A bull call spread and a long call can both express a bullish view, but they do not create the same option exposure. A long call buys direct upside participation by paying one option premium, while the upside is not capped by a second option leg.

A bull call spread also starts with a bullish view, but it adds a short higher-strike call. That short call can reduce the net debit, but it also defines an upper payoff boundary and adds short-leg review before and near expiration.

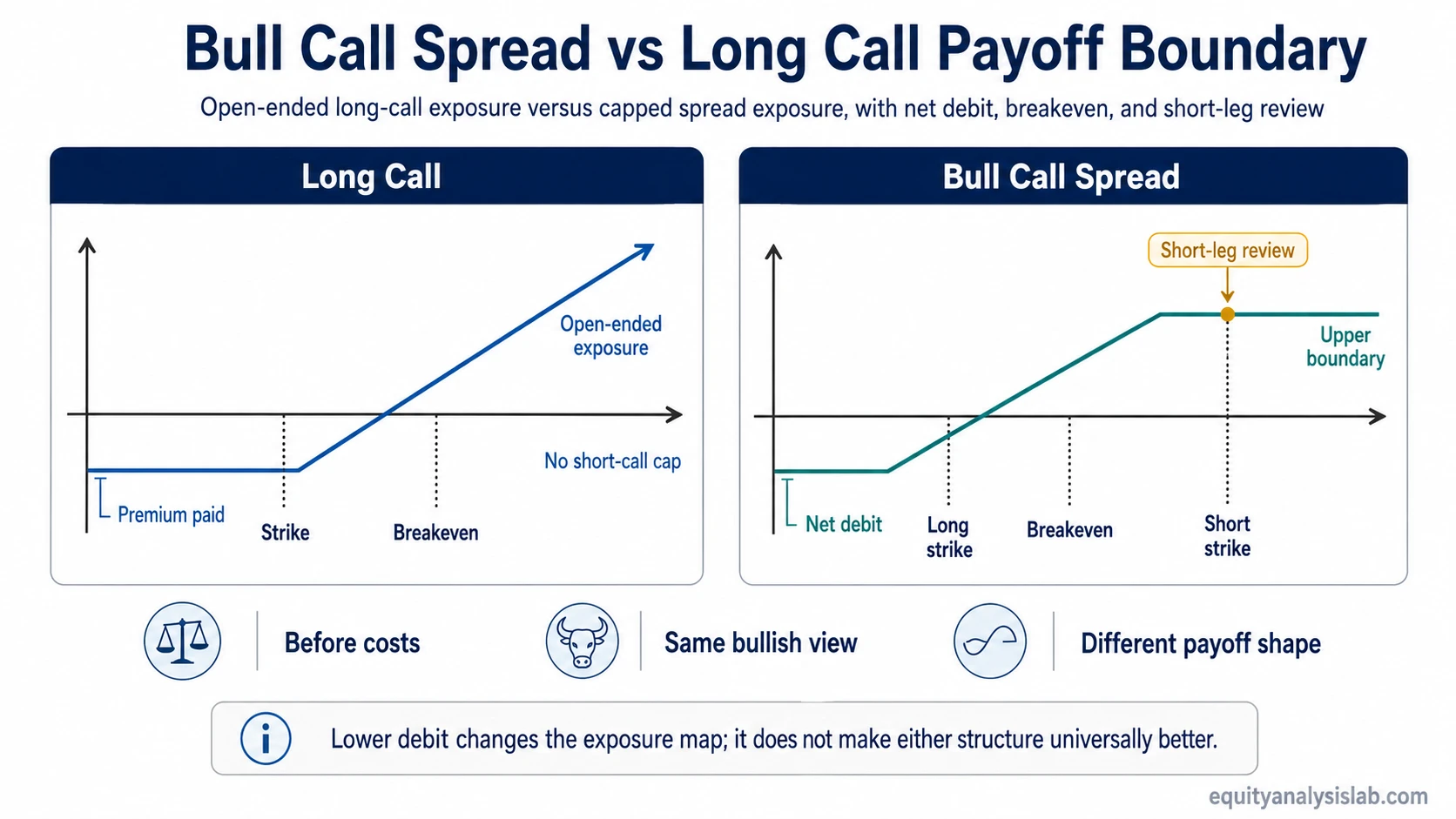

Key Points

- A long call is a single-leg debit position with premium paid and no short-call cap on upside participation.

