Return on invested capital measures how much after-tax operating profit a company generates from the capital invested in its operations. The usual ROIC formula is NOPAT divided by average invested capital. ROIC is a capital-efficiency diagnostic, not proof of business quality, valuation attractiveness, or future stock performance.

Definition: Return on invested capital, often shortened to ROIC, compares after-tax operating profit with the capital a company uses to run and grow the business.

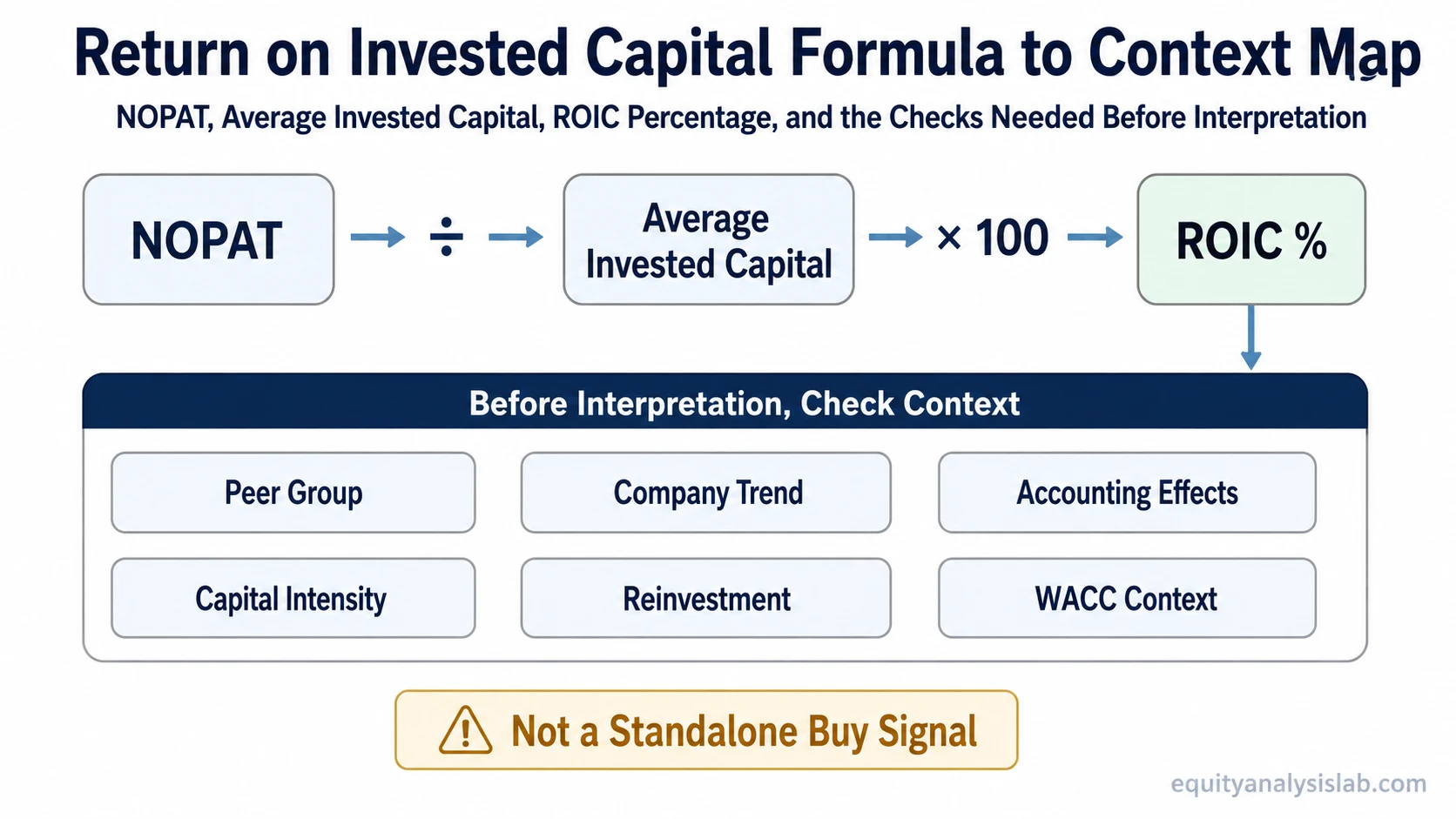

Core formula: ROIC = NOPAT / Average Invested Capital.

