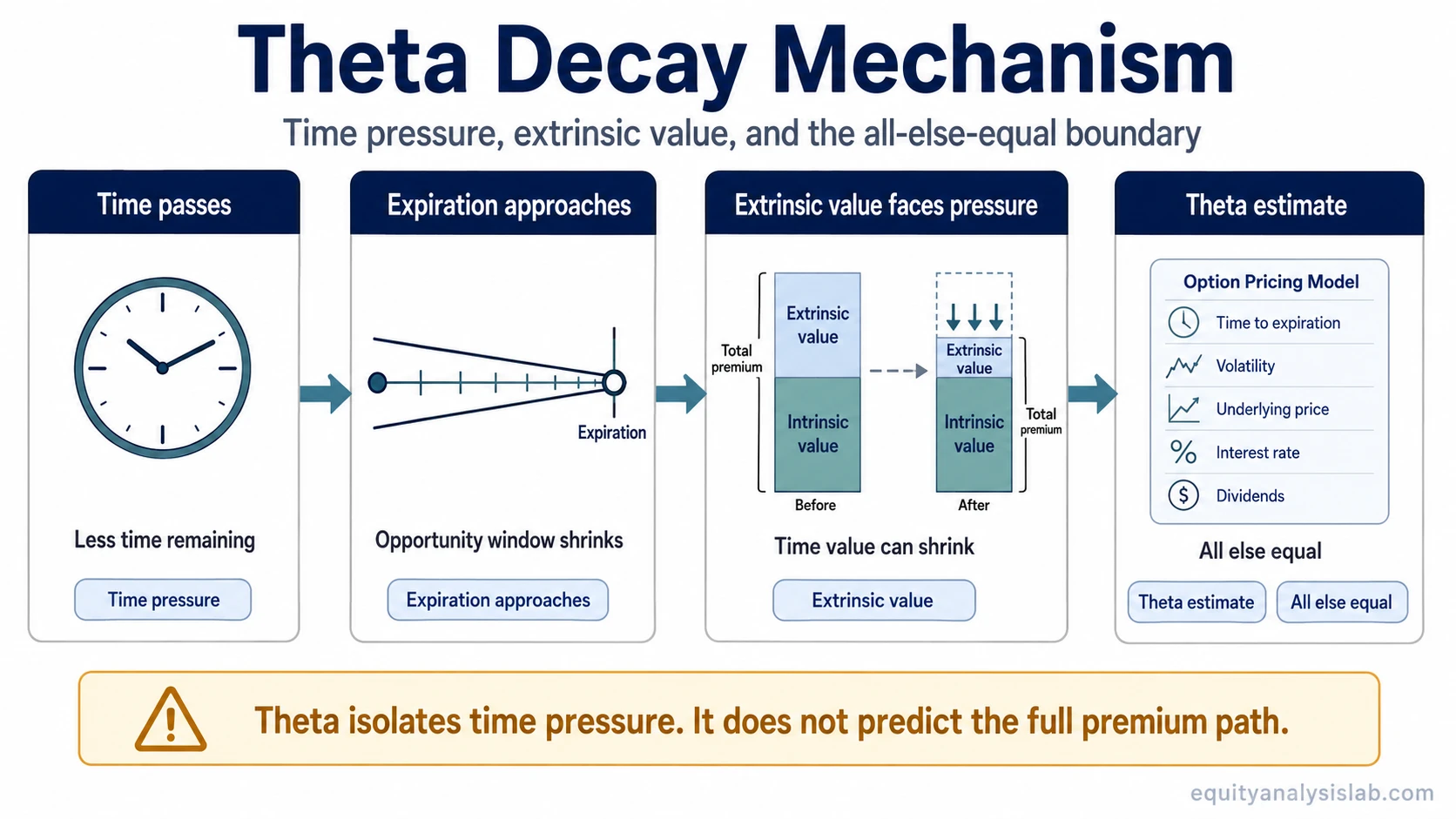

Theta decay describes the time-related pressure on an option’s theoretical value as expiration approaches. The pressure is mainly tied to extrinsic value, and it is measured all else equal, which means the actual option premium can still move differently when price, volatility, liquidity, or moneyness changes at the same time.

