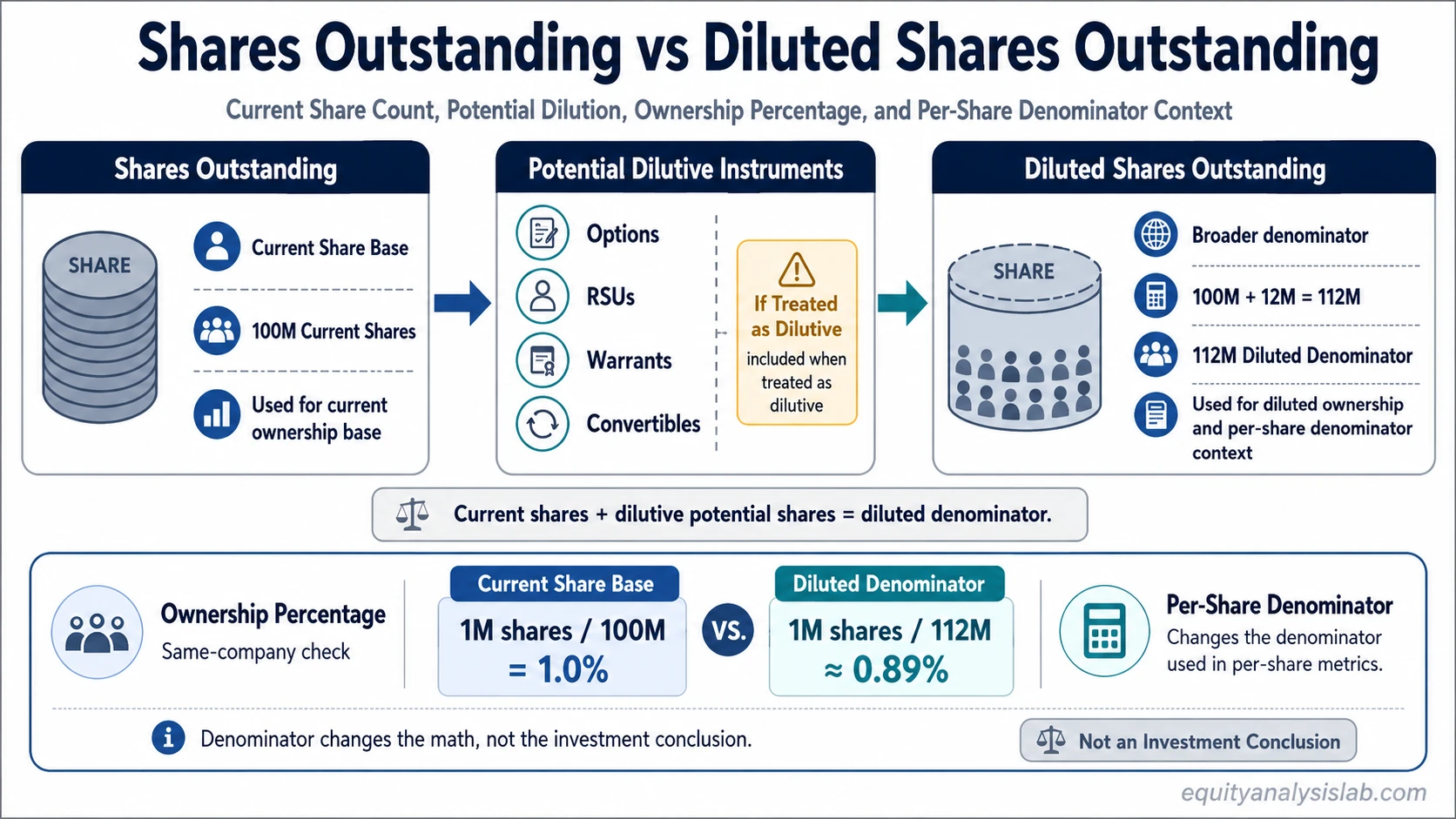

Shares outstanding is the current share count held by shareholders. Diluted shares outstanding is a broader denominator that includes potential shares from dilutive instruments when those instruments are treated as dilutive.

The distinction matters because ownership percentages, per-share metrics, and valuation denominators can look different depending on whether the current share base or diluted share base is used.

Key Points

- Shares outstanding represents the current common shares held by investors, excluding shares that are not currently outstanding.

- Diluted shares outstanding expands the denominator by including potential shares from instruments such as options, RSUs, warrants, or convertibles when they are dilutive.

- The diluted denominator is not the same thing as the shares currently outstanding.

- Neither denominator proves that a stock is attractive, cheap, expensive, high quality, or likely to perform well.

Shares Outstanding vs Diluted Shares Outstanding: Core Difference

Shares outstanding is the current share-count base used to describe how many common shares are actually outstanding at a point in time.

Diluted shares outstanding is a wider share-count base that estimates the share count after including potentially dilutive securities, if those securities are treated as dilutive under the relevant reporting or analysis context.

