IV crush can leave an option premium lower even when the underlying price moves in the expected direction. Option value depends on more than direction: implied volatility, time value, strike location, expiration, liquidity, and exercise or assignment conditions can all change after uncertainty resolves.

Definition: IV crush is a sharp drop in implied volatility after an expected event, such as an earnings announcement, regulatory decision, product update, or macro release. When event uncertainty disappears, the market may price less expected movement into the option, and that can reduce extrinsic value.

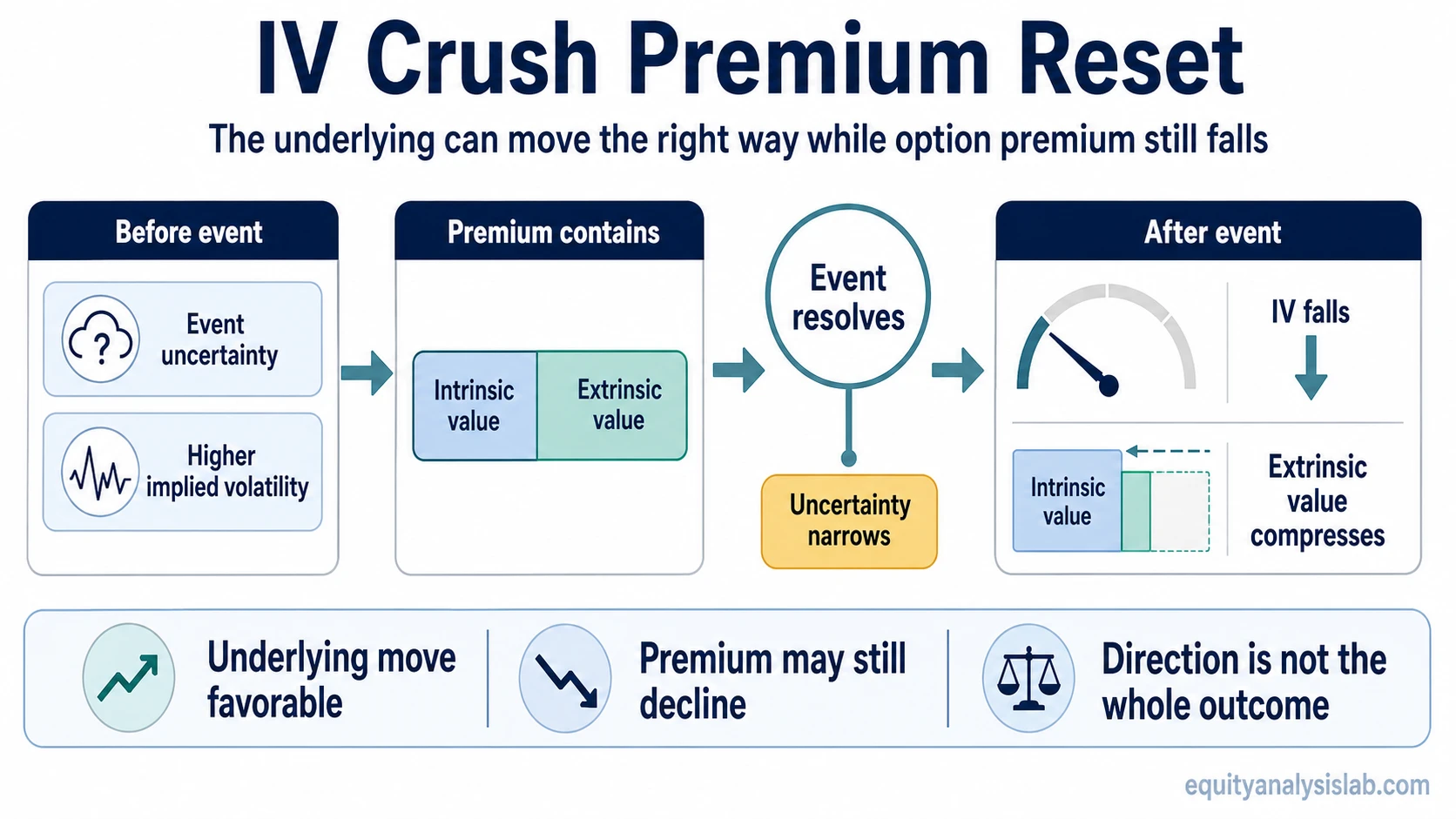

The effect is easiest to understand as a premium reset. Before the event, the option may carry extra volatility value because the market expects a larger possible move. After the event, that extra value can disappear quickly if the market no longer prices the same uncertainty into the contract.

Extrinsic value can fall faster than intrinsic value rises, which is why a directionally correct underlying move may still leave the option premium lower.

Key Points

- IV crush is about a decline in implied volatility, not only a move in the underlying price.

- An option premium can fall if extrinsic value drops faster than intrinsic value increases.

