uses one longer-dated call option, usually with a lower strike, and one shorter-dated short call option, usually with a higher strike. The position begins with a net debit because the long call normally costs more than the premium received from the short call.

The name comes from the comparison with a covered call, but the economic structure is different. A covered call owns shares and sells a call against those shares. A poor man’s covered call owns a call option instead of the stock, so the position depends on option pricing as well as the underlying price.

Key points

- A poor man’s covered call combines a longer-dated call with a shorter-dated short call.

- It can resemble a covered call, but it does not create stock ownership.

- The short call premium comes with an upside cap and assignment or exercise review.

- The simplified payoff chart does not capture every pre-expiration risk.

- Time value, implied volatility, liquidity, dividends, and broker treatment can change the real economics.

PMCC leg structure

The structure has two separate jobs. The longer-dated call provides directional exposure, while the shorter-dated short call receives premium and creates the covered-call-like cap. Because the two legs usually have different expirations, the position must be read as more than a simple one-date payoff diagram.

| Leg | Typical role | Main boundary |

|---|---|---|

| Longer-dated lower-strike call | Provides call exposure to the underlying without buying shares. | Can lose value if the underlying falls, time passes, implied volatility changes, or liquidity worsens. |

| Shorter-dated higher-strike short call | Receives premium and creates the covered-call-like cap. | Can limit upside and may require assignment, exercise, or closeout review. |

| Net debit | Represents the amount paid after subtracting short-call premium from long-call cost. | Defines the simplified capital outlay, but not every practical risk before expiration. |

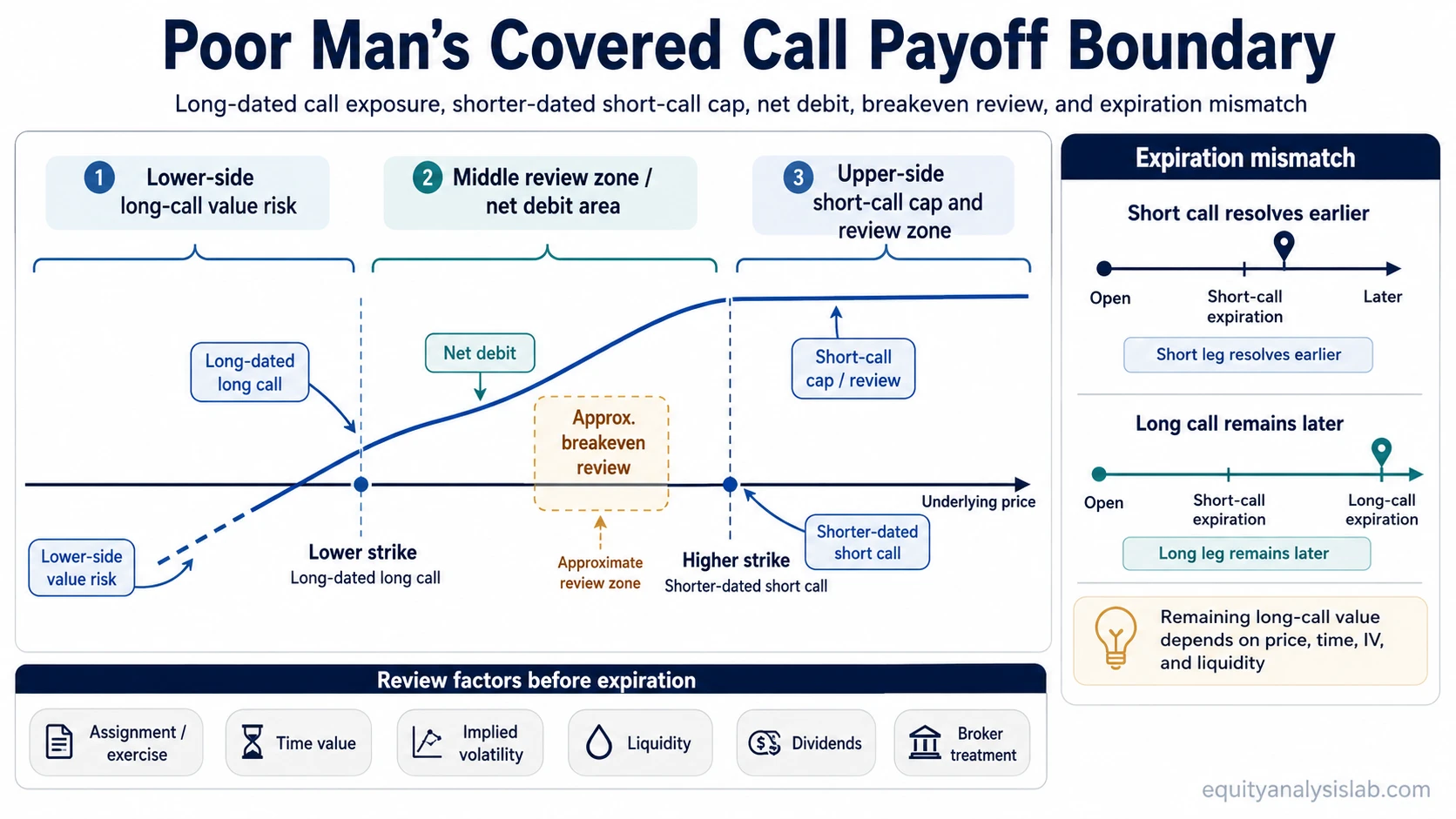

How the payoff boundary works

In a simplified expiration view, the long call gives the position upside exposure above its strike, while the short call limits part of that upside above the short-call strike. The position is usually opened for a net debit, so the long-call cost is only partly offset by the premium received from the short call.

