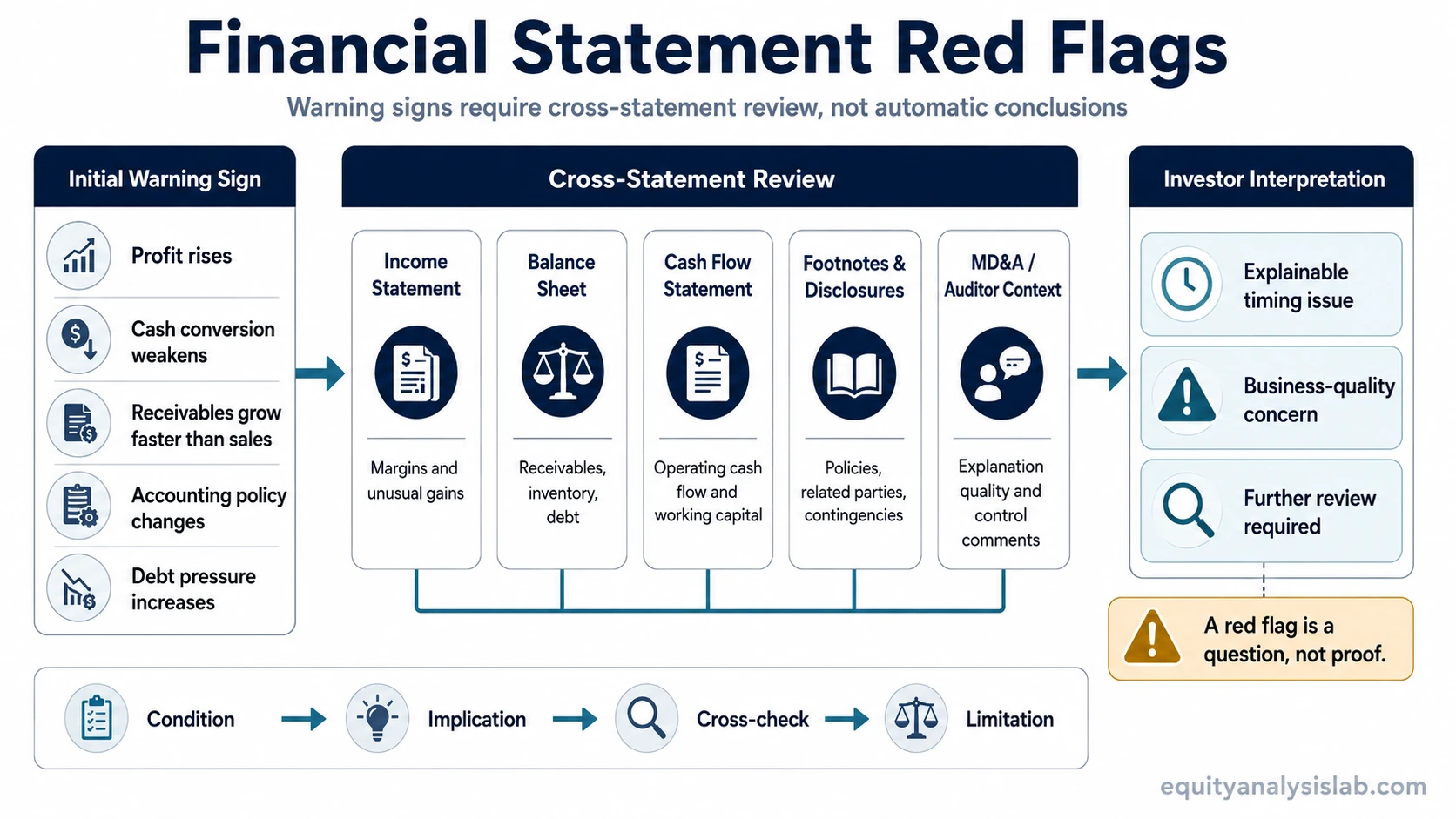

Financial statement red flags are warning signs in a company’s reported numbers, disclosures, or statement relationships that may require deeper investor review. They can point to revenue-quality issues, weak cash conversion, accounting judgment, liquidity pressure, or disclosure risk, but they do not prove fraud or decide investment quality by themselves.

A red flag becomes more useful when it is compared across the income statement, balance sheet, cash flow statement, footnotes, and management commentary. One unusual number is rarely enough. Several weakening relationships at the same time can change the quality of the earnings story.

Key Points

- Financial statement red flags are warning signs that require cross-checking, not standalone conclusions.

- The same red flag can mean different things by sector, accounting policy, business model, and reporting period.

- Cash flow, receivables, inventory, debt, disclosures, and accounting changes need to be reviewed together.

