A currency-hedged ETF uses a hedge overlay to reduce selected foreign-exchange exposure, often through forward contracts or an index-level hedge process. The fund still holds or tracks underlying securities. The hedge changes the currency layer of the investment; it does not automatically make the ETF lower-risk, higher-quality, lower-cost, or more suitable.

The common mistake is treating the currency-hedged label as the whole exposure picture. A hedged ETF can still have equity, bond, sector, country, liquidity, tracking, distribution, and tax characteristics that matter separately from the currency overlay.

Working definition: a currency-hedged ETF is an ETF that adds a currency hedge to reduce the effect of exchange-rate movements between the fund’s reference currency and the currencies linked to its holdings or index exposure.

What a Currency-Hedged ETF Means

A currency-hedged ETF combines two layers. The first layer is the ETF’s underlying exposure, such as stocks, bonds, or another index basket. The second layer is the hedge process, which is designed to offset part of the foreign-currency movement that would otherwise affect returns for a selected reference currency.

The hedge is usually not a separate promise about fund quality. It is a structural feature. A fund may track similar holdings to an unhedged version while using contracts or index rules to reduce currency movement against a chosen currency base.

The reference currency matters. A hedge built around U.S. dollars, euros, pounds, or another currency may not match every investor’s actual base currency. An investor whose spending, liabilities, or portfolio reporting are in a different currency may experience the hedge differently from the fund’s reference design.

How the Currency Hedge Changes Exposure

Foreign-exchange exposure appears when the assets inside the ETF are linked to currencies different from the investor’s base currency or the fund’s reference currency. If those currencies move, the ETF’s return can differ from the return of the underlying securities in their local markets.

A hedge overlay attempts to reduce that currency effect. In plain terms, the fund or the index methodology may use rolling currency forwards or similar instruments so that gains or losses from currency movement are partly offset by the hedge position.