- A bull call spread is a two-leg debit spread that lowers the upfront debit by selling a higher-strike call.

- The spread’s lower net debit comes with a defined upper payoff boundary at the short strike area.

- The main comparison is exposure design: cost, breakeven, upside boundary, time decay, volatility sensitivity, liquidity, and short-leg obligations.

- Neither structure is universally better; the same bullish view can produce different risk, payoff, and review requirements.

The Core Difference

The useful distinction is not “bullish versus bearish.” Both structures are usually built around a bullish underlying view. The difference is how much of that view remains open-ended after the position is constructed.

Long call: pays one premium for one call option. At expiration, if the underlying moves above the strike plus premium, the option can participate in further upside without a short-call ceiling, before transaction costs and other account-level factors.

Bull call spread: buys a lower-strike call and sells a higher-strike call in the same expiration. The short call helps reduce the debit, but it also caps the spread’s expiration payoff beyond the higher strike before costs and exercise or assignment details are reviewed.

This distinction should be judged by payoff shape rather than by a universal label such as safer, better, cheaper, or higher return.

Comparison Table

The clean comparison is structure and exposure: premium paid, maximum loss, upside boundary, breakeven, time decay, implied volatility sensitivity, liquidity, and short-leg review.

| Criterion | Long Call | Bull Call Spread |

|---|---|---|

| Basic structure | Buy one call option. | Buy a lower-strike call and sell a higher-strike call with the same expiration. |

| Initial premium | Full call premium is paid upfront. | Net debit is paid: long-call cost minus short-call premium received. |

| Maximum loss before costs | Limited to the premium paid if the option expires worthless. | Limited to the net debit if the spread expires out of the money. |

| Upside participation | Not capped by another option leg. | Capped by the short higher-strike call. |

| Maximum gain before costs | Theoretical upside remains open as the underlying rises. | At expiration, strike width minus net debit, before transaction costs and exercise or assignment considerations. |

| Breakeven at expiration | Call strike plus premium paid. | Lower long-call strike plus net debit. |

| Time decay | The long option can lose value as time passes if price movement is not enough to offset decay. | The short call can offset some time decay, but the combined spread still depends on price, time, and volatility. |

| Implied volatility sensitivity | More directly exposed to changes in the value of the long option. | Long-call sensitivity is partly offset by the short call, so the spread may respond differently to IV changes. |

| Liquidity and execution friction | One option leg to evaluate. | Two option legs, two bid-ask spreads, and more closing or adjustment friction. |

| Short-leg review | No short call is created by the structure. | The short higher-strike call requires assignment, exercise, expiration, and liquidity review. |

Same Bullish Thesis, Different Payoff Shape

A common scenario is that an investor expects moderate upside in an underlying asset but wants to compare two ways to express that view. One structure buys a standalone call. The other buys a call and sells a higher-strike call against it.

Illustrative setup: The underlying is below both call strikes when the position is opened. The standalone call has a higher premium because the investor is only buying optionality. The bull call spread has a lower net debit because the higher-strike short call brings in premium.

If the underlying rises modestly: both structures can gain value, but the spread may reach its intended payoff range sooner because its breakeven can be lower when the net debit is smaller.

If the underlying rises far beyond the higher strike: the long call continues to participate through its single long option. The bull call spread stops adding expiration payoff beyond the upper strike boundary because the short call offsets additional upside.

If the underlying does not rise enough: both structures can lose their debit. The difference is that the long call risks the full premium paid, while the bull call spread risks the net debit paid for the spread.

The same bullish thesis therefore produces different exposure. The long call keeps upside open but usually costs more. The bull call spread lowers the debit but converts open-ended upside into a defined range.

