Types of economic moats classify the source of a company’s potential competitive advantage. An economic moat is a durable business advantage that may help a company defend profits, returns, or market position over time. The moat label is only useful when it can be tested against customer behavior, financial evidence, and competitive response.

Definition: An economic moat type identifies where a possible advantage may come from, such as switching costs, network effects, scale, brand, intellectual property, regulation, data, or capital intensity. It is a classification tool, not proof of durability by itself.

Key points about economic moat types

- Moat types classify possible sources of competitive advantage, not final investment quality.

- Each moat type requires different evidence, such as customer retention, margins, returns, cash conversion, pricing behavior, or reinvestment needs.

- False positives are common because strong narratives can appear before durable economics show up.

- The strongest moat reading connects the business explanation to measurable operating and financial evidence.

What the types of economic moats actually classify

Moat types separate the possible source of advantage from the evidence that supports it. A company may appear protected because customers are locked in, because its cost base is lower, because its network becomes more useful as participation grows, or because regulation limits new entrants.

The investor question is not only “which moat type is this?” The stronger question is whether that moat type appears in the numbers and in customer behavior. A brand advantage should show more than name recognition. A scale advantage should show more than large revenue. A network effect should show more than many users.

Moat classification is useful because it tells the investor where to look next. The evidence for a switching-cost moat differs from the evidence for a cost advantage, and both differ from the evidence for a regulatory barrier or data advantage.

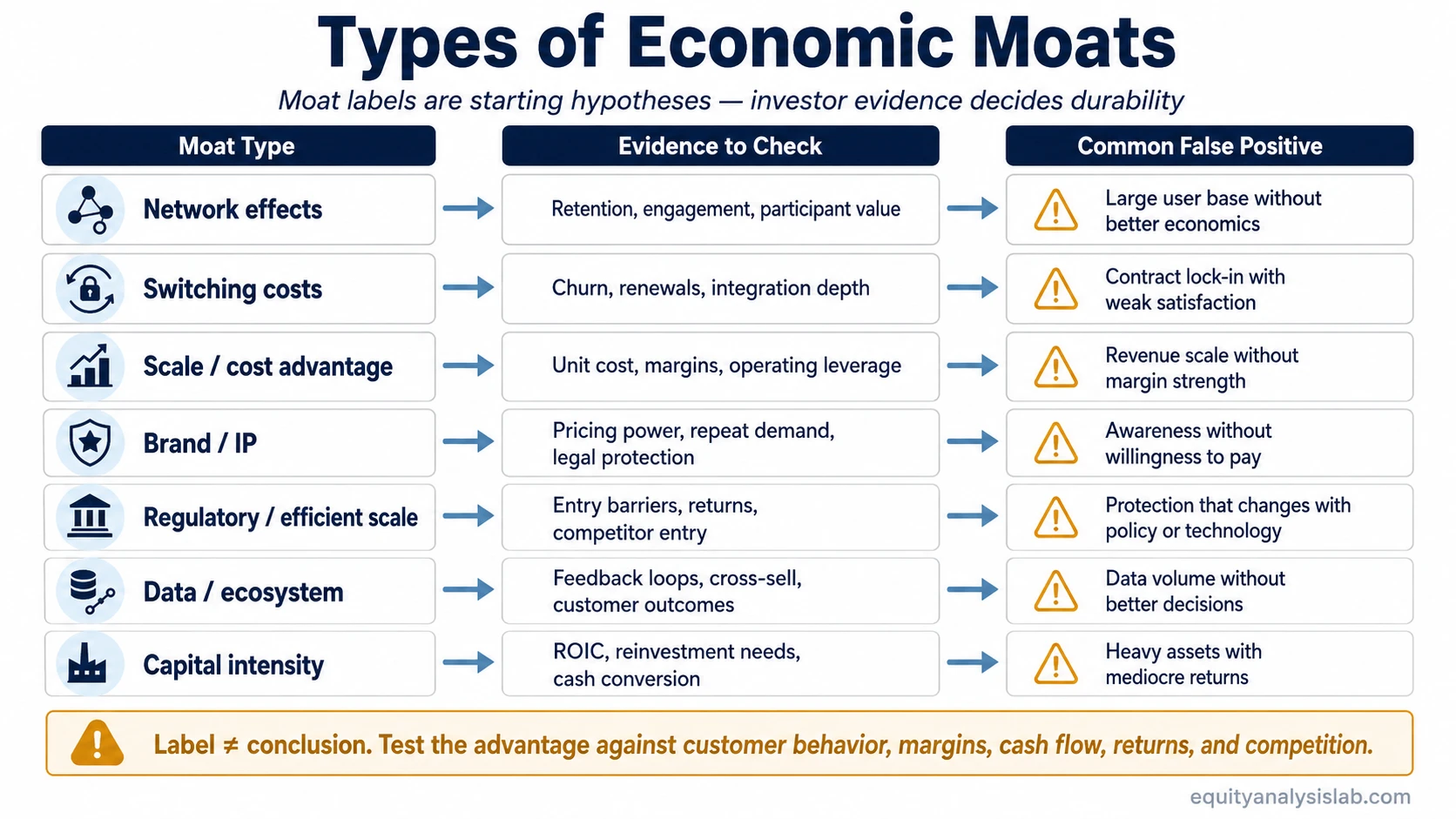

Types of economic moats investors usually test

| Moat type | What it means | Evidence to check | Common false positive |

|---|---|---|---|

| Network effects | The product or service can become more valuable as more users, suppliers, developers, or participants join. | User retention, engagement depth, transaction volume, customer acquisition efficiency, margin stability, and whether added users improve the product’s value. | A large user base that does not improve economics, retention, or customer value. |