Definition: Theta decay is the loss of theoretical option value associated with the passage of time, mainly through the shrinking of time value inside the option’s extrinsic value. It is not a guaranteed daily dollar amount, and it is not a complete forecast of the option’s market premium.

The useful starting point is to separate the clock from the whole option price. Theta estimates the time component of theoretical value. Time decay describes the pressure created as time remaining gets shorter. The market premium before expiration can also change because the underlying moves, implied volatility changes, or the quoted bid and ask no longer match the model value closely.

Key Points

- Theta decay is about time pressure on theoretical option value, not a fixed daily cash flow.

- The effect mainly applies to extrinsic value, because intrinsic value depends on the relationship between the strike and the underlying price.

- Theta is an all-else-equal estimate, so it works best as one input rather than a full premium forecast.

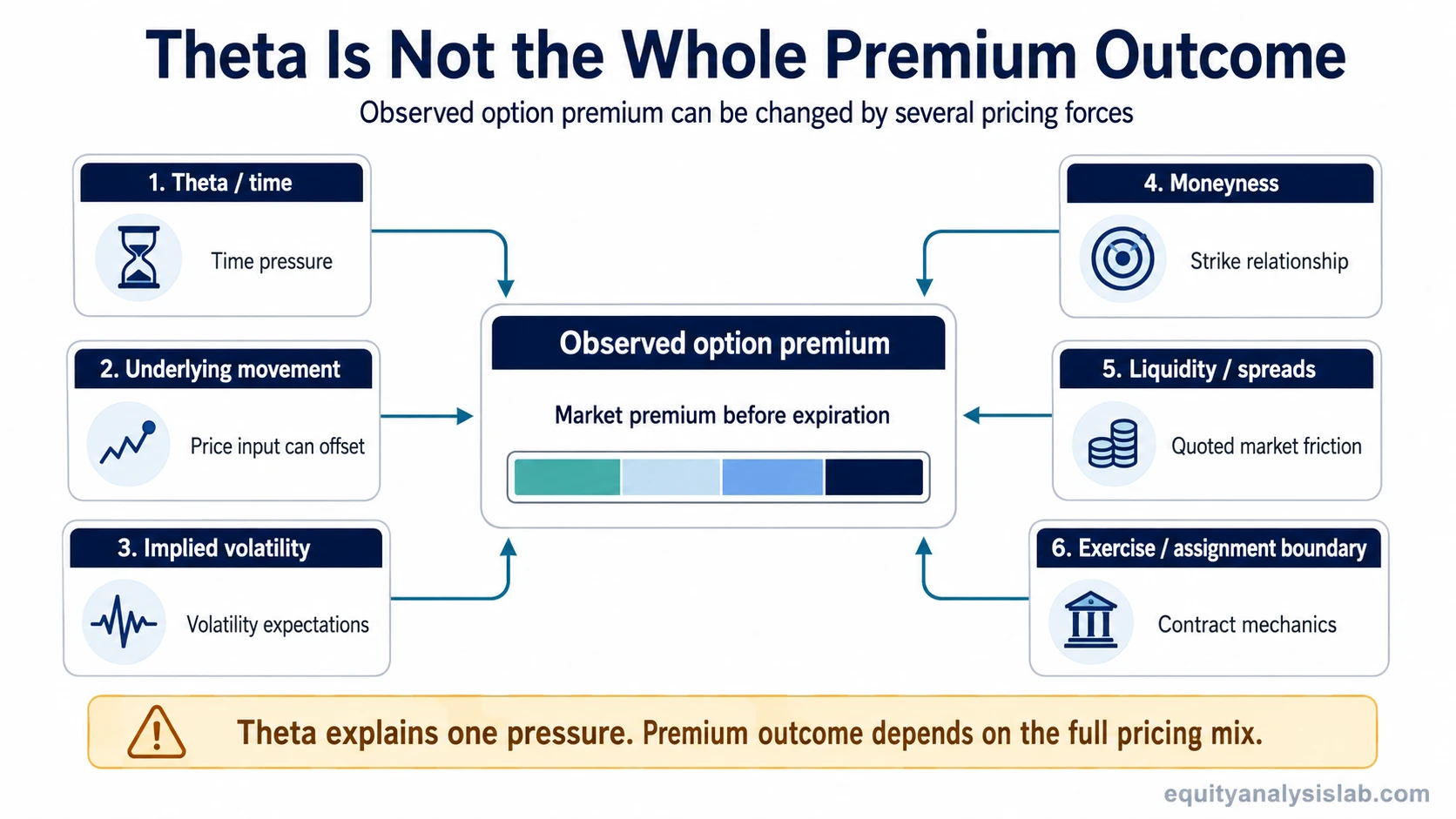

- Underlying movement, implied volatility, moneyness, liquidity, and expiration can change the observed option premium.

- A directionally reasonable view can still be poorly matched to an option if the move is too slow for the expiration and time decay burden.

What Theta Decay Means in Options

Theta is the option Greek connected to time. It estimates how much the theoretical value of an option may change as one day passes, assuming the other pricing inputs stay stable. That “assuming” is the boundary that beginners often miss.

For many long options, theta is usually negative because time passing removes some of the remaining opportunity for the option to become more valuable. For many short options, theta may appear positive because the seller can benefit from time value shrinking. That does not make short theta free income. The seller accepts other risks, including underlying price movement, volatility changes, assignment exposure, and liquidity conditions.

Clean mental model: theta is the clock input, not the whole option outcome. It helps explain time pressure, but it does not decide whether the market premium rises, falls, or stays stable before expiration.

What Part of Option Premium Decays

