Top-down investing starts with the outside environment first. Bottom-up investing starts with the individual business first. Both approaches can review the same stock, but they begin with different questions and give different weight to macro, sector, and company evidence.

Key points

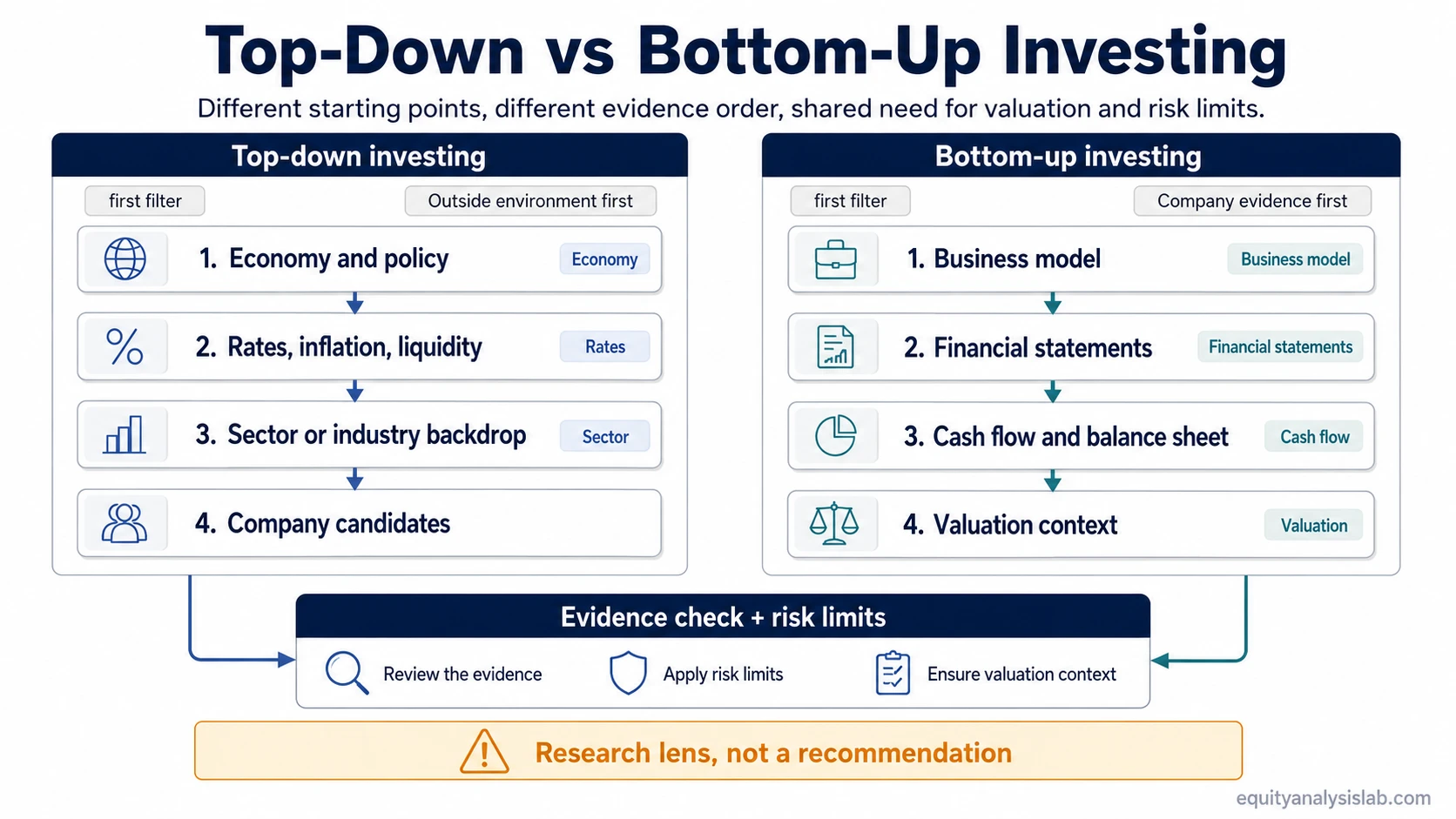

- Top-down investing begins with broad conditions such as the economy, interest rates, policy, sector trends, or market backdrop.

- Bottom-up investing begins with the company itself, including business quality, financial statements, earnings durability, balance sheet strength, and valuation context.

- The same stock can look different under each approach because the research sequence changes what evidence receives priority.

- Neither approach proves that a stock is attractive, safe, undervalued, or suitable for a specific investor.

Top-down vs bottom-up investing: the core difference

Top-down vs bottom-up investing is a difference in research starting point. A top-down investor starts outside the company and asks whether the economic, policy, market, sector, or industry backdrop creates a favorable setting for certain investments. A bottom-up investor starts inside the company and asks whether the business itself has enough quality, durability, cash support, and valuation logic to deserve attention.

The difference is not that one method uses macro evidence and the other ignores it. The difference is sequencing. Top-down analysis uses the outside environment as the first filter. Bottom-up analysis uses company evidence as the first filter.

For a deeper standalone explanation of the outside-in method, see top-down investing. For the company-first method, see bottom-up investing.