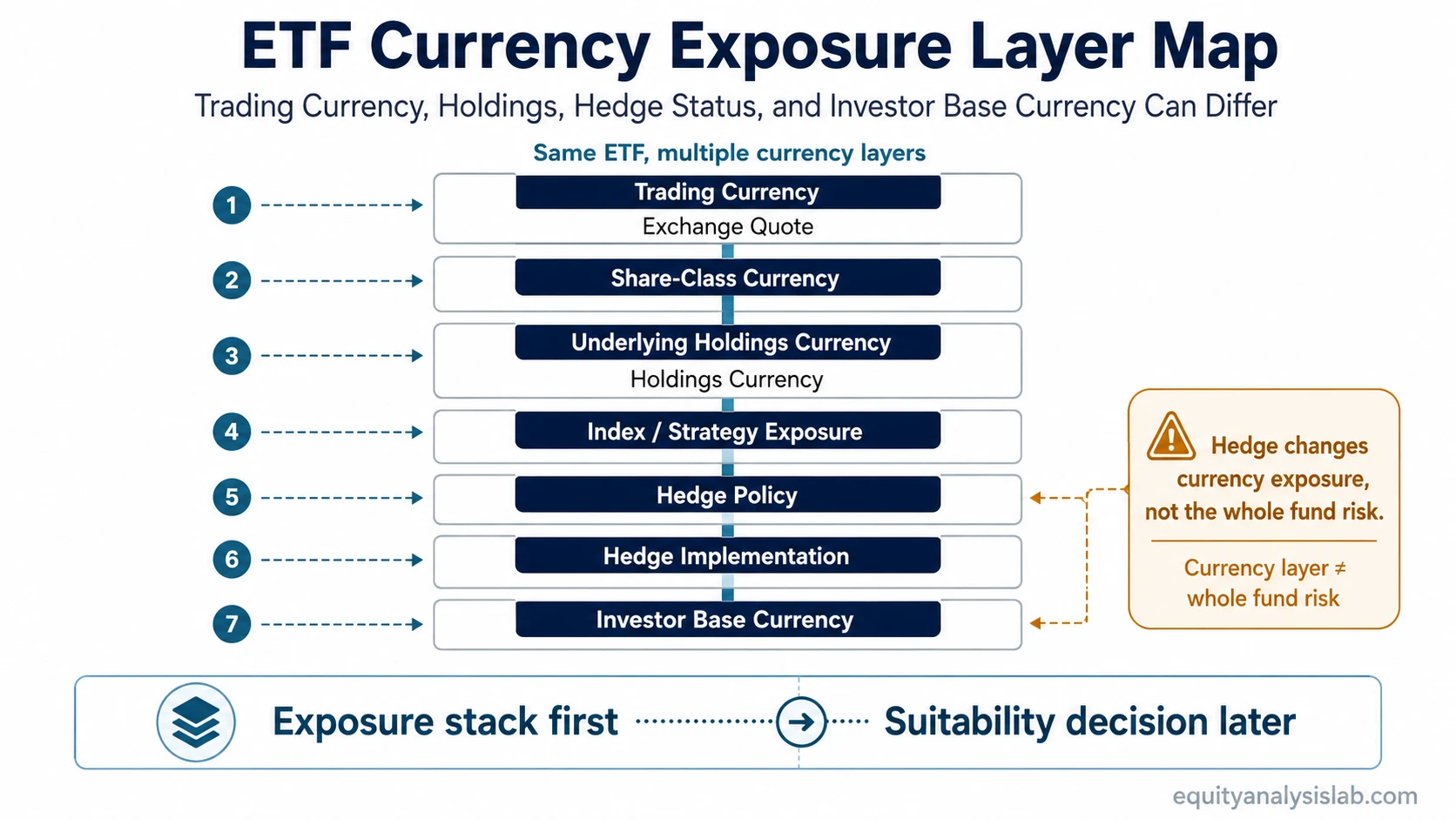

The hedge can be fund-level, share-class-level, index-level, partial, or rules-based. That distinction matters because the ETF’s trading currency, the share class currency, the holdings currency, and the hedge currency are not always the same thing.

Exposure stack: trading currency, share-class currency, holdings currency, index or strategy exposure, hedge policy, hedge implementation, and investor base currency can all differ. The fund label is only one layer.

This is especially relevant when investors compare funds with international holdings, because the stock or bond exposure and the currency exposure may not point to the same practical conclusion.

Hedged vs Unhedged ETF Exposure

A hedged ETF and an unhedged ETF can hold or track similar underlying assets while producing different investor-level return paths because the currency layer is handled differently. The distinction is not that one is automatically better. The distinction is how much currency movement remains visible to the investor.

| Comparison point | Currency-hedged ETF | Unhedged ETF | Investor interpretation |

|---|---|---|---|

| Foreign currency movement | Designed to reduce selected currency effects against a reference currency. | Leaves more of the foreign-currency movement in the return path. | The investor should identify which currency exposure is being reduced and which remains. |

| Hedge overlay | Uses a currency hedge process, often with forwards or an index-level hedge rule. | Usually does not add a currency hedge overlay for the same exposure. | The hedge is an implementation choice, not a quality label. |

| Upside and downside currency effect | May reduce negative currency effects but can also reduce positive currency contributions. | Can benefit or suffer more directly from currency movement. | Currency hedging changes both sides of the currency contribution. |

| Costs | May include higher expense ratios, hedge costs, transaction effects, carry effects, or roll costs. | May avoid explicit hedge implementation costs but still has normal fund costs. | Total cost should be compared beyond the headline expense ratio. |

| Tracking error and tracking difference | Can differ from the benchmark because of hedge timing, cost, contract rolling, and implementation. | Can differ from the benchmark because of fees, sampling, trading, taxes, cash drag, and other fund mechanics. | Both versions can have tracking error and tracking difference; the sources may differ. |

| Suitability / quality interpretation | Not automatically safer, better, or more suitable. | Not automatically riskier, worse, or less suitable. | The decision depends on exposure, costs, base currency, time horizon, liquidity, and investor objectives. |

What to Check Before Comparing Currency-Hedged ETFs

Currency hedging should be compared as part of the ETF structure, not as a standalone label. The same headline exposure can behave differently if the hedge policy, share class, cost structure, and underlying holdings differ.

