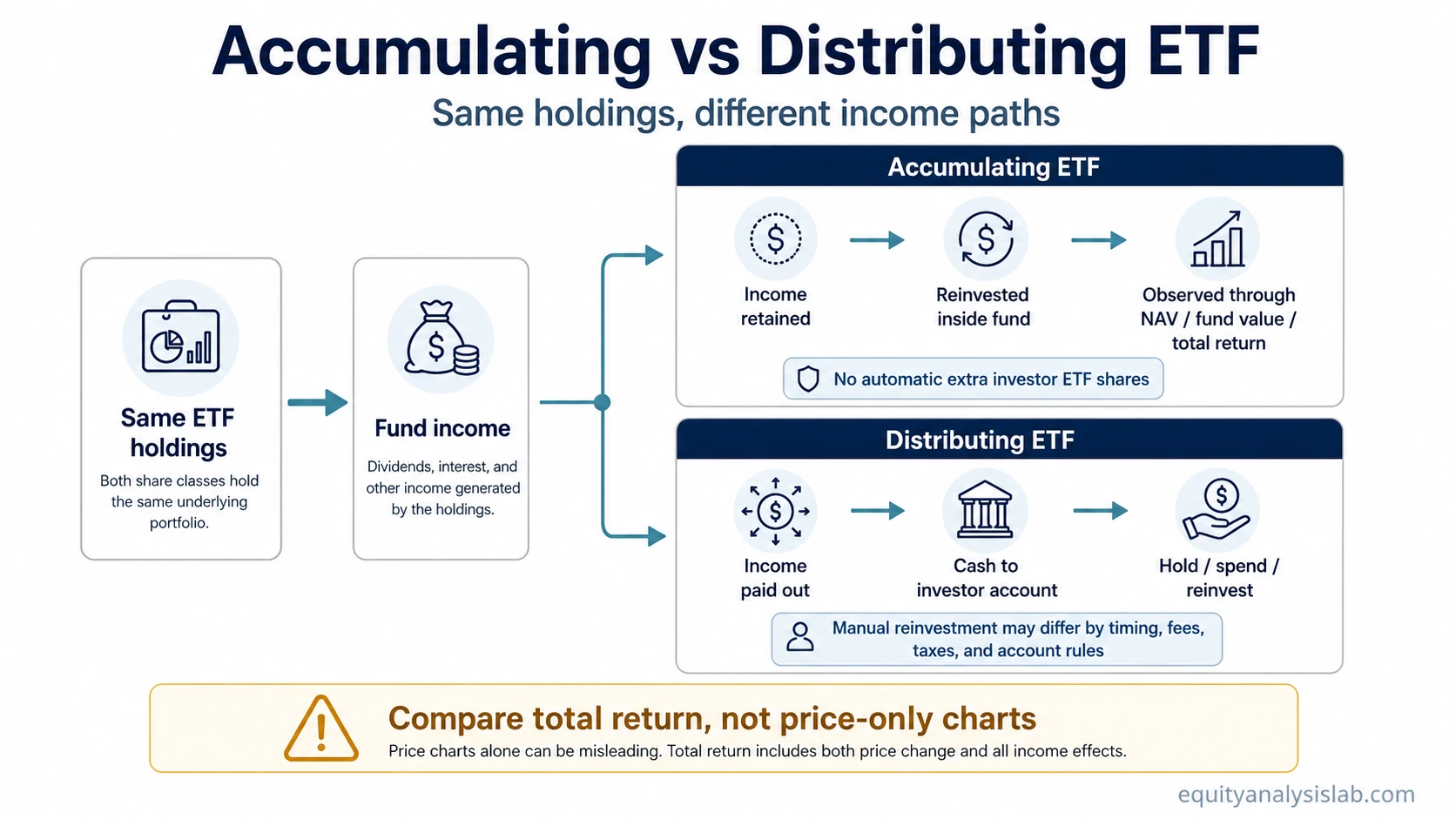

An accumulating ETF reinvests fund income inside the portfolio, while a distributing ETF pays fund income out to investors as cash. The choice changes how income appears in the investor account, how the fund value is observed, and how returns should be compared, but it does not by itself make one ETF better than the other.