Comparison table

| Comparison point | Top-down investing | Bottom-up investing |

|---|---|---|

| Starting question | Which economies, sectors, themes, or market conditions look most attractive? | Which individual businesses look strongest based on company evidence? |

| First filter | Macro, policy, rates, inflation, liquidity, sector conditions, or industry trend. | Business model, financial statements, cash flow, margins, balance sheet, management, and valuation. |

| Typical research path | Economy or market backdrop, then sector, then industry, then company candidates. | Company evidence, then valuation, then industry and macro context. |

| What can make an idea weaker? | A poor macro or sector backdrop can reduce interest even if a company looks strong. | Weak company fundamentals can reduce interest even if the sector or theme looks strong. |

| Best use | Filtering where opportunity may be concentrated across markets, sectors, or themes. | Evaluating whether a specific company can support an investment thesis on its own evidence. |

| Main mistake | Treating a favorable theme as proof that every company in the theme is attractive. | Treating a strong company as immune to valuation, financing, sector, or macro pressure. |

The practical distinction is that top-down investing uses the outside environment as the first filter, while bottom-up investing uses company evidence as the first filter before testing outside conditions.

How top-down investing starts research

A top-down process usually begins outside the company. The investor may start with economic growth, inflation, interest rates, credit conditions, government policy, sector leadership, or industry demand. The goal is to narrow the opportunity set before selecting individual companies.

For example, a top-down investor might first ask whether lower interest rates could support long-duration growth sectors, whether commodity prices could favor energy producers, or whether policy changes could improve demand in a specific industry. Only after that first filter would the investor compare individual companies inside the selected area.

This method is most useful when broad conditions strongly shape company outcomes. Its weakness is that a good backdrop does not automatically make every company inside that backdrop high quality, fairly valued, or financially resilient.

How bottom-up investing starts research

A bottom-up process usually begins at the company level. The investor may start with revenue quality, margins, cash generation, capital allocation, competitive position, debt, dilution, earnings durability, and valuation assumptions. The macro or sector backdrop is still relevant, but it is reviewed after the company-level case begins to take shape.

A bottom-up investor might first ask whether a company earns attractive returns on capital, converts earnings into cash, protects margins, avoids excessive dilution, and trades at a valuation that leaves room for uncertainty. If those company-level checks are weak, a favorable sector story may not be enough.

This method is most useful when company differences matter more than broad category exposure. Its weakness is that a strong company can still face valuation compression, financing stress, cyclical pressure, or changing expectations.

Same-company example: two starting points, two readings

Consider a software company with strong revenue growth, high gross margins, recurring subscriptions, and a valuation that already assumes several years of continued expansion.

A top-down investor may begin with interest rates, liquidity, and market appetite for long-duration growth stocks. If rates are rising and investors are paying less for future earnings, the top-down reading may become cautious before the company’s operating results weaken.

A bottom-up investor may begin with the company’s retention, pricing power, cash flow, balance sheet, and dilution. If those company-level checks remain strong, the bottom-up reading may still find the business attractive, while requiring more care around valuation assumptions.

The point is not that one investor is right and the other is wrong. The same evidence can be organized differently because the first question is different: outside-in conditions for top-down analysis, company-first evidence for bottom-up analysis.

Common confusion: style allocation vs company selection

A common mistake is treating top-down vs bottom-up investing as only an asset allocation debate. Top-down research can influence allocation decisions, but the comparison is broader than deciding how much to place in a sector, country, or asset class.

The distinction also affects company selection. A top-down process may choose a sector first and then look for the strongest companies inside it. A bottom-up process may find a strong company first and then test whether the sector and macro context support or weaken the thesis.

Another mistake is assuming that bottom-up means ignoring macro conditions. A bottom-up process can still review rates, demand cycles, currency exposure, financing conditions, and sector pressure. It simply does not let those factors replace the company-level case as the starting point.

Can investors combine both approaches?

Top-down and bottom-up investing can be combined when the investor keeps the research sequence clear. A hybrid process may use top-down analysis to identify areas where the backdrop is improving, then use bottom-up analysis to avoid weak companies inside those areas.

The reverse can also happen. An investor may find a strong company through bottom-up research, then use top-down analysis to test whether the broader environment supports the valuation, earnings outlook, and risk assumptions.

The combination becomes weaker when broad themes replace company evidence or when company enthusiasm ignores external pressure. A useful hybrid process separates the first filter from the final judgment.

Limits of both approaches

Top-down analysis can identify a favorable backdrop, but it cannot prove that a specific company has durable earnings, good cash conversion, a strong balance sheet, or an attractive valuation. Bottom-up analysis can identify a strong business, but it cannot remove exposure to valuation risk, financing conditions, cyclicality, investor expectations, or sector-level pressure.

Neither approach is a recommendation, risk-tolerance test, suitability screen, performance forecast, or proof of safety. Each method is a research lens. The quality of the conclusion depends on the evidence, assumptions, valuation discipline, and limits applied after the first filter.

FAQ

Is top-down investing better than bottom-up investing?

No. The better approach depends on the research problem. Top-down analysis is useful when broad conditions drive opportunity. Bottom-up analysis is useful when company-specific evidence is the main question.

Does bottom-up investing ignore the economy?

No. Bottom-up investing starts with the company, but it can still review interest rates, demand cycles, financing conditions, sector pressure, and valuation context.

Can the same investor use both approaches?

Yes. An investor can use top-down analysis to understand the backdrop and bottom-up analysis to test whether individual companies have enough quality, cash support, and valuation discipline.