The core difference is timing and inclusion. Shares outstanding reflects the current equity base. Diluted shares outstanding reflects a broader possible denominator after potential share creation is considered.

| Question | Shares outstanding | Diluted shares outstanding | Investor interpretation boundary |

|---|---|---|---|

| What share base does it describe? | The current common shares outstanding. | The current shares plus potentially dilutive shares when included. | One is current; the other is a broader denominator scenario. |

| What does it usually exclude? | Potential future shares from instruments that have not become common shares. | Instruments that are not dilutive or not included under the relevant method. | The diluted figure is not a simple maximum share count in every possible future state. |

| Which instruments matter? | Common shares already outstanding. | Options, RSUs, warrants, convertible securities, and similar instruments may matter. | The instrument terms and reporting treatment control whether inclusion is appropriate. |

| Where does it affect analysis? | Current ownership base, market capitalization, and current per-share references. | Diluted EPS, ownership dilution checks, and per-share analysis under a wider denominator. | The right denominator depends on the question being asked. |

| What is the main misuse? | Treating the current count as if no future dilution can matter. | Treating the diluted count as if those shares are already outstanding. | Both errors can distort ownership and per-share interpretation. |

When Each Share Count Is Used

Shares outstanding is usually the cleaner denominator when the question is about the company’s current common share base. It is the more direct input for current ownership percentage, current market capitalization, and current share-count references.

In many per-share contexts, basic shares outstanding is the closer match for the current share base, while diluted shares outstanding is used when the analysis needs to include potentially dilutive shares.

Diluted shares outstanding becomes more relevant when the question involves potential dilution. Options, warrants, RSUs, convertible preferred shares, convertible debt, or similar instruments can increase the effective share base if they become common shares or are treated as dilutive for reporting purposes.

For reported figures, the included instruments and final diluted count depend on the company’s filing context and the applicable calculation rules, so the diluted figure should be read as a defined reporting or analysis denominator rather than a casual estimate of every possible future share.

EPS is one important context, but it should not take over the comparison. The denominator question is broader: current ownership and per-share figures can differ from diluted ownership and per-share figures even before any conclusion is made about valuation quality.

Same Company Example

A company has 100 million shares outstanding. It also has 12 million potential shares from employee equity awards, warrants, and convertible instruments that may be included in a diluted share-count analysis.

Under the current-share-count view, the denominator is 100 million shares. Under the diluted-share-count view, the denominator may be 112 million shares if those potential shares are treated as dilutive.

| Measure | Using shares outstanding | Using diluted shares outstanding |

|---|---|---|

| Share-count denominator | 100 million | 112 million |

| Ownership interpretation | A 1 million share position equals 1.0% of the current share base. | The same 1 million share position equals about 0.89% of the diluted share base. |

| Per-share interpretation | Company value or earnings are spread across fewer current shares. | The same company value or earnings are spread across a wider potential denominator. |

The example does not show that the company is good or bad. It only shows how the denominator changes the ownership and per-share math.

Common Confusion About Diluted Shares

A common mistake is treating diluted shares outstanding as if every included share is already issued and trading. Diluted shares outstanding is a denominator used for analysis and reporting context. It is not always the same as the current number of shares actually outstanding.

The reverse mistake is ignoring potential dilution completely. A company can look less diluted on the current share count while still having meaningful equity awards, warrants, or convertible instruments that may affect future ownership and per-share results.

What Diluted Shares Can and Cannot Tell Investors

Diluted shares can help investors see how ownership and per-share numbers might change when potential share creation is included. That is useful when comparing companies with different compensation structures, convertible financing, warrants, or other instruments that can expand the common share base.

Diluted shares cannot, by themselves, prove valuation quality, business quality, expected return, management quality, or investment merit. A higher diluted share count may reflect real dilution risk, but the interpretation still depends on cash flow, earnings quality, growth, balance-sheet context, capital allocation, and valuation.

Denominator Choice Is Not an Investment Conclusion

Shares outstanding and diluted shares outstanding answer different denominator questions. The current count is better for current share-base analysis. The diluted count is better for potential-dilution analysis. Neither number is automatically more conservative, more accurate, or more useful in every context.

The safer approach is to match the share count to the question: current ownership, diluted ownership, current per-share metrics, diluted per-share metrics, or dilution-risk review.

FAQ

Is diluted shares outstanding the same as shares outstanding?

No. Shares outstanding is the current common share count. Diluted shares outstanding is a broader denominator that includes potential shares when dilutive instruments are included.

Why can diluted shares outstanding be higher?

It can be higher because options, RSUs, warrants, convertibles, or similar instruments may create additional common shares or be included in diluted-share calculations.

Which number should investors use?

Use shares outstanding for the current share base. Use diluted shares outstanding when the analysis needs to account for potential dilution, diluted EPS, or a wider ownership denominator.

Does a higher diluted share count make a stock worse?

No. A higher diluted share count can signal dilution to evaluate, but it does not prove poor business quality, weak valuation, or poor future performance by itself.