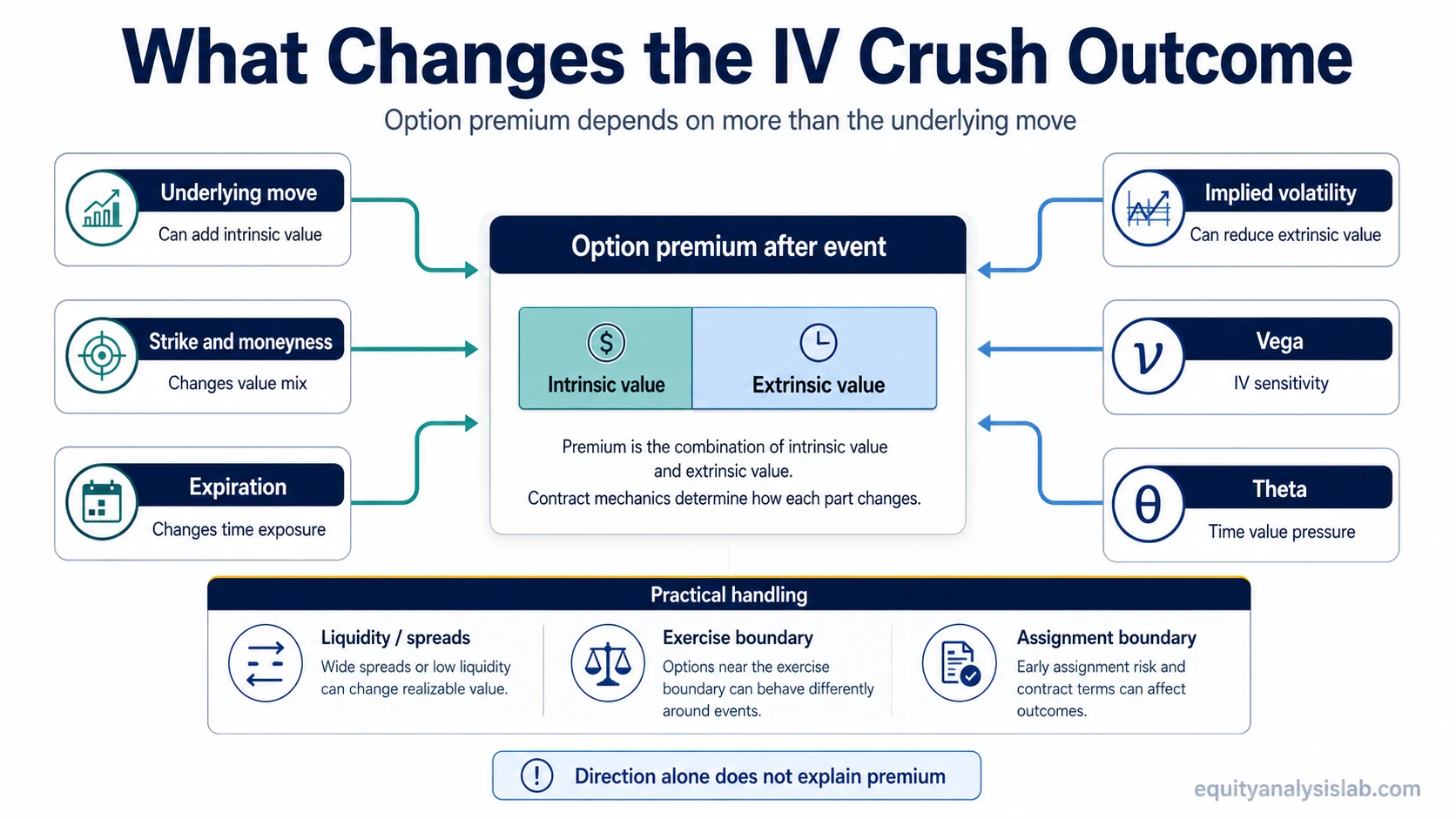

- Vega, theta, strike, expiration, moneyness, liquidity, and exercise or assignment conditions shape the result.

- Short premium exposure still carries obligation, liquidity, and large-underlying-move risk.

What IV crush means for option premium

Option premium is usually made of intrinsic value and extrinsic value. Intrinsic value reflects how far an option is in the money. Extrinsic value reflects the remaining time, expected movement, and market pricing of uncertainty.

IV crush mainly reduces the extrinsic part of the premium. A call or put can become directionally more favorable after an event, but the premium may still decline if the implied-volatility component falls enough. That is why implied volatility matters as a pricing input rather than a simple directional opinion.

Before a scheduled event, buyers may pay more for optionality because the range of possible outcomes is wider. Once the event is known, the market may no longer pay the same amount for uncertainty. The underlying move and the volatility reset are separate forces acting on the same contract.

The direction mistake

The common mistake is treating the underlying move as the whole option outcome. An options buyer may be directionally right after earnings, but a call option can still lose premium if the post-event volatility drop and time-value decay outweigh the benefit from the price move.

The same logic can affect puts after a downside move. Direction helps only if the contract gains enough intrinsic value, or retains enough extrinsic value, to offset the volatility reset and the remaining costs embedded in the premium.

