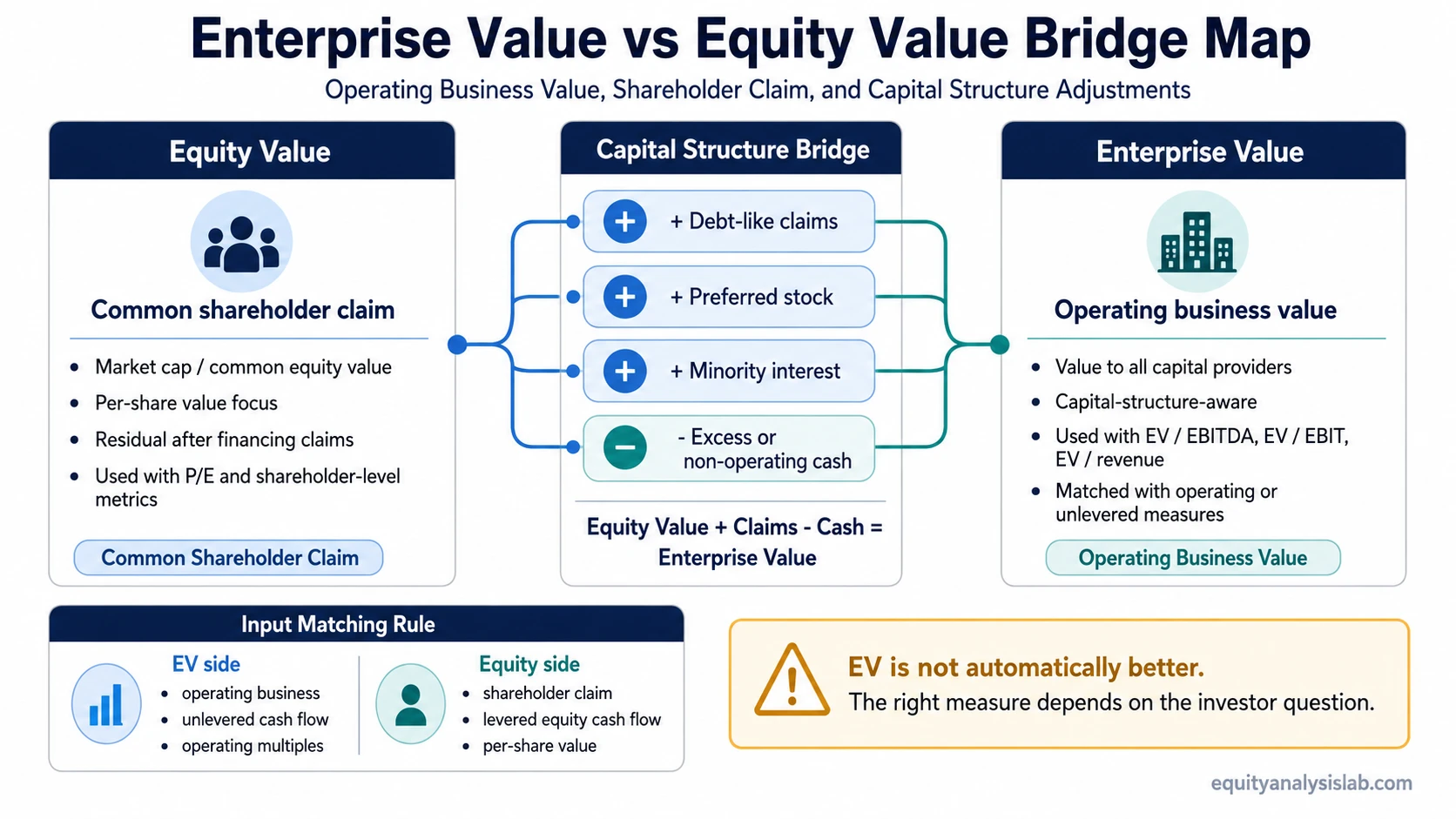

Enterprise value and equity value can use the same company data, but they answer different investor questions. Enterprise value focuses on the value of the operating business available to all capital providers. Equity value focuses on the residual claim left for common shareholders after financing claims are considered.

The practical difference is input matching. Enterprise value fits questions about the whole operating business, unlevered cash flow, and EV-based valuation multiples. Equity value fits questions about common equity ownership, per-share value, levered equity cash flow, and the shareholder claim after debt, cash, and other claims are bridged.

Key Points

- Enterprise value measures the operating business across debt and equity financing, while equity value measures the shareholder-level claim.

- The bridge usually starts with common equity value, then adds debt-like claims and subtracts cash treated as excess or non-operating when estimating enterprise value.

- EV-based multiples should usually be matched with operating metrics, while equity-value measures should usually be matched with shareholder-level metrics.

