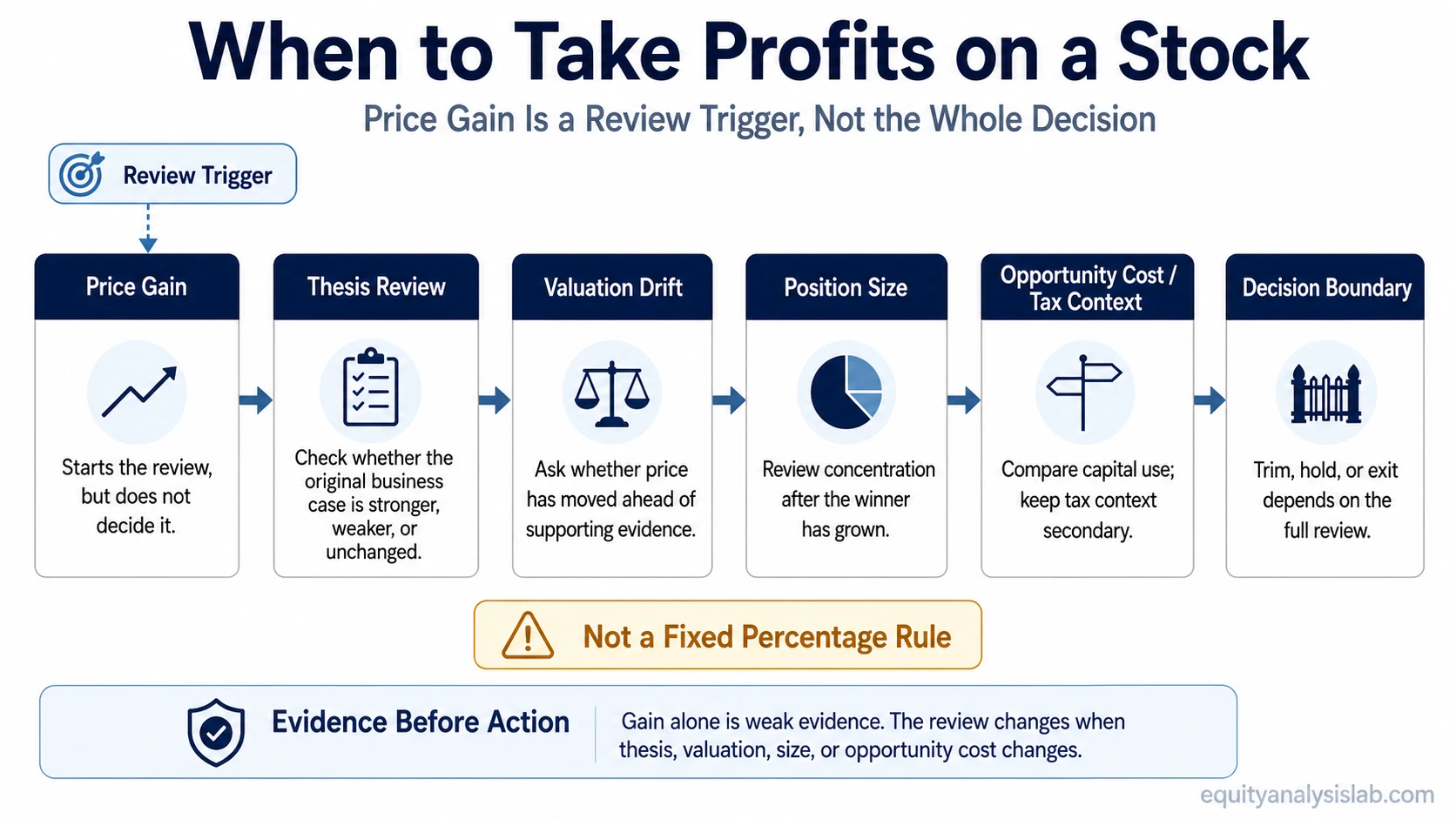

The common mistake is treating a gain as the whole decision. Taking profits on a stock should begin with a review of thesis evidence, valuation, position size, portfolio role, and opportunity cost, not with the question of whether the gain feels large enough.

