ETF currency exposure is not always visible from an ETF name, trading currency, or share class currency. The real exposure can come from the ETF’s underlying holdings, index design, hedge status, fund mechanics, and the investor’s own base currency.

Definition: ETF currency exposure is the way currency movements can affect an investor’s realized ETF return after the ETF’s holdings, fund structure, hedge policy, and investor base currency are considered together.

For ETF selection, the key point is separation. The currency used to quote or trade an ETF is not always the same as the currency risk embedded in the assets the ETF owns. A fund can trade in one currency, hold securities tied to several other currencies, follow an index built from overseas markets, and still be evaluated by an investor whose portfolio is measured in a different base currency.

That makes currency exposure a diagnostic variable, not a standalone reason to choose or reject an ETF. It helps explain why two funds with similar names or similar regional labels may behave differently after costs, tracking, liquidity, distributions, hedge status, and currency translation are considered.

Key Points

- ETF currency exposure depends on underlying holdings and fund design, not only the ETF’s quoted currency.

- A share class currency can describe how the ETF is listed or accounted for, while the economic exposure may come from the assets inside the fund.

- Hedged and unhedged ETFs should be compared by hedge method, cost, tracking behavior, and portfolio role, not by label alone.

- Currency exposure can affect realized return, but it does not forecast return or prove fund quality.

What ETF Currency Exposure Means

ETF currency exposure describes how exchange-rate movements can influence the value of an ETF for a specific investor. The exposure may come from foreign securities, foreign-currency bonds, cash holdings, derivatives, index methodology, currency hedging, or the difference between the investor’s base currency and the currencies represented inside the fund.

For example, an investor whose portfolio is measured in U.S. dollars may buy an ETF that gives exposure to non-U.S. companies. Even if the ETF trades in U.S. dollars, the underlying companies, local market prices, and currency translation effects may still create non-dollar exposure. This is why an international ETF can require more currency review than its trading line suggests.

The same logic applies in reverse. An ETF can look foreign because it tracks overseas assets, but part of the currency effect may be reduced, altered, or targeted through a hedging policy. The relevant question is not simply “what currency is shown on the listing?” The better question is “which currency layers can change the investor’s realized outcome?”