- The comparison becomes unreliable when debt, cash, preferred stock, minority interest, diluted shares, or per-share assumptions are handled inconsistently.

Enterprise Value vs Equity Value at a Glance

Enterprise value asks what the operating business is worth before separating claims between lenders and shareholders. It is often used when comparing companies with different debt and cash balances because it moves the analysis closer to the business itself rather than only the equity slice.

Equity value asks what value remains for shareholders. Public market capitalization is often used as a starting point for common equity value, but per-share analysis can require diluted shares, option effects, preferred claims, or other adjustments depending on the question.

| Comparison point | Enterprise value | Equity value |

|---|---|---|

| Question answered | What is the operating business worth to all capital providers? | What claim remains for common shareholders? |

| Claim level | Debt and equity perspective | Shareholder perspective |

| Formula direction | Usually common equity value plus debt-like claims minus excess or non-operating cash | Usually enterprise value minus debt-like claims plus relevant cash and non-operating assets |

| Cash-flow match | Unlevered free cash flow or operating cash-flow measures before financing | Levered equity cash flow or shareholder-level value per share |

| Multiple match | EV / EBITDA, EV / EBIT, EV / revenue, and other enterprise-level multiples | P / E, price / book, equity value per share, and shareholder-level measures |

| Capital-structure treatment | Designed to reduce distortion from different debt and cash balances | Directly affected by the company’s financing structure and shareholder claim stack |

| Common use | Operating business comparison, acquisition framing, and valuation multiples | Market capitalization, per-share value, shareholder ownership, and residual claim analysis |

| Main trap | Using EV as if it were the amount available to common shareholders | Using equity value as if debt, cash, and other capital claims did not matter |

Enterprise Value vs Equity Value Formula

Core bridge: Enterprise value = common equity value + debt and debt-like claims + preferred stock + minority interest – cash treated as excess or non-operating, with further adjustments when non-operating assets or unusual claims are material.

The bridge works because enterprise value tries to look through the financing mix. A company funded mostly with equity and a company funded with more debt may have different market capitalizations even if their operating businesses are similar. Adding debt-like claims and subtracting excess or non-operating cash helps move the calculation toward a value for the business operations rather than only the common equity claim.

The reverse bridge moves from enterprise value back toward shareholder value. Common equity value is generally estimated by moving from enterprise value back through debt-like claims, preferred stock, minority interest, cash, non-operating assets, diluted shares, and any claim-specific adjustments needed for the analysis.

Input-matching rule: Enterprise value should not be paired casually with shareholder-only metrics, and equity value should not be paired casually with operating metrics that belong to all capital providers. The value measure and the metric must describe the same claim level.

Same Company, Different Investor Question

Consider a hypothetical company with a market capitalization of $1.2 billion, debt of $500 million, cash of $200 million, preferred stock of $100 million, and minority interest of $50 million. Using the simplified bridge, enterprise value would be:

Illustrative calculation: $1.2 billion common equity value + $500 million debt + $100 million preferred stock + $50 million minority interest – $200 million cash treated as excess or non-operating = $1.65 billion enterprise value.

The same company can now support different valuation readings, depending on the question. If the investor is comparing operating business value against EBITDA, the $1.65 billion enterprise value may be the more consistent numerator. If the investor is estimating what common shareholders own, the $1.2 billion equity value and the diluted share count become more relevant.

| Investor question | Better starting value | Why the answer changes |

|---|---|---|

| How much is the operating business valued at before financing claims? | Enterprise value | Debt, cash, preferred stock, and minority interest affect the claim stack around the business. |

| What value is attached to common shareholders? | Equity value | The common equity claim is what remains after senior and non-common claims are considered. |

| Which company looks cheaper on an EV / EBITDA basis? | Enterprise value | EBITDA is before interest, so the numerator should not be only common equity value. |

| What is the implied value per diluted share? | Equity value | Per-share analysis depends on the shareholder claim and diluted share count. |

| What headline value might an acquirer discuss for the business? | Enterprise value | Acquisition framing often considers the operating business plus assumed or refinanced capital claims. |

The calculation does not prove that the stock is cheap or expensive. It only organizes the claim level. Valuation still depends on earnings quality, cash-flow durability, growth assumptions, discount rates, reinvestment needs, and the price paid for the claim being analyzed.

How to Match the Value Measure to the Input

The cleanest way to separate enterprise value from equity value is to start with the input being analyzed. The numerator and denominator should describe the same economic claim. Mixing them can make a company look cheaper or more expensive for reasons that come from the formula rather than the business.

Use enterprise value when the input belongs to the operating business. Examples include EBITDA, EBIT, revenue, unlevered free cash flow, invested-capital framing, and acquisition-style business comparisons.

Use equity value when the input belongs to common shareholders. Examples include net income to common shareholders, earnings per share, price-to-earnings analysis, book value of equity, levered equity cash flow, and implied value per diluted share.