Common mistake: A rising price can make selling feel prudent simply because the position is profitable. The gain only says that the stock has moved. It does not say whether the original reasoning is stronger, weaker, overvalued, under-supported, or too large for the portfolio.

A more disciplined review separates the profit from the evidence. A winning stock can still deserve ownership if the business case, valuation context, and portfolio role remain reasonable. It can also deserve trimming if the same gain has created concentration risk, reduced future return potential, or made another use of capital more attractive.

What Taking Profits on a Stock Means

Taking profits on a stock means reducing or exiting part of a winning position after its price has risen. The decision can be connected to valuation, concentration, opportunity cost, thesis change, cash needs, or portfolio policy, but the gain itself is not a complete sell signal.

The practical question is not whether the profit is “enough.” The better question is whether the position still deserves the same role, size, and risk exposure after the price move. That review belongs inside an investment discipline process rather than a fixed percentage rule.

The Gain Is a Review Trigger, Not the Whole Decision

A stock can rise for different reasons. Earnings expectations may have improved, valuation multiples may have expanded, the market may have rewarded a temporary catalyst, or the position may simply have become a larger share of the portfolio. Those situations require different interpretations.

If the business case has improved and valuation still leaves room for uncertainty, the gain alone may not justify reducing exposure. If price appreciation has moved far ahead of evidence, the same gain may make trimming more defensible. The decision changes when the facts behind the position change.

Decision boundary: A profit becomes more relevant when it changes the position’s risk, valuation, opportunity cost, or portfolio role. It is weaker evidence when it only reflects that the stock price is higher than the purchase price.

Review the Thesis Before Reviewing the Profit

The first review point is the investment thesis. If the reason for ownership is still intact, the position may deserve a different review than a stock whose thesis has weakened even though the price is up.

Useful thesis questions include whether the company’s operating evidence still supports the original case, whether new risks have changed the expected payoff, and whether the investment case now depends more on momentum or sentiment than on the original business evidence.

Taking profits becomes more defensible when the price gain is paired with weaker evidence, a narrower margin for error, or a thesis that now requires more optimistic assumptions than it did before.

Check Valuation Drift After the Price Move

Valuation drift occurs when the stock price rises faster than the evidence supporting future cash flow, earnings power, growth quality, or business durability. The stock may still be a strong company, but the risk/reward balance can change when the price embeds a much more demanding expectation.

A valuation review does not require a precise target price. It requires comparing current expectations with the evidence available. A stock that was attractive at one price can become more fragile if the new price leaves little room for disappointment.

Limitation: Valuation alone does not mechanically require selling. High-quality businesses can remain expensive for long periods, and a low valuation can still be justified by weak fundamentals. The review should compare valuation with evidence, not treat either side as automatic.

Check Position Size and Concentration Risk

A winner can become riskier for portfolio reasons even if the company’s fundamentals remain intact. After a large gain, the position may represent a larger share of total capital than originally intended. That changes the portfolio question from “is the stock good?” to “is this much exposure still appropriate?”

This is where position size after a large gain becomes part of the profit-taking review. Trimming may reduce concentration while preserving some exposure to the thesis. Holding may be more reasonable when the position remains within the investor’s intended risk range.

Concentration review is especially different from thesis review. A stock can still be attractive as a company while becoming too dominant inside a portfolio.

Partial Profit-Taking vs Full Exit

Partial profit-taking and a full exit solve different problems. Trimming reduces exposure while keeping part of the position connected to the thesis. A full exit is a stronger decision and normally belongs to a different boundary: the thesis, valuation, opportunity cost, or portfolio role no longer supports ownership.

Partial selling can be useful when the thesis remains alive but the position has become too large, valuation has become less forgiving, or portfolio policy requires rebalancing. A full exit is more defensible when the original reason for owning the stock no longer holds or when the capital has a clearly better use elsewhere.

| Decision type | What it means |

|---|---|

| Trim | Reduces exposure while keeping the position connected to the thesis. |

| Hold | Keeps exposure unchanged when thesis, valuation, and portfolio role still support the current size. |

| Full exit | Removes exposure when the ownership case no longer supports the position. |

A Simple Review Framework

The review should compare the current position with the current evidence. The same unrealized gain can lead to different outcomes depending on thesis strength, valuation, portfolio exposure, and competing uses of capital.