- A red flag becomes more serious when several statement relationships weaken at the same time.

- Red flags can challenge business-quality claims without automatically proving fraud or poor investment quality.

What Financial Statement Red Flags Are

A financial statement red flag is an observable condition that makes reported performance less straightforward than the headline numbers suggest. It may appear as a mismatch between profit and cash flow, a sudden accounting-policy change, unusual balance-sheet growth, unexplained margin movement, aggressive revenue timing, or disclosure language that leaves important risks unclear.

The useful investor question is not whether one red flag proves something bad. The better question is what relationship changed, what could explain it, and what evidence would make the concern stronger or weaker.

For example, rising revenue can look positive, but the interpretation changes if receivables grow faster than sales and operating cash flow falls. That combination can suggest looser payment terms, slower collections, customer strain, or revenue recognition that needs more review. It may also reflect normal timing in a seasonal business. The red flag identifies the question; it does not answer it by itself.

Where Red Flags Appear in the Statements

Financial statement red flags rarely belong to only one statement. The same concern often begins in one line item and becomes clearer only after related statement relationships are compared.

| Statement area | Common red-flag location | Investor interpretation | Important limitation |

|---|---|---|---|

| Income statement | Revenue, margins, expenses, unusual gains | Reported profitability may depend on timing, pricing, cost classification, or non-recurring items. | Margins can move for normal reasons such as mix shift, input costs, investment cycles, or seasonality. |

| Balance sheet | Receivables, inventory, debt, deferred revenue, goodwill | Growth in assets or liabilities may reveal collection risk, demand risk, leverage pressure, or acquisition risk. | Balance-sheet changes need to be compared with revenue growth, cash flow, and business model timing. |

| Cash flow statement | Operating cash flow, working capital, capital expenditure, free cash flow | Cash conversion may be weaker than reported profit suggests. | One weak cash-flow period may reflect working-capital timing rather than a structural issue. |

| Footnotes and disclosures | Accounting policies, related parties, contingencies, leases, off-balance-sheet obligations | Reported numbers may depend on judgments or obligations not visible in headline metrics. | Disclosure complexity is not automatically a problem, but vague or changing explanations increase review risk. |

| MD&A and auditor context | Management explanations, risk language, auditor changes, internal-control comments | The quality of explanation can confirm or weaken confidence in reported trends. | Language must be read with the numbers; a clear explanation does not remove the need for cross-checking. |

Common Financial Statement Red Flags Investors Cross-Check

The strongest analysis treats each red flag as a condition with a possible implication, a required cross-check, and a limitation. That keeps the review analytical instead of turning it into a fraud checklist.

| Red flag | Where it appears | Possible implication | What to check | Limitation |

|---|---|---|---|---|

| Aggressive revenue recognition | Revenue, receivables, deferred revenue, footnotes | Reported sales may be pulled forward or depend on collection assumptions. | Compare revenue growth with receivables growth, cash collections, contract terms, and disclosure language. | Some business models naturally bill before or after delivery, so timing must match the model. |

| Profit rising while operating cash flow weakens | Income statement and cash flow statement | Earnings quality may be weaker than net income suggests. | Compare net income, operating cash flow, working capital changes, receivables, inventory, and deferred revenue. | Cash flow can be temporarily distorted by working-capital timing, taxes, or growth investment. |

| Receivables growing faster than revenue | Balance sheet and income statement | Customers may be taking longer to pay, terms may be loosening, or revenue quality may need review. | Compare days sales outstanding, customer terms, bad-debt allowances, concentration, and collection history. | Fast-growing companies can show receivables growth without manipulation if collection quality remains strong. |

| Inventory rising faster than sales | Balance sheet, cost of goods sold, margin trend | Demand may be slowing, inventory may be overvalued, or future margins may face pressure. | Compare inventory turnover, sales growth, gross margin, write-downs, and management’s demand explanation. | Inventory build can be normal before seasonal demand, product launches, or supply-chain normalization. |

| Margins deteriorating without a clear explanation | Income statement and MD&A | Pricing power, cost control, mix, or operating leverage may be weakening. | Compare gross margin, operating margin, input costs, price increases, product mix, and competitor behavior. | Temporary investment, launch costs, or cyclical input pressure can reduce margins without permanent damage. |

| Debt, interest burden, or liquidity pressure increasing | Balance sheet, cash flow statement, debt footnotes | The company may have less flexibility to fund operations, reinvest, refinance, or absorb shocks. | Compare debt maturity, interest coverage, free cash flow, covenant language, and liquidity sources. | Debt is not automatically negative if cash flow, maturity structure, and capital use remain sound. |