An option premium can be thought of as a combination of intrinsic value and extrinsic value. Intrinsic value reflects how far the option is already in the money. Extrinsic value reflects the remaining time, uncertainty, volatility expectation, and other pricing assumptions above intrinsic value.

Theta decay mainly pressures extrinsic value. As the expiration clock runs down, there is less time for the underlying to move favorably, so the time-value portion of the option tends to compress if other inputs do not offset it.

| Concept | Role in theta decay | Boundary |

|---|---|---|

| Theta | Measures time-related sensitivity in theoretical value. | It excludes other forces that can move the traded premium. |

| Time decay | Describes the pressure from shrinking time remaining. | The amount does not disappear in the same way every day. |

| Extrinsic value | The part of premium most directly pressured by time decay. | Can also change when volatility expectations or demand for the option changes. |

| Expiration | Creates the boundary where time value eventually disappears. | Does not describe every premium change before expiration. |

| Premium path | The observed market price of the option before expiration. | Can be affected by underlying price, volatility, spreads, and moneyness. |

Why Expiration Changes Theta Decay

The closer an option gets to its expiration date, the less time remains for uncertainty to be priced into the contract. This is why theta decay often becomes more noticeable near expiration, especially for options near the money.

Moneyness matters because an option that is far out of the money, near the money, or deep in the money does not carry the same mix of intrinsic value and extrinsic value. Near-the-money options often have more time value to lose, while deep in-the-money options may have a larger share of value tied to intrinsic value.

Expiration boundary: by expiration, an option’s value is determined by its payoff mechanics. Before expiration, the premium can still reflect time, volatility expectations, liquidity, and changes in the underlying price.

Theta Decay Does Not Equal Final Premium Outcome

Theta is useful because it isolates one pricing pressure. It becomes misleading when it is treated as the whole premium outcome. The observed premium can rise even when theta is negative, or fall less than expected, if another force offsets the time decay estimate.