This distinction matters most when companies have different capital structures. A low market capitalization company with heavy debt may not be as cheap as it first appears if the operating business must also support that debt. A cash-rich company may look expensive on market capitalization alone, but the enterprise value can tell a different story if excess cash is material.

Enterprise Value and Capital Structure Neutrality

Enterprise value is often described as capital-structure neutral because it reduces the immediate effect of whether a company is financed with debt or equity. That does not make enterprise value a perfect measure. It means the calculation tries to compare operating businesses before assigning the claim between lenders, preferred holders, minority interests, and common shareholders.

Capital-structure neutrality is useful when comparing companies in the same industry with different leverage. It can also be useful when valuation multiples are based on operating metrics that are available before interest expense. The benefit weakens when debt is not economically comparable, cash is restricted, minority interests are material, or non-operating assets require separate treatment.

Limitation: Enterprise value is not automatically better than equity value. It is better only when the question is about the operating business or an all-capital-provider claim. Equity value is more relevant when the question is about common shareholders, market capitalization, or per-share ownership.

Common Confusion Traps

Trap 1: treating market capitalization as the whole company value. Market capitalization reflects the value of common equity, not the entire operating business when debt, cash, preferred stock, or minority interests matter.

Trap 2: matching EV to shareholder-only earnings. Enterprise value belongs with operating-level metrics. Pairing EV with net income to common shareholders can mix claim levels.

Trap 3: ignoring diluted shares in equity value work. Equity value per share can change when options, convertibles, restricted stock, or other dilutive instruments are relevant.

Trap 4: subtracting cash without asking whether it is excess or usable. Cash treatment can be more complex when cash is restricted, needed for operations, trapped in subsidiaries, or paired with large working-capital needs.

Trap 5: using M&A language as if it always equals shareholder proceeds. Acquisition headlines often refer to enterprise value, while shareholder proceeds depend on the actual transaction structure and claim stack.

When Enterprise Value Fits Better

Enterprise value usually fits better when the analysis is about the operating company rather than the common equity slice. It is especially useful for comparing companies with different levels of debt and cash, using EV-based multiples, or analyzing business value before financing decisions.

Common enterprise-value use cases include EV / EBITDA, EV / EBIT, EV / revenue, unlevered DCF analysis, acquisition comparisons, and capital-structure comparison. The measure becomes less useful when the operating metric is weak, one-time adjustments dominate, or the business has financial assets and liabilities that do not fit a simple operating-company bridge.

When Equity Value Fits Better

Equity value fits better when the analysis is about what belongs to common shareholders. It is the more natural starting point for market capitalization, per-share value, earnings per share, price-to-earnings analysis, and shareholder dilution questions.

Equity value also matters when the investor is comparing the value of the claim being bought in the public market. Even if enterprise value gives a cleaner operating-business comparison, the shareholder outcome still depends on the equity claim, dilution, debt burden, cash use, and how much of the business value ultimately reaches common shareholders.

How the Bridge Can Mislead

The EV-to-equity bridge is simple in a textbook formula, but real analysis can become more sensitive. Preferred stock, minority interest, leases, pension obligations, restricted cash, non-operating investments, discontinued operations, and convertible securities can change the claim stack. The right treatment depends on what is being valued and which claim is being measured.

A clean bridge also requires consistent timing. Debt, cash, share count, market value, and operating metrics should refer to comparable periods when possible. Mixing a current market capitalization with stale balance sheet figures or a normalized EBITDA figure can create a valuation output that looks precise but rests on mismatched inputs.

Practical check: Before comparing EV and equity value, identify the claim level, the cash-flow level, the multiple type, the share count basis, and the date of the balance sheet inputs.

FAQ

Is enterprise value the same as equity value?

No. Enterprise value estimates the value of the operating business across debt and equity claims. Equity value estimates the value attributable to shareholders, usually starting from common equity market value.

Why is debt added to enterprise value?

Debt is added because enterprise value looks at the business value available to all capital providers. A buyer or analyst assessing the operating business needs to consider debt-like claims rather than looking only at common equity value.

Why is cash subtracted from enterprise value?

Cash is commonly subtracted because excess cash can reduce the net cost of owning the operating business. The adjustment needs care when cash is restricted, operationally necessary, or not freely available.

Which is better for valuation, enterprise value or equity value?

Neither is automatically better. Enterprise value fits operating-business and all-capital-provider analysis. Equity value fits shareholder-level and per-share analysis. The better measure depends on the metric and question being analyzed.

Can enterprise value prove that a stock is cheap?

No. Enterprise value can help compare operating business value, but it does not prove investment attractiveness. The conclusion still depends on cash flows, growth, risk, capital allocation, dilution, balance sheet quality, and the price paid for the claim.