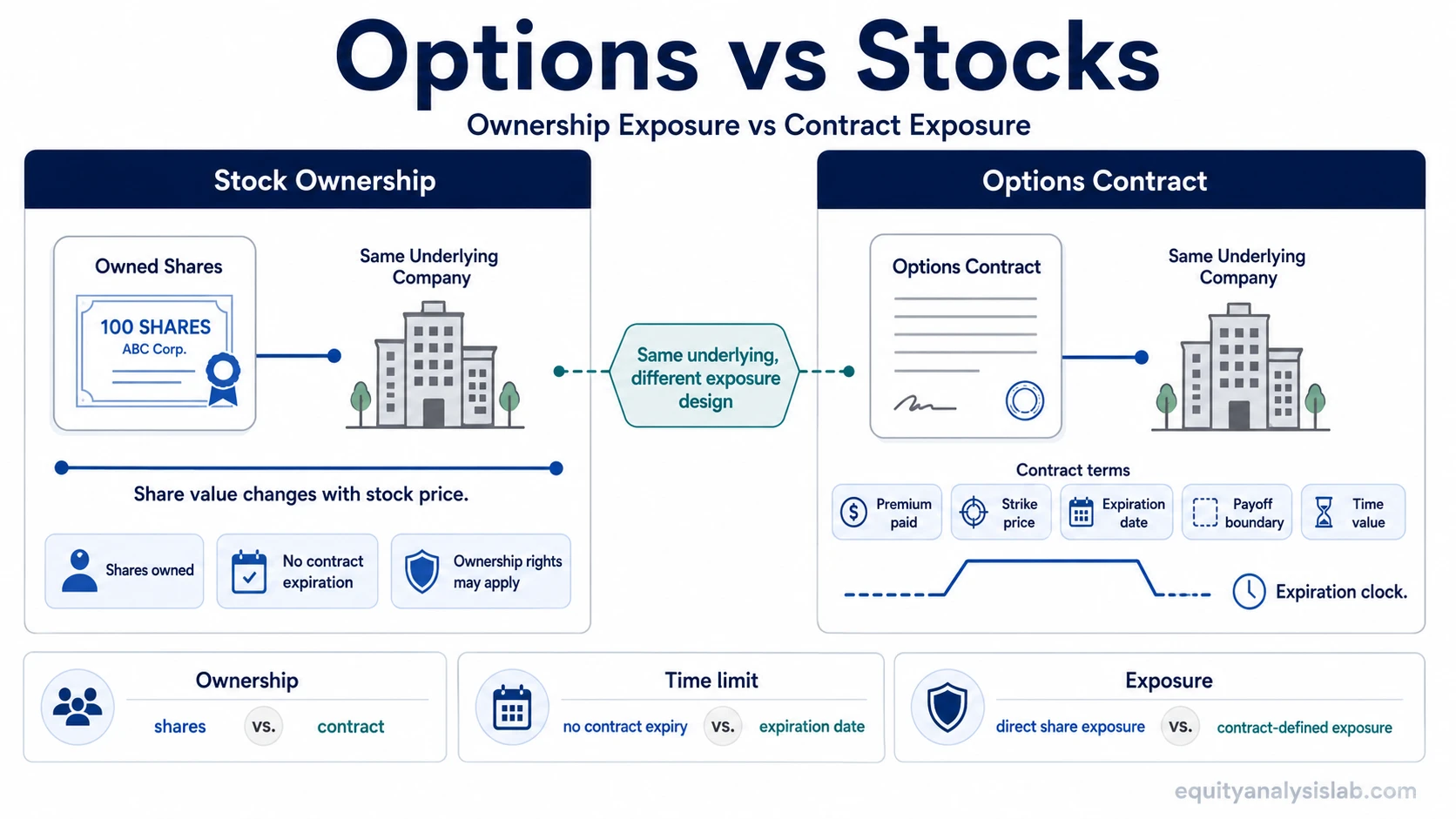

Stocks give ownership exposure. Options give contract-based exposure with defined terms, including a strike price, an option premium, an expiration date, and a payoff boundary.

The difference is not that one is always better than the other. The important distinction is how the exposure works. A stockholder owns shares of the company and participates directly in the value of those shares. An options position is a contract tied to an underlying stock or ETF, and its result depends on contract terms rather than ownership from the start.

That mechanical difference changes capital required, risk, time pressure, liquidity, rights, obligations, and how gains or losses can develop. The same market view can create very different exposure depending on whether it is expressed through shares or through an options contract.