Both structures can give exposure to the same market, index, or strategy. The difference is the income path: accumulation keeps income inside the fund, while distribution moves income out of the fund and into the investor’s cash balance. That distinction matters when comparing ETF share classes, reinvestment assumptions, taxes, and total return.

Key points

- The main distinction is the income path: retained inside the ETF versus paid out to the investor’s cash balance.

- An accumulating ETF does not automatically give the investor extra ETF shares purely because income was reinvested inside the fund.

- A distributing ETF can be manually reinvested, but timing, fees, taxes, and account rules can change the realized result.

- Price-only charts can mislead because distributions may not appear in the ETF price after cash is paid out.

- Tax treatment depends on jurisdiction and account type, so the label alone is not enough to choose between share classes.

Accumulating vs distributing ETF: quick comparison

| Comparison point | Accumulating ETF | Distributing ETF |

|---|---|---|

| Income handling | Fund income is retained and reinvested inside the portfolio. | Fund income is paid out to investors as cash distributions. |

| Investor cash flow | The investor usually does not receive cash from the income event. | The investor receives cash into the brokerage or account cash balance. |

| Fund value effect | Reinvested income is reflected inside the fund’s value over time. | Paid-out income leaves the fund, so price-only comparison can understate total return. |

| Investor share count | The investor does not automatically receive more ETF shares just because the fund accumulated income. | The investor’s ETF share count also stays the same unless cash is manually reinvested into more shares. |

| Manual reinvestment | Reinvestment is handled inside the fund. | The investor may spend, hold, or reinvest the cash, subject to account rules, timing, fees, and taxes. |

| Tax/account caveat | Treatment depends on the investor’s jurisdiction and account type. | Treatment also depends on the investor’s jurisdiction and account type. |

| Possible investor fit | May fit investors who want income retained inside the investment structure. | May fit investors who want visible cash income or direct control over reinvestment. |

How accumulation affects fund value and share count

An accumulating ETF keeps fund income inside the portfolio instead of paying it directly to the investor. That income may come from dividends, interest, or other portfolio income depending on what the fund holds. For equity ETFs, the income is commonly linked to ETF dividends, but the broader distinction is about fund income, not only company dividends.

The reinvested income is reflected through the fund’s value rather than through a separate cash payment. If the ETF’s underlying holdings generate income and the fund retains it, the value stays inside the fund structure. The investor does not automatically see new ETF units appear in the account purely because the ETF is accumulating.

In fund reporting, that retained income is usually observed through the ETF’s fund value, NAV, and total-return data rather than through a separate cash distribution paid to the investor.

Share-count clarification: Accumulation happens inside the ETF. It is not the same as a broker automatically buying additional ETF shares for the investor. The investor’s number of ETF shares changes only if additional shares are bought, sold, or otherwise credited under a separate account or broker process.

How distributing ETFs handle income

A distributing ETF pays fund income out to investors as cash. The investor then decides whether to hold the cash, spend it, or reinvest it. Distribution frequency can vary by fund, share class, provider, market, and policy, so the label alone does not tell the full timing pattern.

When income is paid out, the cash leaves the fund and appears outside the ETF position. That does not automatically make the ETF worse. It means the return is split between the ETF price movement and the cash distributions received. For that reason, a distributing ETF can look weaker on a price-only chart even when the investor received cash along the way.

Same holdings, different income path

Consider two ETF share classes that track the same index and hold the same securities. If the underlying companies pay income into the fund, the accumulating class reinvests that income inside the ETF, while the distributing class pays the income out to the investor as cash.

The economic comparison becomes closer if the distributing investor manually reinvests every cash distribution into the same ETF. Even then, the realized result may differ because of tax treatment, cash drag, trade timing, bid-ask spread, transaction costs, fractional-share availability, and account rules. The point is not that one label is automatically superior; the point is that the income path changes how the investor experiences the same underlying exposure.

Compare total return, not only price

A price-only chart can be misleading when comparing accumulating and distributing ETFs. An accumulating ETF keeps income inside the fund, so the effect is more likely to be reflected in the fund value. A distributing ETF pays income out, so part of the investor’s return may sit outside the ETF price as cash received.