In a simplified expiration view, the breakeven depends on the net debit paid and the value retained by the longer-dated call after the shorter-dated call resolves. Because the two options usually expire on different dates, a PMCC breakeven should be treated as an approximation rather than a fixed stock-style breakeven.

The upper boundary comes from the short call. If the underlying rises above the short-call strike, the short call can gain intrinsic value against the position and may need to be closed, assigned, or otherwise reviewed depending on the account and broker treatment.

The lower boundary is not identical to a stock covered call. If the underlying falls, the long call can lose intrinsic value, extrinsic value, or both. Because the long call expires, the structure has a time limit that common stock does not have.

Poor man’s covered call vs traditional covered call

The core difference is the asset used as the long side of the structure. A traditional covered call owns the underlying shares. A poor man’s covered call uses a long call option as the exposure leg.

| Feature | Traditional covered call | Poor man’s covered call |

|---|---|---|

| Long exposure | Shares of the underlying stock. | A longer-dated call option. |

| Expiration on long side | No option expiration on the shares. | The long call has an expiration date. |

| Capital required | Usually higher because shares are purchased. | Often lower because the long call substitutes for stock exposure. |

| Main added complexity | Stock ownership plus short-call obligation. | Short-call obligation plus time value, implied volatility, and long-call expiration risk. |

Lower initial capital does not automatically mean lower risk. The PMCC changes the risk mix by replacing stock ownership with an option whose value depends on price, time, implied volatility, moneyness, and liquidity.

What changes the interpretation before expiration

A payoff diagram can be useful, but it is usually too clean for real-time interpretation. Before expiration, both legs can change value for reasons that are not visible in a simple final-payoff line.

| Variable | Why it matters | Interpretation limit |

|---|---|---|

| Expiration mismatch | The short call can expire or be assigned before the long call expires. | The position may need review before the long call reaches its own expiration. |

| Time decay | The short call and long call decay on different timelines. | Short-call premium is not free compensation if the long call loses value at the same time. |

| Implied volatility | Changes in volatility can affect the long call and short call differently. | A favorable price move can still produce weaker results if option value changes unfavorably. |

| Dividends | Dividend timing can influence early-exercise risk on some short calls. | Dividend review matters, especially when the short call is near or in the money. |

| Liquidity and spreads | Wide bid-ask spreads can raise entry, exit, and adjustment friction. | Theoretical payoff can differ from executable economics. |

| Assignment and exercise | The short call creates an obligation that can interact with the long call. | Assignment treatment can vary by broker, account permissions, and position handling. |

| Broker treatment | Margin, approval, exercise, and risk systems are not identical across brokers. | The simplified structure does not guarantee identical operational treatment in every account. |

Illustrative PMCC example

Assume an underlying trades at a symbolic price of 100. A longer-dated call with a lower strike is purchased for 25, and a shorter-dated call with a higher strike is sold for 4. The simplified net debit is 21 before commissions, fees, taxes, spread friction, and later changes in option pricing.

If the underlying rises toward or above the short-call strike, the long call may gain value, but the short call can cap part of the upside and may require assignment or closeout review. If the underlying falls, the long call can lose value even if the short call premium partly offsets the initial cost.

This example is only a structural illustration. It does not imply that any strike, expiration, premium, or account treatment should be used in practice.

Common mistakes with poor man’s covered calls

- Treating premium as free compensation: short-call premium is received in exchange for an obligation and an upside cap.

- Treating the long call as identical to stock: the long call has expiration, time value, implied-volatility exposure, and option liquidity risk.

- Ignoring the expiration mismatch: the short call can require review before the long call expires.

- Reading the payoff chart too literally: simplified expiration diagrams do not show all pre-expiration price, volatility, and liquidity changes.

- Assuming assignment risk disappears: the short call can still create assignment or exercise questions depending on moneyness, timing, dividends, and broker handling.

Risk and limitation boundary

A poor man’s covered call can reduce the capital needed to create covered-call-like exposure, but it does not remove downside risk, short-call obligation, or operational complexity. The position can be sensitive to the underlying price, the remaining life of both options, implied volatility, bid-ask spreads, dividend timing, and broker-specific exercise or assignment rules.

The cleanest way to read the structure is as a capped long-call diagonal spread, not as a cheaper version of stock ownership. That distinction keeps the analysis focused on contract mechanics instead of premium claims or strategy promotion.

Related spread structures

A PMCC is not a vertical spread, but comparing it with nearby structures can clarify the boundary. A bull call spread uses two calls with the same expiration to define a capped bullish debit spread. A bull put spread uses put options and typically starts with a net credit. A bear put spread uses puts to create a bearish debit spread with defined expiration boundaries.

FAQ

Is a poor man’s covered call the same as a covered call?

No. A covered call owns shares and sells a call against them. A poor man’s covered call uses a longer-dated call option instead of the shares, so it adds expiration, time value, implied-volatility, and option-liquidity considerations.

Why is it called a poor man’s covered call?

The name refers to the lower initial capital outlay compared with buying shares for a traditional covered call. The name should not be read as a risk label because the option version has its own contract-specific risks.

Can the short call be assigned in a PMCC?

Yes, assignment can be a review factor when a short call is in or near the money, especially around dividend timing or expiration. Broker and account treatment can vary, so the simplified payoff diagram should not be treated as the full operational picture.