Key Points

- Stocks represent direct ownership exposure, while options represent contract-based exposure.

- Stock ownership does not expire as an instrument, but every standard option contract has an expiration date.

- Options can create leverage, but leverage also adds timing pressure and contract-specific risk.

- Option buyers pay premium for rights; option sellers may take on obligations depending on the structure.

- A lower upfront option premium does not make an option economically identical to owning shares.

- The comparison should focus on exposure mechanics, not on declaring one instrument universally better.

Options vs Stocks: Main Difference

The main difference between options and stocks is ownership. Stocks are shares of a company. Options are contracts that give rights or create obligations tied to an underlying security.

Core distinction: Stock ownership gives direct share exposure. Options exposure is defined by contract terms such as premium, strike price, expiration, and exercise or assignment mechanics.

Stockholders may have ownership-related rights such as voting rights, dividend eligibility when declared, and the ability to hold shares without a built-in expiration date. Option buyers do not become stockholders simply because they buy a call or put. They hold a contract whose value depends on the underlying price, time remaining, volatility, strike selection, and market liquidity.

This is why options can look less expensive upfront while still carrying a different type of risk. Paying a smaller premium for a contract is not the same as purchasing the underlying shares. It changes the exposure from ownership to a time-limited contract claim.

Options vs Stocks Comparison Table

| Comparison Point | Stocks | Options |

|---|---|---|

| Basic structure | Shares represent ownership in a company. | Contracts are tied to an underlying stock or ETF. |

| Ownership rights | Stockholders may have voting rights and dividend eligibility when applicable. | Option holders do not receive ownership rights by default. |

| Capital required | The investor usually pays the share price multiplied by the number of shares. | The buyer pays premium; the seller may need margin or collateral depending on the contract. |

| Expiration | Shares do not expire as instruments. | Options have defined expiration dates. |

| Time decay | There is no contract time decay built into share ownership. | Time decay can reduce option value as expiration approaches, especially for long options. |

| Leverage | Exposure usually changes directly with the number of shares owned. | A smaller premium can control larger notional exposure, but the contract may expire with limited or no value. |

| Payoff boundary | Share value rises or falls with the stock price. | Payoff depends on strike price, premium paid or received, expiration, and contract type. |

| Liquidity and spreads | Large stocks often have visible share liquidity, though liquidity can still vary. | Options liquidity can vary by strike, expiration, volume, open interest, and bid-ask spread. |

| Exercise and assignment | There is no option exercise or assignment process in ordinary share ownership. | Exercise and assignment are contract mechanics that can create or remove stock exposure under specific terms. |

| Common misunderstanding | Assuming shares are simple ignores business, valuation, or market risk. | Assuming lower premium makes the contract a simple substitute for shares. |

How Stock Ownership Works

Buying stock means buying shares of a company. The investor participates directly in share-price changes and may receive ownership-related rights depending on the share class, the company, and market rules.

In equity investing, stock ownership is usually interpreted through business quality, valuation, earnings durability, cash flow, capital allocation, and portfolio role. The instrument itself is simple compared with an option contract, but the investment risk is still real because the company’s value and market price can change.

Stocks do not have a built-in expiration date. A shareholder can continue holding the shares unless the position is sold, the company is acquired, the security is delisted, or another corporate event changes the structure. That does not make the position risk-free. It means the instrument is not forced to resolve by a specific contract expiration date.

Ownership boundary: A shareholder owns shares. That ownership exposure is different from using a contract that may or may not become stock exposure later.

How Options Exposure Works

An option is a contract tied to an underlying security. A call option is linked to the right to buy under defined terms, while a put option is linked to the right to sell under defined terms. The exact exposure depends on the option type, strike price, expiration date, premium, and whether the investor is buying or selling the contract.

The option premium is the price paid by the buyer and received by the seller. For the buyer, premium is the upfront cost of the contract. For the seller, premium is compensation for taking on the contract obligation, subject to the structure and collateral or margin requirements.

Options can create leverage because a contract may provide exposure to the underlying security for less upfront capital than buying shares outright. That leverage is not automatically an advantage. The contract has a time limit, and the underlying price must interact with the strike and premium in a way that makes the position economically useful before or at expiration.

At expiration, payoff and breakeven are contract-specific. They depend on the option type, strike price, premium paid or received, and the underlying price, rather than simply matching the stock’s gain or loss.