| Review question | What it checks | What would support trimming | What would support holding |

|---|---|---|---|

| Has the thesis changed? | Whether the original ownership case still has evidence behind it. | The business case is weaker, more speculative, or more dependent on optimistic assumptions. | The thesis has strengthened or remains supported by current evidence. |

| Has valuation moved faster than fundamentals? | Whether price appreciation has outrun the evidence behind earnings, cash flow, growth, or quality. | The new valuation leaves little room for disappointment or depends on aggressive expectations. | Valuation still appears consistent with the updated business evidence and uncertainty range. |

| Has the position become too concentrated? | Whether the winner now represents more portfolio risk than intended. | The position has grown beyond the investor’s intended exposure or creates single-stock dependence. | The position remains within the intended allocation and risk budget. |

| Is there a better use for capital? | Whether another opportunity offers a more attractive evidence-adjusted use of funds. | The current position has less upside relative to risk than another well-supported opportunity. | The current stock still compares favorably against available alternatives. |

| Does tax or cash context change timing? | Whether implementation factors affect the timing or size of a reduction. | A cash need, portfolio policy, or tax-aware timing consideration supports a measured reduction. | Implementation costs or timing considerations argue against acting before the investment case changes. |

Decision boundary: The strongest profit-taking case usually appears when at least two review inputs point in the same direction, such as stretched valuation and oversized position risk, rather than when price appreciation appears alone.

Simple Taking Profits Scenario

A stock has doubled after several quarters of improving expectations. The tempting shortcut is to say the gain is large enough and reduce the position automatically.

The review changes if the evidence is separated. If earnings quality, cash flow, and business momentum have improved enough to support the new valuation, the gain may be less important than it appears. If valuation has expanded while the business evidence has not improved much, trimming becomes easier to justify.

The same position may also require a portfolio review. A stock that began as a moderate allocation can become the largest holding after a large gain. In that case, the issue may be concentration rather than a broken thesis.

What Taking Profits Should Not Mean

Taking profits should not mean selling only because a fixed percentage gain has appeared. A 20%, 50%, or 100% gain does not carry the same meaning across different companies, valuations, portfolios, tax situations, or opportunity sets.

It also should not mean using a target price as if it guarantees fair value. A target can be a useful planning reference, but the decision still depends on updated evidence, valuation context, concentration, and competing uses of capital.

Not a mechanical rule: Taking profits is not a way to remove all regret, avoid all volatility, or guarantee a better future outcome. It is a structured review of whether the position still deserves the same exposure after a gain.

Tax context can influence execution timing, but it should not replace investment logic. Specific tax decisions depend on the investor’s jurisdiction, account type, holding period, and personal circumstances.

Related Decision Boundaries

Profit-taking is strongest as a review boundary when the gain changes one of four things: thesis support, valuation context, portfolio concentration, or opportunity cost. If none of those has changed, the gain itself is weaker evidence.

Those boundaries prevent two opposite mistakes: selling every winner too early because the gain feels large, or refusing to review a winner because the unrealized profit feels validating.

FAQ

Should I take profits after a stock doubles?

A doubled stock should be reviewed, not automatically sold. The decision depends on whether the thesis has improved, whether valuation has become stretched, whether the position is now too concentrated, and whether there is a better use for the capital.

Is taking profits the same as trimming a position?

Taking profits can mean trimming, but it can also mean a larger reduction or full exit. Trimming reduces exposure while keeping part of the thesis alive. A full exit usually requires a stronger reason, such as thesis deterioration, poor valuation support, or a changed portfolio role.

Should valuation or position size matter more when taking profits?

They answer different questions. Valuation asks whether the stock still offers enough compensation for uncertainty. Position size asks whether the stock has become too large inside the portfolio. A strong business can still create portfolio risk if it grows into an oversized allocation.

Can taxes decide when to take profits?

Taxes can affect timing and implementation, but they should not replace the investment review. Tax treatment depends on personal circumstances, account structure, jurisdiction, and holding period, so specific tax decisions require qualified tax guidance.

When is selling a winner a mistake?

Selling a winner can be a mistake when the only reason is that the price has risen. If thesis evidence, valuation context, position size, and opportunity cost still support the holding, the gain alone may be a weak reason to reduce the position.