Why Fund Currency and Underlying Exposure Can Differ

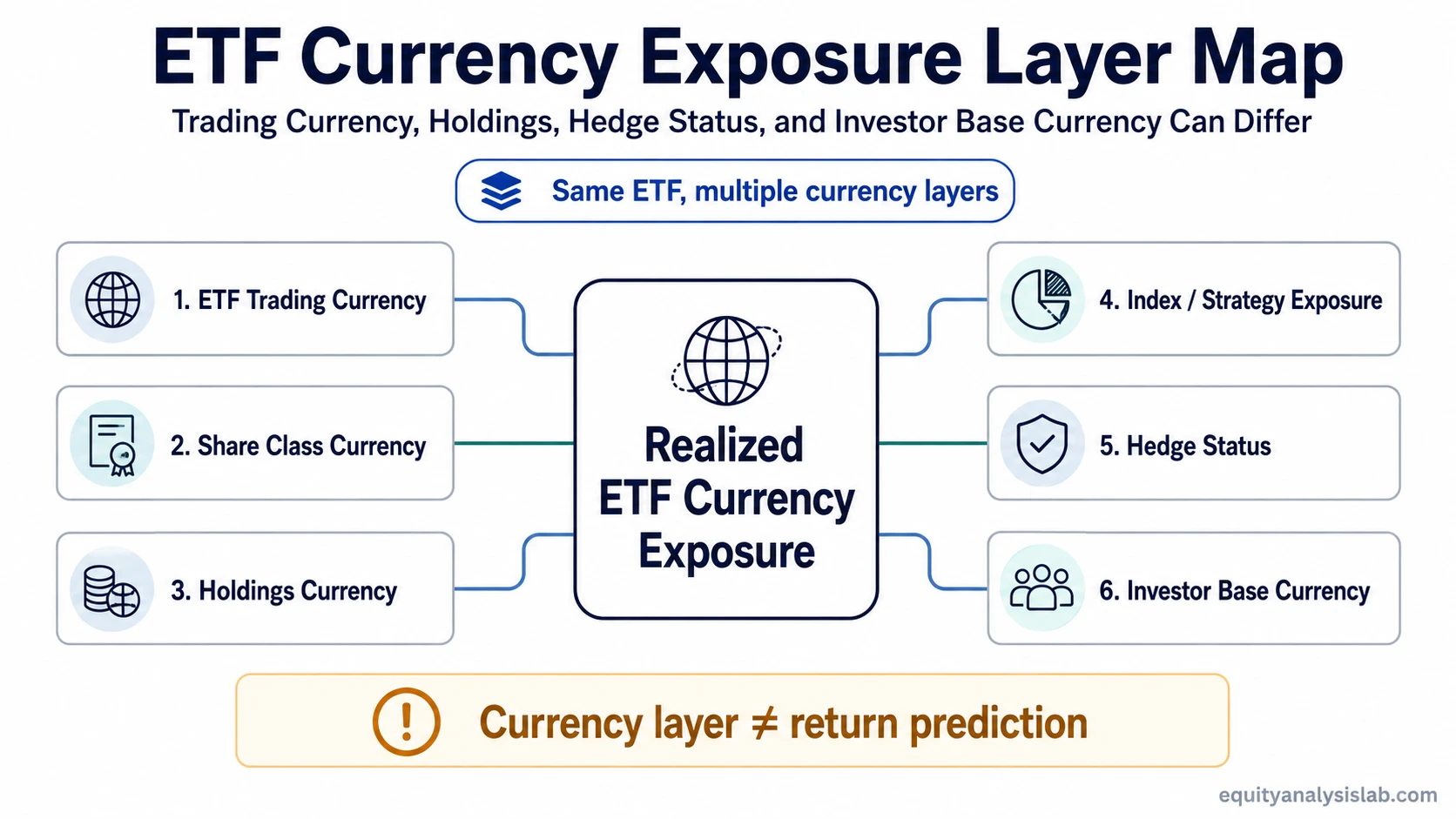

An ETF can have several currency labels at the same time. One label may describe the exchange trading currency. Another may describe the share class currency. The holdings may be denominated in different currencies again. The index may use its own base currency for reporting. The investor may measure returns in another currency entirely.

This is the common source of confusion. The ETF’s visible quote is often the easiest layer to see, but it may be the least complete description of the fund’s economic exposure. A U.S.-dollar quoted ETF can still hold assets whose returns are affected by the euro, yen, pound, franc, Canadian dollar, or emerging-market currencies. A local-currency listed share class can still track the same underlying basket as another share class, with translation effects appearing through the investor’s reporting currency.

Hedging adds another layer. A currency-hedged ETF may try to reduce selected currency movements relative to a target currency, but the result still depends on hedge design, rebalancing, costs, tracking behavior, and the exact exposure being hedged. Hedging should therefore be treated as a fund-design feature, not as a guarantee that currency effects disappear.

The Main Currency Layers to Separate

The most useful way to read ETF currency exposure is to separate the layers before comparing funds. Each layer answers a different question.

| Currency layer | What it describes | Why it matters in ETF selection |

|---|---|---|

| ETF trading currency | The currency in which the ETF is quoted or traded on an exchange. | It affects execution, reporting, and visible price display, but it may not describe the fund’s real economic exposure. |

| Share class currency | The currency attached to a specific share class or listing line. | It can affect reporting and investor comparison, but it should not be confused with the holdings’ currency exposure. |

| Underlying holdings currency | The currencies tied to the securities, cash, or instruments inside the ETF. | This often drives the core currency exposure that affects translated returns. |

| Index or strategy exposure | The currency assumptions, market selection, and methodology behind the ETF’s benchmark or strategy. | Two ETFs can track different versions of a similar market exposure if the index or strategy treats currency differently. |

| Hedge status | Whether the ETF uses a currency hedge, what it hedges, and relative to which currency. | It can change currency sensitivity, costs, and tracking behavior without making the ETF automatically better or safer. |

| Investor base currency | The currency in which the investor measures portfolio returns and liabilities. | The same ETF can create different realized currency effects for investors with different base currencies. |

What to Check Before Comparing ETFs

Currency exposure should be reviewed alongside the rest of the ETF selection process. A currency layer that looks attractive in isolation may be less useful if the fund has weaker liquidity, higher costs, poor tracking consistency, or a structure that does not match the investor’s role for the position.

ETF currency exposure checklist:

- Which currency does the ETF trade in?

- What is the share class currency?