Breakeven and Payoff Boundary

At expiration, a long call’s simplified breakeven is the call strike plus the premium paid. The position needs the underlying to move far enough above the strike to recover the premium before the payoff becomes positive before costs.

At expiration, a bull call spread’s simplified breakeven is the lower long-call strike plus the net debit. Because the short call reduces the debit, the breakeven may be lower than a comparable standalone call, but that same short call also defines the upper payoff boundary.

Boundary rule: a lower debit is not the same thing as better exposure. It changes the payoff map by trading some open-ended upside for a defined range between the long strike, breakeven, and short strike.

The ROI, Theta, and IV Confusion Trap

A bull call spread can sometimes show a higher percentage return on debit than a standalone call if the underlying finishes near or above the spread’s upper strike. That can make the spread look superior when the comparison is framed only as return on capital.

That framing is incomplete. Percentage return ignores the fact that the spread has sold away upside beyond the short strike. A fast move far above the short strike can make the standalone call behave very differently from the capped spread.

Common mistake: comparing only the lower debit or possible percentage return without checking what was given up. The short call can reduce cost, offset some time decay, and change volatility exposure, but it also limits the payoff and creates review obligations.

The same issue applies to theta and implied volatility. A long call is more exposed to the long option’s time decay and IV changes. A bull call spread has offsetting long and short option sensitivities, but the result is not mechanically better. It depends on strike distance, time to expiration, price movement, implied volatility, and liquidity.

Short-Leg and Liquidity Review

The short call is the feature that makes the bull call spread different from a standalone call. It reduces the net debit, but it also introduces obligations that a single long call does not have.

Short-leg review: if the short call becomes in the money, the investor needs to review assignment risk, exercise mechanics, expiration behavior, and how the spread would be closed or managed. Contract terms, broker mechanics, account permissions, and market liquidity can all affect the practical outcome.

Liquidity also matters. A standalone long call has one bid-ask spread to evaluate. A bull call spread has two option legs, and the combined price can be affected by bid-ask width, fill quality, early closing costs, and the availability of liquid strikes. A lower theoretical debit may not remain as attractive if execution friction is high.

How to Read the Comparison

The comparison is most useful when the investor separates market view from option expression. The market view may be bullish in both cases. The option expression changes the cost, breakeven, upside boundary, volatility sensitivity, and review requirements.

| Question | What it reveals |

|---|---|

| Is the goal direct upside exposure or a defined upside range? | This separates open-ended long-call exposure from capped spread exposure. |

| How important is the upfront debit? | This shows whether premium reduction is central to the structure. |

| What happens if the underlying moves far beyond the short strike? | This reveals the opportunity cost of the spread’s upside cap. |

| How much do time decay and IV changes matter before expiration? | This keeps the comparison from relying only on expiration payoff diagrams. |

| Can both legs be entered and exited with acceptable liquidity? | This brings bid-ask friction and multi-leg execution into the analysis. |

| Does the structure create short-leg review? | This separates single-option ownership from a spread with a short call. |

FAQ

Is a bull call spread the same as a long call?

No. Both can express a bullish view, but a long call is one long option while a bull call spread combines a long lower-strike call with a short higher-strike call. The short call lowers the net debit and caps the upside.

Why can a bull call spread cost less than a long call?

The spread sells a higher-strike call, and the premium received from that short call reduces the net debit. The lower cost comes with a tradeoff: payoff is capped above the short strike before costs and exercise or assignment details are reviewed.

Does a lower debit make the bull call spread better?

Not by itself. A lower debit changes the breakeven and maximum loss, but it also limits upside beyond the short strike. The better comparison is exposure design, not a universal better-or-worse label.

Does a long call have more upside than a bull call spread?

A standalone long call is not capped by a short call, so its theoretical upside can continue as the underlying rises. A bull call spread has a defined upper boundary because the short higher-strike call offsets gains beyond that area.

What is the main risk difference at expiration?

For a long call, the main expiration risk is losing the premium paid if the underlying does not finish above breakeven. For a bull call spread, the net debit is at risk, but the short call also requires assignment, exercise, and closing review if the spread is near or above the short strike.