A credit spread receives a net premium upfront. A debit spread pays a net premium upfront.

That cash-flow difference changes the breakeven, payoff path, time-decay exposure, volatility sensitivity, and short-leg review. It does not make either spread automatically safer, better, or more appropriate. The structure still depends on strikes, expiration, option style, costs, liquidity, and how the underlying moves.

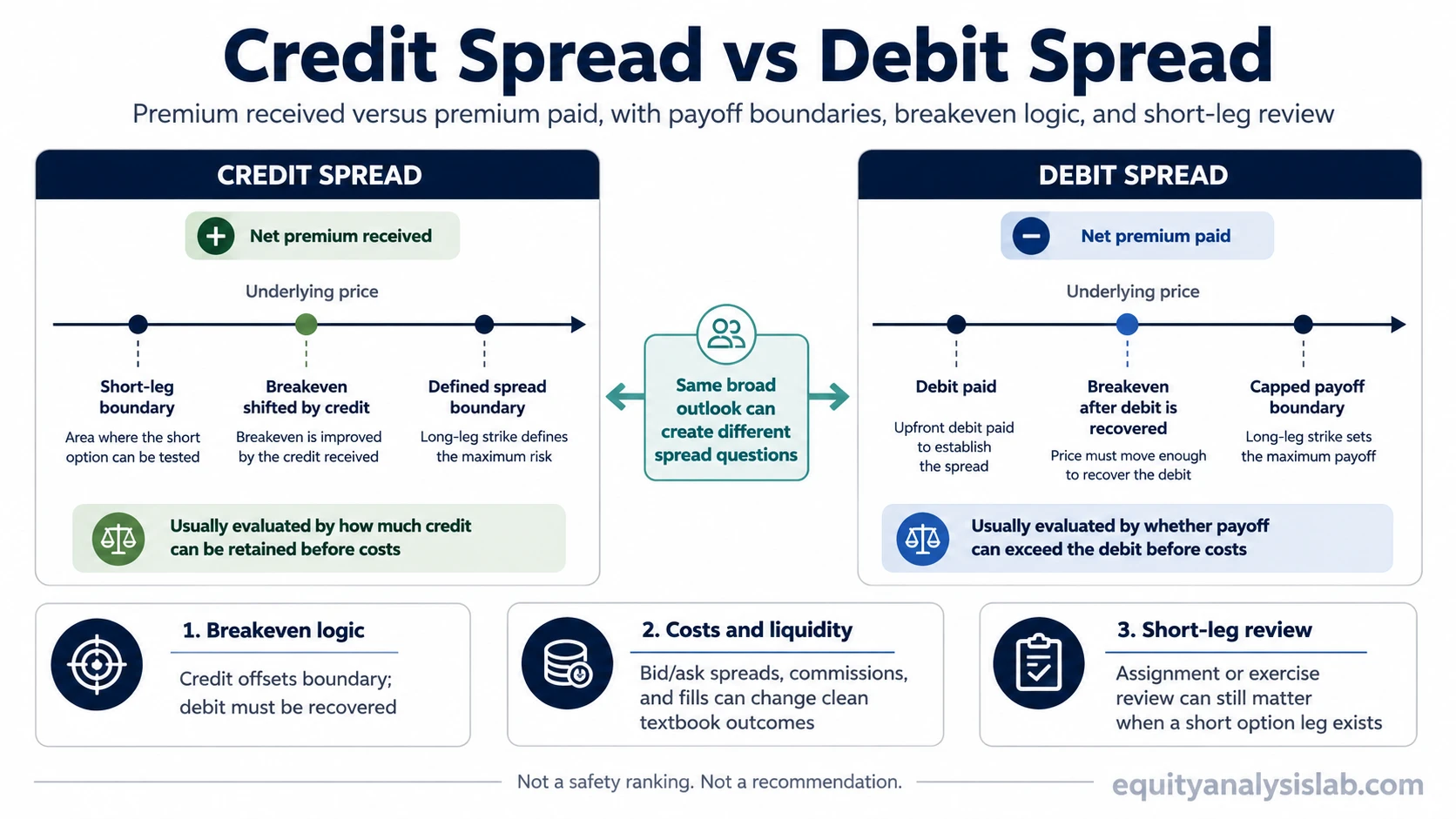

Core distinction: a credit spread starts with premium received; a debit spread starts with premium paid. Both can use options with the same expiration and different strikes, but the initial cash flow changes how the position reaches profit or loss before costs.