Interpretation boundary: A higher ROIC can be useful, but it still needs context from peers, company history, accounting choices, reinvestment needs, and the durability of operating profit.

Key Points

- Return on invested capital focuses on operating profit after tax, not simple net income.

- Invested capital is the operating capital deployed in the business, not total assets by default.

- ROIC is most useful when compared with similar companies and with the same company over time.

- A strong ROIC figure can mislead if the denominator is distorted, the cycle is unusually favorable, or future reinvestment opportunities are limited.

What Is Return on Invested Capital?

Return on invested capital is a profitability and capital-efficiency metric. It asks a specific question: how much after-tax operating profit does the business produce for each unit of capital invested in its operations?

The operating focus matters. ROIC is usually built around NOPAT, which stands for net operating profit after tax. That keeps the numerator closer to operating performance and reduces the influence of financing structure, unusual below-the-line items, and shareholder-equity accounting.

The denominator also matters. Invested capital is meant to capture the capital used by the operating business. It is not the same as total assets, and it is not limited to shareholder equity. That is why ROIC can tell a different story from asset-based or equity-based return metrics.

Return on Invested Capital Formula

ROIC = NOPAT / Average Invested Capital

When expressed as a percentage, the result is multiplied by 100.

NOPAT is after-tax operating profit. Average invested capital is usually calculated by averaging invested capital at the beginning and end of the period, although exact definitions can vary by analyst, company, and data provider.

A simplified version of NOPAT often starts with operating income, or EBIT, and applies an estimated tax rate. A simplified invested-capital calculation usually starts with operating working capital and operating long-term assets, then adjusts for non-operating assets when the data allows.

Because ROIC is sensitive to definitions, two analysts can calculate slightly different ROIC figures from the same company. The important part is to keep the method consistent when comparing companies or tracking the same company over time.

What Goes Into NOPAT and Invested Capital?

The useful starting point is to separate observable inputs from interpretation. The inputs come from financial statements. The interpretation comes after the analyst checks whether those inputs are representative, comparable, and economically meaningful.

| Input | What it tries to capture | Common issue |

|---|---|---|

| NOPAT | Operating profit after tax, before financing effects | Can be distorted by unusual operating gains, losses, tax assumptions, or one-time items |

| Average invested capital | Capital deployed in the operating business across the period | Can be affected by acquisitions, write-downs, lease treatment, cash adjustments, and working-capital swings |

| ROIC percentage | Operating return generated on invested capital | Can look strong or weak for reasons that require peer and historical context |

This is why ROIC should be read as a diagnostic rather than a mechanical ranking tool. The calculation is useful only when the numerator, denominator, and comparison set are reasonably consistent.

How to Interpret ROIC

ROIC usually becomes more useful when it is interpreted through several layers of context. A single number rarely explains whether a business is improving, whether its economics are durable, or whether the market already reflects that quality.

| Context check | Why it matters |

|---|---|

| Peer group | Capital intensity differs by industry, so cross-industry comparisons can mislead. |

| Company trend | A rising or falling ROIC trend can reveal more than a single-period figure. |

| Accounting effects | Write-downs, acquisitions, leases, and tax assumptions can change the numerator or denominator. |

| Reinvestment opportunity | A high current ROIC is less useful if the company cannot reinvest much capital at attractive operating returns. |

| Cost of capital | Comparing ROIC with WACC can help frame value creation, but only after assumptions are checked. |

Two companies can have similar ROIC figures but very different investment implications. One may operate in a stable, asset-light business with repeatable economics. Another may show a temporarily high ROIC because capital has been written down, demand is unusually strong, or reinvestment needs are low. The same percentage can therefore mean different things once business model, accounting, and capital intensity are compared.

What Is a Good ROIC?