Why direction can be right while premium falls

A pre-event option often contains a volatility charge for the unknown outcome. After the announcement, uncertainty narrows. The market may reduce the expected future move, which lowers the option’s extrinsic value.

Vega measures how sensitive the option premium is to changes in implied volatility. Higher-vega contracts can react more strongly when volatility drops. Theta adds another layer because time value can erode quickly around short-dated options, especially after the event that supported the premium has passed.

The Black-Scholes model helps organize the pricing inputs behind this behavior, but model value is not the same as realized market handling. Bid-ask spreads, contract liquidity, early exercise choices, and assignment exposure can change the practical result.

Contract mechanics that change the outcome

| Mechanic | How it affects IV crush | Limitation |

|---|---|---|

| Underlying move | A favorable move can add intrinsic value if the option moves deeper in the money. | The move may not be large enough to offset the implied-volatility decline. |

| Strike and moneyness | In-the-money, at-the-money, and out-of-the-money options react differently because their intrinsic and extrinsic value mix differs. | Out-of-the-money contracts can remain mostly extrinsic value and may be more exposed to volatility compression. |

| Expiration | Short-dated options can lose event premium quickly once the expected catalyst passes. | Longer-dated options may still hold value, but they can also have larger vega exposure. |

| Implied volatility | A sharp implied-volatility drop can reduce extrinsic value after uncertainty resolves. | A lower IV reading does not prove that a contract is cheap or safe. |

| Vega | Higher vega means the premium is more sensitive to changes in implied volatility. | Vega is not a standalone forecast; price movement, time, and liquidity still matter. |

| Theta and time value | Time value can fall quickly around event windows, especially in near-term contracts. | Theta is uneven because volatility, price movement, and expiration all change together. |

| Liquidity and bid-ask spread | Wide spreads can make the observed premium harder to translate into an executable value. | A theoretical premium may not match the price available in a thin contract. |

| Exercise and assignment boundary | Deep in-the-money or short option positions can introduce exercise or assignment considerations. | Premium collected or paid must be judged against the obligation or right created by the contract. |

A simple IV crush scenario

An earnings announcement is approaching, and short-dated call options carry elevated implied volatility. The market expects a large move, so the option premium includes a large amount of extrinsic value before the report.

The company reports, and the stock opens higher. The directional read was not wrong. The incomplete read was assuming that the call premium would rise simply because the stock moved up.

If the stock move is modest and implied volatility falls sharply after the announcement, the call may gain some intrinsic value while losing more extrinsic value. The premium can decline because the market no longer prices the same event uncertainty into the option.

Premium retention becomes more plausible when the underlying move is large enough to create meaningful intrinsic value, spreads remain tight, and volatility demand does not disappear completely. The opposite case appears when the move is small, the contract is still mostly extrinsic value, and the bid-ask spread widens while implied volatility resets lower.

Buyer and seller exposure after IV crush

Long option holders are exposed to paying for volatility that can disappear after the event. The premium paid before the announcement may include event uncertainty that is no longer present afterward.

Short option holders can benefit from volatility compression, but that does not remove the obligation created by the contract. A large underlying move, poor liquidity, early exercise conditions, or assignment risk can still dominate the premium collected.

The better distinction is not buyer versus seller. The better distinction is whether the premium change is being explained through direction alone or through the full contract mechanics.

What IV crush does not show

- IV crush does not forecast the next underlying move.

- IV crush does not prove that an option trade was high quality.

- IV crush does not guarantee a premium increase or decrease for every contract.

- IV crush does not remove assignment, exercise, liquidity, or spread risk.

- IV crush does not replace strike, expiration, moneyness, vega, and theta analysis.

How IV crush relates to pricing models and strike differences

Pricing models treat volatility as one input among several. When implied volatility falls, the model value can fall even if the underlying price moved in the expected direction. Model value, market premium, and realized contract handling need to be separated.

Strike selection also changes the exposure. At-the-money options usually carry more extrinsic value than deep in-the-money options, while far out-of-the-money contracts may rely heavily on volatility and remaining time. Across an option chain, the shape of implied volatility across strikes can make one contract react differently from another after the same event.

IV crush is not only an earnings label. It is a premium-compression mechanism that becomes most visible when event uncertainty, volatility exposure, strike location, and expiration timing collide.

FAQ

Can IV crush happen if the stock moves in the expected direction?

Yes. The option premium can still fall if implied volatility and time value decline more than the contract gains from the underlying move.

Is IV crush the same as time decay?

No. Time decay comes from the passage of time, while IV crush comes from a drop in implied volatility. Around events, both can affect the same option premium.

Does IV crush only affect option buyers?

No. Buyers may be hurt by falling volatility, but sellers still face underlying movement, liquidity, exercise, and assignment risk.

Is IV crush only an earnings issue?

No. Earnings are a common context, but IV crush can appear after any event where uncertainty was priced into options and then resolves.