- Credit spread: premium is collected at entry, and the spread is usually evaluated by how much of that credit can be retained before costs.

- Debit spread: premium is paid at entry, and the spread is usually evaluated by whether the payoff can exceed the debit before costs.

- Risk review: the short option leg still matters, especially around expiration, moneyness, dividends, interest rates, and contract specifications.

Credit spread vs debit spread at a glance

The cleanest comparison starts with initial cash flow, then moves to payoff boundary, breakeven logic, volatility, time decay, and short-leg exposure.

| Criteria | Credit spread | Debit spread |

|---|---|---|

| Initial cash flow | Receives net premium upfront. | Pays net premium upfront. |

| Typical structure | Sells a higher-premium option and buys a lower-premium option in the same spread structure. | Buys a higher-premium option and sells a lower-premium option in the same spread structure. |

| Maximum profit before costs | Usually limited to the net credit received, before commissions, fees, and execution effects. | Usually limited to the strike width minus the net debit paid, before commissions, fees, and execution effects. |

| Maximum loss before costs | Usually the strike width minus the net credit received, before costs and real-world execution effects. | Usually limited to the net debit paid, before costs and real-world execution effects. |

| Breakeven logic | The received credit shifts the breakeven away from the short strike. | The paid debit must be overcome before the spread can reach profit. |

| Time decay tendency | Often discussed as benefiting from time decay if the underlying stays in a favorable zone, but that is not guaranteed. | Often faces time-decay pressure if favorable movement does not develop quickly enough. |

| Implied volatility tendency | Often discussed as more exposed to volatility contraction or expansion through the short option component. | Often discussed as more sensitive to whether the long option value can expand enough to offset the debit and time decay. |

| Assignment/exercise review | Short option legs can create assignment review, especially with American-style options. | Short option legs can still matter when the debit spread includes a short option. |

| Main confusion | Receiving premium can be mistaken for lower risk. | Paying premium can be mistaken for a worse structure. |

| Next mechanics to review | Review credit-spread mechanics when the key question is premium received and short-leg boundary. | Review debit-spread mechanics when the key question is premium paid and capped payoff potential. |

Capital or margin treatment can differ by broker, account type, strategy structure, and contract specifications, so the clean payoff comparison should not be treated as a universal capital requirement rule.

The core difference is premium direction, not safety

A credit spread begins with cash coming in. A debit spread begins with cash going out. That difference affects how the spread is measured, but it is not a safety ranking.

Receiving premium can make a position look more forgiving because the credit can create some room before the spread reaches loss. The tradeoff is that the maximum profit before costs is usually capped at the credit received, while the short option leg still needs review.

Paying premium can make a position look more demanding because the spread needs enough favorable movement to overcome the debit. The tradeoff is that the maximum loss before costs is commonly tied to the debit paid, while the payoff remains capped by the strike width.

How the payoff boundary changes

The payoff boundary is shaped by strike distance, net premium, and expiration behavior. A credit spread and a debit spread may both have defined expiration payoff ranges, but they reach those ranges from different starting points.

| Payoff question | Credit spread reading | Debit spread reading |

|---|---|---|

| What is paid or received at entry? | The position starts with a net credit. | The position starts with a net debit. |

| What must happen for the best simplified expiration result? | The spread usually needs the underlying to stay away from the short strike or finish in a favorable zone. | The spread usually needs the underlying to move far enough into the favorable zone to overcome the debit. |

| What creates the breakeven? | The credit offsets part of the strike boundary. | The debit raises the amount of favorable movement needed. |

| What can distort the textbook boundary? | Bid/ask spreads, early assignment, liquidity, expiration timing, and transaction costs. | Bid/ask spreads, exercise decisions, liquidity, expiration timing, and transaction costs. |

A payoff diagram is a simplified expiration map. It does not fully describe early assignment, exercise behavior, liquidity, bid/ask spreads, changing implied volatility, or how the spread behaves before expiration.