A good ROIC depends on the company, industry, accounting base, and cost of capital. In general, a higher ROIC is more favorable than a lower one, but the conclusion is incomplete without context.

For a capital-light software business, a high ROIC may reflect scalable economics and limited tangible capital needs. For a manufacturer, utility, bank, retailer, or energy producer, capital intensity and accounting treatment can make ROIC comparisons much more complicated.

Important limitation: A high ROIC does not automatically mean a stock is undervalued, low risk, or likely to outperform. Valuation, growth durability, competitive position, reinvestment runway, balance-sheet risk, and expectations still matter.

ROIC vs ROA and ROE

ROIC is often compared with return on assets and return on equity, but the three metrics answer different questions.

| Metric | Basic focus | Typical denominator |

|---|---|---|

| ROIC | Operating return on capital invested in the business | Average invested capital |

| ROA | Profit relative to the asset base | Average total assets |

| ROE | Profit relative to shareholder equity | Average shareholders’ equity |

ROIC can be more useful when the analyst wants to focus on operating capital rather than total assets or equity. ROA can be better for broad asset efficiency, while ROE can be more affected by leverage, buybacks, and equity accounting.

ROIC and Asset Turnover

ROIC can be connected to margin and capital turnover. A company may generate a high return on invested capital because it earns strong operating margins, because it turns invested capital efficiently, or because both are true.

This makes asset turnover ratio a useful related metric. Asset turnover does not replace ROIC, but it helps explain whether returns are coming from efficient use of the asset base rather than from margin alone.

Example: A retailer may operate with thin margins but high turnover. A software company may operate with high margins and low tangible capital needs. Both can show attractive return characteristics, but the drivers are different.

Common ROIC Mistakes

| Mistake | Why it creates risk |

|---|---|

| Treating ROIC as a stock recommendation | ROIC is a business metric, not a valuation conclusion or buy signal. |

| Comparing unrelated industries | Different capital intensity can make the same ROIC level mean different things. |

| Ignoring accounting adjustments | Write-downs, acquisitions, leases, and tax assumptions can distort comparability. |

| Using one year in isolation | Cyclicality or temporary margin strength can make one period unrepresentative. |

| Ignoring reinvestment runway | A company may have high current ROIC but limited ability to deploy more capital at similar returns. |

When ROIC Is Most Useful

ROIC is most useful when the analyst wants to understand operating capital efficiency. It is especially relevant for comparing companies that compete in similar industries, use similar accounting definitions, and have comparable business models.

It is less useful when the data is not comparable, when invested capital is difficult to define, or when recent accounting events have heavily altered the denominator. In those cases, ROIC should be supported by margin analysis, cash-flow analysis, balance-sheet review, and valuation work.

Practical reading: ROIC can help identify whether a business has historically converted operating capital into after-tax operating profit efficiently. It does not answer whether the stock price is attractive, whether future returns will remain high, or whether the business can reinvest at the same rate.

Related Metrics to Check With ROIC

ROIC should usually be read with other profitability, efficiency, and cash-flow metrics. Related metrics can show whether returns are supported by margins, asset use, cash conversion, and balance-sheet structure.

| Related metric | What it adds |

|---|---|

| Gross margin | Shows product or service profitability before operating expenses. |

| Operating margin | Shows operating profitability before interest and taxes. |

| Net margin | Shows bottom-line profitability after all expenses. |

| Free cash flow | Helps test whether accounting profit converts into cash after capital spending. |

| Debt-to-equity ratio | Shows how financing structure may affect risk and equity-based return metrics. |

FAQ

Is ROIC the same as return on equity?

No. ROIC focuses on after-tax operating profit relative to invested operating capital. Return on equity compares profit with shareholder equity and can be more affected by leverage and equity accounting.

Is a high ROIC always good?

No. A high ROIC can be useful, but it can also reflect accounting choices, a small invested-capital base, cyclical profit strength, or limited reinvestment opportunity. It needs context before interpretation.

How does ROIC relate to WACC?

ROIC can be compared with a company’s cost of capital to frame value creation, but that comparison still needs assumptions, business context, and valuation work. It should not be treated as a standalone buy signal.