| Check | Why it matters | What can go wrong |

|---|---|---|

| Underlying holdings | The fund’s securities still drive the main asset exposure. | The hedge can distract from sector, country, duration, credit, or concentration risk. |

| Trading or share-class currency | The exchange quote currency may not equal the holdings currency or the hedge reference currency. | An investor may assume the trading currency defines the real currency exposure. |

| Index or strategy exposure | The fund may follow an index methodology that defines how hedging is applied. | Two funds with similar names may hedge differently. |

| Hedge currency | The hedge is usually designed around a specific reference currency. | The hedge may not align with the investor’s own base currency. |

| Hedge policy and rebalance method | Currency forwards and hedge ratios may be reset on a schedule or according to index rules. | The hedge may be imperfect between rebalance points. |

| Expense ratio and hedge cost | The visible expense ratio may not capture every currency-hedging effect. | Roll costs, transaction effects, and interest-rate differentials can affect results. |

| Liquidity and spreads | ETF market price execution can differ from fund value, especially in less liquid share classes. | The hedge may be evaluated while ignoring trading cost and bid-ask spread. |

| Distributions | Currency gains and fund distributions can affect the amount and timing of cash received by the investor. | A generic hedge explanation may not match the fund’s actual distribution mechanics. |

| Tax mechanics | Withholding tax, local tax treatment, and account type can affect the investor’s realized experience. | The hedge may be interpreted without checking jurisdiction-specific tax treatment. |

Currency exposure can also matter beyond equity funds. For example, a global or foreign-currency bond ETF structure may have interest-rate, credit, duration, and currency layers that need to be separated before the hedge is interpreted.

Where Currency Hedging Can Mislead Investors

The label can mislead when it sounds like a complete risk answer. A currency hedge may reduce one selected foreign-exchange exposure while leaving the underlying asset risk intact. It can also reduce currency upside that would have helped an unhedged version.

A second mistake is treating the ETF’s trading currency as the same thing as its economic currency exposure. A fund may trade in one currency, hold securities exposed to several currencies, and hedge to a different reference currency.

A third mistake is ignoring implementation. Hedge frequency, forward pricing, transaction costs, carry effects, tax treatment, and distributions can all affect the investor’s realized experience. These details do not make hedging good or bad by themselves, but they can explain why the result differs from a simple currency assumption.

Limitation: a currency hedge is a structural exposure choice, not a recommendation. It does not guarantee lower risk, better returns, better tracking, or better fund quality. The result depends on the investor’s base currency, the ETF’s holdings, hedge method, costs, liquidity, distributions, tax treatment, and the currency path over the holding period.

A Simple ETF Selection Scenario

Consider an investor comparing two international equity ETFs that track similar overseas stocks. One share class is currency-hedged to the investor’s reference currency, while the other is unhedged. If the foreign currency weakens, the hedged version may reduce part of that drag. If the foreign currency strengthens, the unhedged version may receive more of that currency benefit.

The diagnostic question is not “which version is better?” but “which currency layer is being accepted, reduced, or left exposed?” That forces the comparison back to holdings, index methodology, expense ratio, bid-ask spread, hedge policy, expected tracking behavior, distribution treatment, and tax treatment. The hedge changes the currency layer, but it does not replace the full ETF selection process.

FAQ

What is a currency-hedged ETF?

A currency-hedged ETF is an ETF that adds a hedge overlay designed to reduce selected foreign-exchange exposure. It still holds or tracks underlying securities, so the hedge changes the currency layer rather than removing the fund’s other risks.

Does currency hedging make an ETF safer?

No. Currency hedging can reduce selected currency movements, but it does not guarantee lower risk, better returns, or better fund quality. The underlying holdings, costs, liquidity, tracking behavior, and investor base currency still matter.

What is the difference between a hedged and unhedged ETF?

A hedged ETF tries to reduce selected currency effects through a hedge process. An unhedged ETF leaves more of the currency movement in the return path. Neither structure is automatically better; they expose the investor to different currency outcomes.

Does the ETF trading currency show the real currency exposure?

Not necessarily. The trading currency is only the currency in which the ETF shares are quoted on an exchange. The holdings currency, index exposure, hedge reference currency, and investor base currency can all differ.