| Question | What theta helps with | What theta does not fully answer | Better route |

|---|---|---|---|

| How does time affect the option? | It estimates the time-related pressure on theoretical value. | It does not isolate volatility changes or underlying price movement. | Read theta and time decay together. |

| What part of premium can shrink? | It points mainly toward pressure on extrinsic value. | It does not explain changes in intrinsic value when the underlying moves. | Separate option premium into intrinsic and extrinsic value. |

| Why did the option premium rise even with negative theta? | It shows that time was a headwind. | An underlying move, volatility increase, or change in demand may have outweighed that headwind. | Check implied volatility, delta, and gamma together. |

| What happens at expiration? | It helps explain why time value disappears as the contract reaches its endpoint. | It does not describe every premium path before the contract reaches expiration. | Use expiration date, exercise, and assignment concepts for the boundary. |

| Why is the bid or ask different from theoretical value? | It gives a model sensitivity, not an executable quote. | Bid-ask spreads and options liquidity can affect the price a trader or investor can actually transact at. | Separate theoretical value from market quote quality. |

A Short Example of Being Directionally Right but Time-Wrong

Consider a call option with negative theta. The underlying stock may move in the expected direction, but if the move is slow and implied volatility falls at the same time, the option premium may not rise as much as the directional view suggested. In another case, a sharp underlying move or a rise in implied volatility may offset the time decay pressure.

The lesson is not that theta is unimportant. The lesson is that theta is one layer in the premium path. The option’s market price before expiration reflects timing, volatility, moneyness, liquidity, and the underlying move together.

Beginner Mistakes With Theta Decay

Mistake 1: Treating theta as guaranteed daily cash flow. Theta is a model estimate. It can change as the option moves across strikes, time passes, or volatility changes.

Mistake 2: Assuming theta is the only reason premium changes. Premium can also respond to the underlying price, implied volatility, liquidity, and moneyness.

Mistake 3: Confusing theoretical value with executable market premium. A model value and a live bid-ask quote are not the same thing.

Mistake 4: Reading short theta as free income. Positive theta exposure still carries risk from price movement, volatility changes, margin or collateral needs, and exercise or assignment boundaries.

Mistake 5: Ignoring implied volatility and underlying movement. A volatility increase or strong price move can offset theta pressure, while a volatility drop can make a directionally correct option position weaker than expected.

Mistake 6: Treating expiration payoff as the whole story. Expiration payoff is the endpoint. The premium path before that endpoint can behave differently.

Which Concept to Read Next

The broad phrase “theta decay” usually hides several different questions. The next concept depends on the question behind it.

| If the question is… | Read next | Why it helps |

|---|---|---|

| What does the theta number mean? | theta | It focuses on the Greek itself and how the time-sensitivity estimate is read. |

| Why does time pressure increase as expiration approaches? | time decay | It explains the time-value compression mechanism in more detail. |

| Which part of the option price is affected? | option premium | It separates the total premium into the pieces that can change for different reasons. |

| What is the time-value part of premium? | extrinsic value | It explains the portion most directly pressured by the passage of time. |

| Why does the endpoint matter? | expiration date | It explains the boundary where remaining time value reaches its endpoint. |

| Why can volatility offset time decay? | implied volatility | It explains why changing volatility expectations can raise or lower premium apart from time passing. |

| Why can the underlying move change the option faster than expected? | delta and gamma | Delta describes current underlying sensitivity, while gamma describes how that sensitivity can change. |

| Why can exercise or assignment matter near expiration? | exercise and assignment | These concepts explain contract handling boundaries that are not captured by theta alone. |

FAQ

Is theta decay the same as time decay?

Theta is the Greek that estimates time-related sensitivity, while time decay is the broader idea that an option’s time value can shrink as expiration approaches. They are closely related, but theta is the measurement and time decay is the pressure being described.

Does theta decay mean an option loses money every day?

No. Theta decay does not guarantee a fixed daily premium loss. Other inputs can change at the same time, including the underlying price, implied volatility, moneyness, and market liquidity.

Can an option rise even when theta is negative?

Yes. A negative theta reading means time passing is a headwind all else equal. The option premium can still rise if another force, such as a favorable underlying move or higher implied volatility, outweighs that headwind.

Why does theta often change near expiration?

Theta often changes near expiration because less time remains for uncertainty to be priced into the option. The effect can be especially noticeable for options near the money, where extrinsic value can still be meaningful.