| Switching costs | Customers may stay because changing providers is difficult, expensive, risky, or operationally disruptive. | Renewal rates, churn, net retention, contract length, integration depth, pricing behavior, and customer dependence on the product. | Customers remain because contracts are hard to exit, while satisfaction, margins, or product relevance are weakening. |

| Cost advantage / economies of scale | A company may produce, distribute, acquire customers, or operate at lower cost than smaller or weaker competitors. | Gross margin stability, operating leverage, cost per unit, supplier terms, distribution efficiency, and unit economics. | Revenue scale that does not translate into stronger margins, better cash conversion, or sustainable returns. |

| Intangible assets / brand / IP | Brand, patents, licenses, proprietary knowledge, or reputation may support demand or protect economics. | Pricing power, repeat purchase behavior, patent life, legal protection, customer willingness to pay, and margin resilience. | Brand awareness that does not support price, retention, margin quality, or defensible customer preference. |

| Efficient scale / regulatory barriers | A market may only support a few efficient competitors, or rules and approvals may limit new entrants. | Market size, capacity discipline, regulatory licenses, local market structure, returns on capital, and competitor entry behavior. | Regulation that protects incumbents temporarily but changes when policy, technology, or market structure shifts. |

| Data / ecosystem advantage | Data depth, product breadth, integrations, or ecosystem participation may improve customer value and retention. | Data feedback loops, product adoption across modules, retention, cross-sell quality, customer outcomes, and margin contribution. | Large data sets or broad product menus that do not improve decisions, retention, or economics. |

| Capital intensity as barrier | High required investment may discourage new entrants if incumbents can earn adequate returns on that capital. | Maintenance capital needs, reinvestment burden, asset utilization, return on invested capital, and cash conversion. | Heavy assets that deter competitors but also consume cash and depress returns for the incumbent. |

How moat type changes investor interpretation

Different moat types point to different tests. A moat story becomes more useful when it can be compared against margins, cash conversion, retention, reinvestment needs, and competitive behavior.

| If the moat claim is based on… | The investor should look for… | The interpretation weakens when… |

|---|---|---|

| Network effects | More participants improve utility, liquidity, matching, data quality, or ecosystem value. | Growth requires rising incentives, discounting, or acquisition spend without better retention or economics. |

| Switching costs | Customers renew because the product is embedded in workflow, not only because exiting is inconvenient. | Churn rises after contract expiry, customers downgrade, or competitors reduce migration friction. |

| Cost advantage | Scale lowers unit cost and supports margin resilience without constant price cutting. | Scale grows but operating margins, gross margins, or cash conversion fail to improve. |

| Brand or intangible assets | Customers pay, return, or choose the product because the brand or protected asset changes behavior. | Recognition is high but pricing, repeat purchase, or margin evidence is weak. |

| Regulatory or efficient scale barriers | Entry barriers remain difficult to bypass and incumbents still earn acceptable returns. | Rules change, new technology lowers entry costs, or protected returns attract political or competitive pressure. |

| Capital intensity | Large investment requirements protect the business while returns remain above the cost of capital. | The business needs heavy ongoing reinvestment just to defend its position. |

Financial evidence matters because a moat narrative can sound persuasive before it appears in results. Durable advantage is usually more credible when it supports returns, margins, retention, and free cash flow instead of relying only on market share or brand language.

A compact example of moat evidence

A subscription software company may appear to have switching costs because customers dislike migration. That reading becomes stronger if retention remains high without heavy discounting, product usage deepens over time, and margins stay resilient. It becomes weaker if customers stay mainly because contracts are hard to exit while pricing pressure rises and cash conversion deteriorates.

Wide moat vs narrow moat

Wide moat and narrow moat language describes estimated durability, not a separate moat source. A wide moat reading implies the advantage may last longer or resist competition better. A narrow moat reading implies the advantage may exist but with less duration, less evidence, or more vulnerability.

The distinction becomes more useful when the same moat type is checked against competitive pressure, customer dependence, reinvestment needs, and return quality.

Common mistake: treating the label as the conclusion

The most common mistake is stopping at the label. “Brand,” “network effect,” “scale,” or “data advantage” can sound durable even when the business evidence is mixed. A moat label is a starting hypothesis, not the conclusion.

A brand can lose pricing power. A network can grow without improving economics. Scale can hide weak per-customer economics. Regulation can change. Capital intensity can protect a market while also trapping cash in assets that earn mediocre returns.

The safer investor reading separates the story from the evidence. The moat claim becomes more credible when it is supported by returns, customer behavior, margin quality, cash conversion, and disciplined capital allocation.

How moat types connect back to economic moat analysis

Moat type classification helps organize the first question: where might the advantage come from? Full economic moat analysis then asks whether that advantage is durable, measurable, and still visible after competitive pressure, reinvestment needs, and customer behavior are considered.

Use the moat type as a diagnostic route: network effects point toward participation and retention evidence; switching costs point toward churn and renewal evidence; scale points toward margin and unit-cost evidence; intangible assets point toward pricing and repeat-demand evidence; capital intensity points toward returns and reinvestment quality.

The strongest reading combines qualitative advantage with financial confirmation. The weakest reading relies on a strong story while returns, margins, retention, or cash flow move the other way.

FAQ

Is brand always an economic moat?

No. Brand becomes more moat-like when it affects customer behavior, pricing, repeat demand, or margin resilience. Recognition alone is not enough.

Can a company have more than one moat type?

Yes. A company can combine several advantage sources, such as brand, scale, and switching costs. The investor still needs evidence that the combined advantages support durable economics.

Does having an economic moat make a stock a good investment?

No. A moat can be relevant to business quality, but valuation, financial strength, growth durability, risk, and future expectations still matter.