A better comparison looks at total return, including distributions and any reinvestment assumptions. If one share class assumes automatic reinvestment and another shows only market price, the comparison is not like-for-like. The investor should check whether the performance figure includes distributions, assumes reinvestment, deducts costs, or reflects the actual cash flow received in the account.

Tax and account rules can change the answer

Tax treatment can depend on the investor’s country, account wrapper, fund domicile, distribution policy, and local rules. Some investors may be taxed when income is distributed. Others may face rules that treat accumulated income differently. The correct comparison can change across jurisdictions and account types.

This is why the accumulating-versus-distributing decision should not be reduced to a universal tax rule. The label is only one input. Investors comparing share classes should also review the relevant fund documents, account rules, and the broader ETF tax efficiency considerations that apply to their situation.

How to identify an ETF’s distribution policy

ETF providers often use labels such as Acc, Dist, Dis, C, or D to indicate whether a share class accumulates or distributes income. These labels are not perfectly standardized across every provider and market, so they should be treated as clues rather than final proof.

The more reliable check is the fund’s official factsheet, prospectus, key information document, or provider page. Look for terms such as accumulation, income, distribution, dividend policy, reinvestment policy, distribution frequency, and share class. The share-class label should match the fund documents before it is used in an investment comparison.

Observable checklist before comparing Acc and Dist share classes

Before choosing between an accumulating and distributing version of an ETF, compare the structure rather than only the label.

- Same index or strategy: Confirm that both share classes track the same benchmark or investment approach.

- Same underlying holdings: Check whether the portfolio exposure is actually comparable.

- Same costs: Compare the expense ratio and any other recurring fund-level costs.

- Tracking difference: Review whether one class has behaved differently from the benchmark after costs and fund mechanics.

- Trading conditions: Check spread, market depth, and ETF liquidity, especially if one share class trades less actively.

- Distribution policy: Confirm whether income is accumulated, distributed, or subject to a specific policy.

- Tax and account treatment: Check how the relevant account and jurisdiction treat accumulated income, distributed income, and reinvestment.

Common mistakes when comparing accumulating and distributing ETFs

- Assuming accumulation creates extra shares: Accumulation normally affects the fund value, not the investor’s share count.

- Calling distributing ETFs worse because cash leaves the fund: Cash distributions are part of total return and must be counted.

- Comparing price-only performance: A price chart can miss cash distributions unless total return is included.

- Treating tax rules as universal: Tax outcomes can vary by country, account type, fund domicile, and investor situation.

- Choosing by label alone: Acc or Dist should be checked alongside holdings, costs, liquidity, tracking difference, and fund documents.

- Ignoring reinvestment frictions: Manual reinvestment may involve timing differences, spreads, transaction costs, or fractional-share limits.

When each structure may fit better

An accumulating ETF may fit an investor who wants income retained inside the fund structure and does not need visible cash payments from the ETF. It can make reinvestment simpler because the income path stays inside the fund, although the tax treatment still needs to be checked.

A distributing ETF may fit an investor who wants visible cash income, needs portfolio cash flow, or wants direct control over whether income is spent, held, or reinvested. That control can be useful, but it also creates more decisions and possible reinvestment friction.

The practical decision is not “which ETF type is better?” It is “which income path fits the investor’s cash-flow needs, account rules, tax situation, and comparison method?”

FAQ

Is an accumulating ETF always better than a distributing ETF?

No. An accumulating ETF is not automatically better. It reinvests income inside the fund, while a distributing ETF pays income out as cash. The better fit depends on cash-flow needs, account rules, taxes, reinvestment behavior, costs, and total-return comparison.

Does an accumulating ETF give me more ETF shares?

Not automatically. Accumulation happens inside the fund. The investor’s ETF share count normally changes only if additional shares are bought, sold, or otherwise credited through a separate account or broker process.

Can I make a distributing ETF behave like an accumulating ETF?

You may be able to reinvest cash distributions manually, which can make the comparison closer. The result may still differ because of taxes, timing, bid-ask spreads, transaction costs, fractional-share rules, and account restrictions.

Why can price charts make distributing ETFs look worse?

A distributing ETF pays part of its return out as cash, so a price-only chart may not show the full investor return. Total-return comparison is usually more appropriate because it accounts for distributions and reinvestment assumptions.