Time decay is one of the main differences. A stockholder does not face an expiration clock inside the share itself. A long option holder does. As expiration approaches, the time value embedded in the option can decline, even when the underlying thesis has not fully changed.

Contract boundary: Options can express a market view, hedge a position, or define a payoff shape, but they are not automatic replacements for owning stock. The contract terms decide the exposure.

Why Lower Option Premium Is Not the Same as Owning Stock

A common mistake is treating a lower option premium as if it were simply a cheaper version of the stock. The upfront cost may be lower, but the investor is buying a different instrument with different mechanics.

For example, buying shares gives direct exposure to the share price. Buying a call option gives contract exposure that depends on the strike price, premium paid, expiration date, volatility, and market liquidity. If the stock price moves, the option may not move in a simple one-for-one way, especially when expiration, implied volatility, and moneyness are changing at the same time.

The same issue applies to risk. A stock can decline substantially, but the investor still owns the shares unless the position is sold or the company’s equity value is impaired. A long option can lose most or all of its premium if the contract expires without sufficient value. Those are different risk shapes, not just different prices.

Common mistake: Lower upfront cost does not mean lower total risk. It can mean a narrower, time-limited, contract-defined exposure where timing and payoff boundaries matter more.

Same Company, Different Exposure Example

Consider two investors who both have a constructive view on the same company, without assuming any specific outcome.

Investor A: Buys shares and receives direct ownership exposure. The position changes with the stock price, and the investor may continue holding without a contract expiration date.

Investor B: Buys an option contract tied to the same stock. The position is defined by premium paid, strike price, expiration date, and the payoff boundary of the contract.

Both investors are connected to the same underlying company, but the exposures are not identical. Investor A owns shares. Investor B owns a contract. If the company thesis develops slowly, stock ownership and option exposure may behave very differently because the option has an expiration date and time value component.

The same distinction applies when options are used around existing stock exposure. A cash-secured put structure is built around reserved cash and a potential purchase obligation, not current share ownership.

A hedged stock structure such as a collar starts from owned shares and adds option contracts that can reshape upside and downside boundaries.

The useful comparison is therefore not “stock or option equals the same thesis.” It is “same underlying, different exposure design.”

When the Comparison Can Mislead Investors

The options vs stocks comparison becomes misleading when it is reduced to cost alone. A contract that costs less upfront may still be more sensitive to time, volatility, liquidity, and strike selection than a stock position.

It can also be misleading to compare maximum loss without comparing probability, holding period, and exposure continuity. A long option buyer may have a defined premium at risk, but the contract can expire before the underlying thesis has enough time to develop. A stockholder may have no expiration date, but the position can still suffer large losses if the business or valuation deteriorates.

Option selling adds another boundary. The seller receives premium, but that premium comes with obligations. Depending on the contract, assignment can create or remove stock exposure under specific terms. That is not the same as starting with ordinary stock ownership.

Investor-use boundary: Options and stocks should be compared by mechanics, rights, obligations, time limits, and payoff structure. Treating either instrument as universally better removes the context that makes the comparison useful.

Related Concepts

Several related concepts help separate ownership exposure from contract exposure without turning the comparison into strategy selection.

| Concept | Why It Matters |

|---|---|

| Equity investing | Explains stock ownership as part of company analysis, valuation, and portfolio construction. |

| Option premium | Shows how contract cost affects payoff boundaries, risk, and breakeven interpretation. |

| Cash-secured put | Illustrates that an option structure can involve reserved cash and a potential assignment obligation rather than current ownership. |

| Collar | Shows how options can be added around owned shares to reshape payoff boundaries. |

The broader lesson is that stock ownership and options exposure can reference the same underlying security while creating different economic positions. The contract terms, not only the market view, determine the exposure.

FAQ

Are options the same as stocks?

No. Stocks are shares of ownership in a company. Options are contracts tied to an underlying stock or ETF, with defined terms such as strike price, premium, and expiration.

Are options riskier than stocks?

Options have different risks rather than one universal risk ranking. They can involve leverage, expiration, time decay, liquidity differences, and assignment or exercise mechanics. Stocks have direct ownership risk and can still lose substantial value.

Why can options cost less than buying stock?

An option premium buys contract exposure, not ownership of the underlying shares. The lower upfront cost reflects a different instrument with defined terms, time limits, and payoff boundaries.

Do option buyers own the stock?

Not by default. An option buyer owns a contract. A buyer may create stock exposure through exercise under the relevant terms, while assignment applies to option sellers rather than buyers.