| Related-party transactions becoming more material | Footnotes, governance disclosures, balance sheet | Reported economics may be affected by relationships that are not fully arm’s length. | Review transaction size, pricing, recurrence, approval process, and disclosure clarity. | Related-party activity can be legitimate, but weak disclosure or unusual economics raises review risk. |

| Accounting policy changes or estimate changes | Footnotes, MD&A, income statement | Comparability may weaken, and reported trends may depend more on judgment. | Check what changed, why it changed, whether prior periods are restated, and how the change affects margins or earnings. | Some changes are required or reasonable; the issue is whether the effect is clearly explained. |

| Off-balance-sheet obligations or complex commitments | Footnotes, leases, guarantees, contingencies | Economic obligations may be larger than headline debt suggests. | Review lease commitments, guarantees, purchase obligations, litigation exposure, and contingent liabilities. | Materiality matters. Not every disclosed obligation changes the investment reading. |

How Investors Should Interpret a Red Flag

A useful red-flag review starts with a condition, not a conclusion. The condition is the observable change: receivables rising faster than revenue, cash flow lagging profit, debt becoming more expensive, margins moving without explanation, or disclosures becoming less comparable.

The next step is the implication. A receivables build may point to slower collections, looser terms, customer stress, or revenue timing. A cash-flow gap may point to working-capital pressure or earnings-quality risk. A margin decline may point to weaker pricing power, higher input costs, mix shift, or investment spending.

The final step is the limitation. Many red flags have normal explanations. Seasonality, acquisitions, billing cycles, growth investment, product launches, and accounting requirements can all create unusual statement patterns. The concern becomes stronger when the issue repeats, expands across statements, and is not explained clearly.

Illustrative Example: Profit Improves but Cash Conversion Weakens

A company reports higher revenue and higher net income. At first glance, the earnings trend looks stronger. The review changes if operating cash flow falls at the same time and receivables grow much faster than revenue.

That combination can mean customers are paying more slowly, the company is offering easier terms, or some revenue is being recognized before cash collection is strong. It can also reflect normal timing if the company has seasonal billing or a temporary working-capital build.

The stronger case appears when collections normalize, disclosure explains the timing, and cash flow later catches up. The weaker case appears when receivables keep rising, bad-debt allowances increase, customer payment behavior worsens, and management gives only broad explanations.

What Financial Statement Red Flags Do Not Prove

Financial statement red flags do not prove fraud by themselves. They also do not automatically mean a company is low quality, overvalued, or unsuitable for further research. A red flag is a diagnostic prompt: it tells the investor where the reported story needs more evidence.

They also do not work the same way in every sector. A software company, retailer, bank, manufacturer, and commodity producer can show different working-capital patterns, margin structures, cash-flow timing, and disclosure needs. The same ratio movement can carry different meaning depending on the business model.

The biggest mistake is treating a red flag as a shortcut. It should narrow the investigation, not replace it. The better test is whether several independent pieces of evidence point toward the same concern.

Related Business-Quality Checks

Financial statement red flags often connect to wider business-quality questions. If receivables rise because one buyer receives easier payment terms, customer concentration risk may become part of the review.

If debt increases, acquisitions accelerate, buybacks continue during weak cash generation, or reinvestment falls while margins are under pressure, capital allocation becomes relevant.

If the red flags challenge margin durability, pricing power, retention, or the company’s ability to recover from pressure, the durability of an economic moat may need to be tested again.

A Practical Cross-Statement Review Sequence

A disciplined review starts with the headline trend, then tests whether the supporting statements agree with it. If revenue and profit improve, operating cash flow should be checked next. If cash flow lags, working capital explains part of the gap. If working capital is the issue, receivables, inventory, customer terms, payment behavior, and disclosure language become more important.

If margins change, the review moves to pricing, cost structure, product mix, capitalization policies, and one-time items. If debt rises, the review moves to interest coverage, maturity schedule, refinancing exposure, covenant language, and cash generation. If disclosures change, the review moves to comparability and whether management gives enough detail to separate accounting from economics.

Financial Statement Red Flags FAQ

Are financial statement red flags proof of fraud?

No. Financial statement red flags are warning signs that require investigation. They can point to accounting risk, cash-flow weakness, disclosure problems, or business stress, but fraud requires stronger evidence than an unusual financial-statement pattern.

Which statement usually shows the first red flag?

There is no single statement that always shows the first red flag. Some concerns begin in the income statement through revenue or margin changes, while others appear first in the balance sheet through receivables, inventory, debt, or disclosure changes. The cash flow statement often helps test whether reported profit is turning into cash.

Can a strong company still have financial statement red flags?

Yes. Strong companies can show temporary red flags because of seasonality, growth investment, acquisitions, working-capital timing, or accounting changes. The concern becomes stronger when the issue repeats, expands across statements, and lacks a clear explanation.