Same outlook, different spread reading

Consider a simplified investor-oriented scenario where the underlying is expected to move moderately higher or remain stable through the same expiration family. Two spread structures can express that general view in different ways.

| Structure | Initial cash flow | What the structure needs | Main review point |

|---|---|---|---|

| Bull call debit spread | Pays a net debit. | The underlying generally needs enough favorable movement for the spread value to exceed the debit before costs. | Time decay can matter if the move is delayed, and the payoff is capped by the short call. |

| Bull put credit spread | Receives a net credit. | The underlying generally needs to stay above the relevant downside boundary for the credit to be retained before costs. | The short put can create assignment review, especially near expiration or when the option is in the money. |

The same broad market view can therefore produce different risk questions. The debit version asks whether the move can overcome the upfront cost. The credit version asks whether the received premium is enough compensation for the short-leg boundary. Neither answer is automatic.

Where investors often misread the comparison

Receiving premium is not the same as low risk. A credit spread can still lose more than the credit received before costs if the underlying moves through the adverse boundary.

Paying premium is not automatically worse. A debit spread starts with an upfront cost, but that cost also defines the simplified maximum loss before costs in many standard expiration examples.

Probability language can hide payoff asymmetry. A spread that appears to have more room before loss may also have a smaller maximum gain before costs relative to the capital at risk.

Defined risk is not the same as no operational risk. Short option legs can still require assignment or exercise review, and real fills can differ from clean theoretical examples.

Volatility, time decay, and short-leg review

Many credit-spread examples are discussed through positive time-decay exposure when price stays in a favorable zone, but the net effect still depends on strike placement, time to expiration, implied volatility, and how both legs behave. A strong adverse move, widening spreads, poor liquidity, or changing implied volatility can still offset the clean textbook effect.

Debit spreads often need favorable movement before time decay erodes too much of the spread value. A debit spread may still benefit from the right price path, but the initial debit, strike width, time to expiration, and changing implied volatility all shape the result.

Implied volatility rank or percentile can provide context, but it is not a complete decision rule. Price movement, bid/ask spreads, commissions, expiration timing, strike distance, liquidity, and the relationship between the long and short legs can dominate a simple “credit versus debit” label.

Assignment and exercise review

Any spread with a short option leg can require assignment or exercise review. This matters most when the option is American-style, close to expiration, in the money, near an ex-dividend date for equity options, or affected by interest-rate and contract-specific details.

A defined-risk spread can reduce the simplified expiration range of outcomes, but it does not remove the need to understand how the legs behave before expiration. The short leg, long leg, broker rules, contract specifications, and exercise process can all matter.

The practical review is not only “What does the expiration diagram show?” It is also “What happens if the short leg is assigned, liquidity is poor, the spread is hard to close, or the position behaves differently before expiration than the simplified payoff map suggests?”

When to review credit-spread and debit-spread mechanics

Review credit-spread mechanics when the main question is how net premium received, short-leg placement, breakeven, and defined payoff boundaries work together.

Review debit-spread mechanics when the main question is how net premium paid, capped payoff potential, breakeven, and time decay interact.

The useful distinction is structural: the credit or debit label explains the starting cash flow, not the full strike, expiration, exercise, liquidity, or execution profile.

Credit spread vs debit spread FAQ

Is a credit spread safer than a debit spread?

No. Risk depends on strikes, premium, expiration, costs, liquidity, option style, and short-leg behavior. Premium received or paid does not make either structure automatically safer.

Can both credit spreads and debit spreads be bullish or bearish?

Yes. Each can be constructed with calls or puts depending on the structure. The important distinction is the net premium received or paid, not a fixed bullish or bearish label.

Why does volatility matter in credit spreads vs debit spreads?

Volatility affects option premiums and spread values, but it is only one input. Price movement, time decay, bid/ask spreads, transaction costs, liquidity, and expiration behavior also matter.