- Which currencies are represented by the underlying holdings?

- Does the index or strategy introduce currency assumptions?

- Is the ETF hedged, unhedged, or partially hedged?

- What are the hedge costs and rebalancing effects?

- How does the currency layer affect tracking behavior?

- How does the exposure translate into the investor’s base currency?

This checklist works best when used with other ETF comparison variables. Currency exposure should be reviewed with ETF expense ratio, tracking difference, tracking error, liquidity, tax or domicile considerations, distribution policy, and portfolio role.

It is also important to separate currency exposure from fund quality. A hedged ETF is not automatically better than an unhedged ETF. An unhedged ETF is not automatically more “pure.” The right comparison depends on what the investor is trying to measure, what risks the fund introduces, and whether those risks are acceptable in the portfolio context.

A Common ETF Currency Exposure Mistake

A common mistake is assuming that the ETF’s trading currency tells the whole story. For example, a fund that trades in dollars may still hold European or Japanese securities. If the investor’s base currency is also dollars, the quote may look familiar, but the economic exposure can still include foreign-currency translation effects.

Common mistake: Treating the ETF quote currency as the same thing as the ETF’s underlying currency exposure.

The opposite mistake can also occur. A fund may appear foreign because of its listing or market label, but its currency sensitivity may be partly hedged or altered by the index design. That does not remove the need for review. It simply means the review should focus on the actual layers rather than the surface label.

This distinction matters most when comparing funds that appear similar. Two ETFs may both target the same region, sector, or asset class, but one may hedge currency exposure and the other may not. They may therefore behave differently even before differences in costs, liquidity, replication method, or benchmark construction are considered.

When Currency Exposure Can Mislead Investors

Currency exposure can mislead investors when it is read as a prediction or as a simple good-or-bad label. Exchange-rate movements can help or hurt realized returns, but the direction and size of that effect are not known in advance. A currency hedge can reduce selected exposure, but it can also introduce costs, tracking differences, and imperfect alignment with the investor’s actual currency needs.

Limitation: ETF currency exposure is an input for comparison. It does not predict ETF returns, prove fund quality, or decide whether hedging is appropriate for every investor.

Currency effects can also be mixed inside a single ETF. A global equity fund may hold companies that report in one currency, sell products in many currencies, list shares in another currency, and derive revenues across regions. A bond ETF may have issuer currency, payment currency, duration risk, credit risk, and hedge policy interacting at the same time.

Because of those overlaps, currency exposure is best treated as one diagnostic layer inside a broader ETF review. It should clarify what the investor owns, not replace analysis of the fund’s holdings, benchmark, cost structure, trading liquidity, and portfolio purpose.

How ETF Currency Exposure Fits ETF Selection

ETF currency exposure fits ETF selection as a comparison variable. It helps investors ask whether two funds that look similar on the surface actually expose the portfolio to the same underlying currency effects. This is especially useful when reviewing international equity ETFs, global bond ETFs, emerging-market ETFs, commodity-linked ETFs, and hedged share classes.

A careful review starts with the ETF’s visible listing details, then moves inward toward holdings, index design, hedge policy, and investor base currency. That sequence keeps the review anchored in observable fund mechanics instead of opinion about exchange rates.

The final selection question is not “does the ETF have currency exposure?” Most international or cross-border ETFs do in some form. The better question is whether the currency layer is understood well enough to compare the fund against alternatives with different costs, tracking behavior, hedge design, liquidity profile, and portfolio role.

FAQ

Is ETF currency exposure the same as the ETF trading currency?

No. The trading currency is the currency used to quote or transact the ETF on an exchange. ETF currency exposure can also come from the underlying holdings, benchmark methodology, hedge status, and the investor’s base currency.

Can a U.S.-dollar ETF still have foreign currency exposure?

Yes. A U.S.-dollar listed ETF can still hold foreign assets or track overseas markets. The dollar quote does not automatically remove the currency effects connected to the underlying exposure.

Does currency hedging remove all ETF currency risk?

Not necessarily. A hedge may reduce selected currency movements relative to a target currency, but hedge design, costs, rebalancing, tracking behavior, and partial exposures can still affect the final result.

Should currency exposure decide which ETF to choose?

Currency exposure should inform comparison, not decide it alone. ETF selection also depends on holdings, costs, tracking, liquidity, tax or domicile considerations, time horizon, and portfolio role.