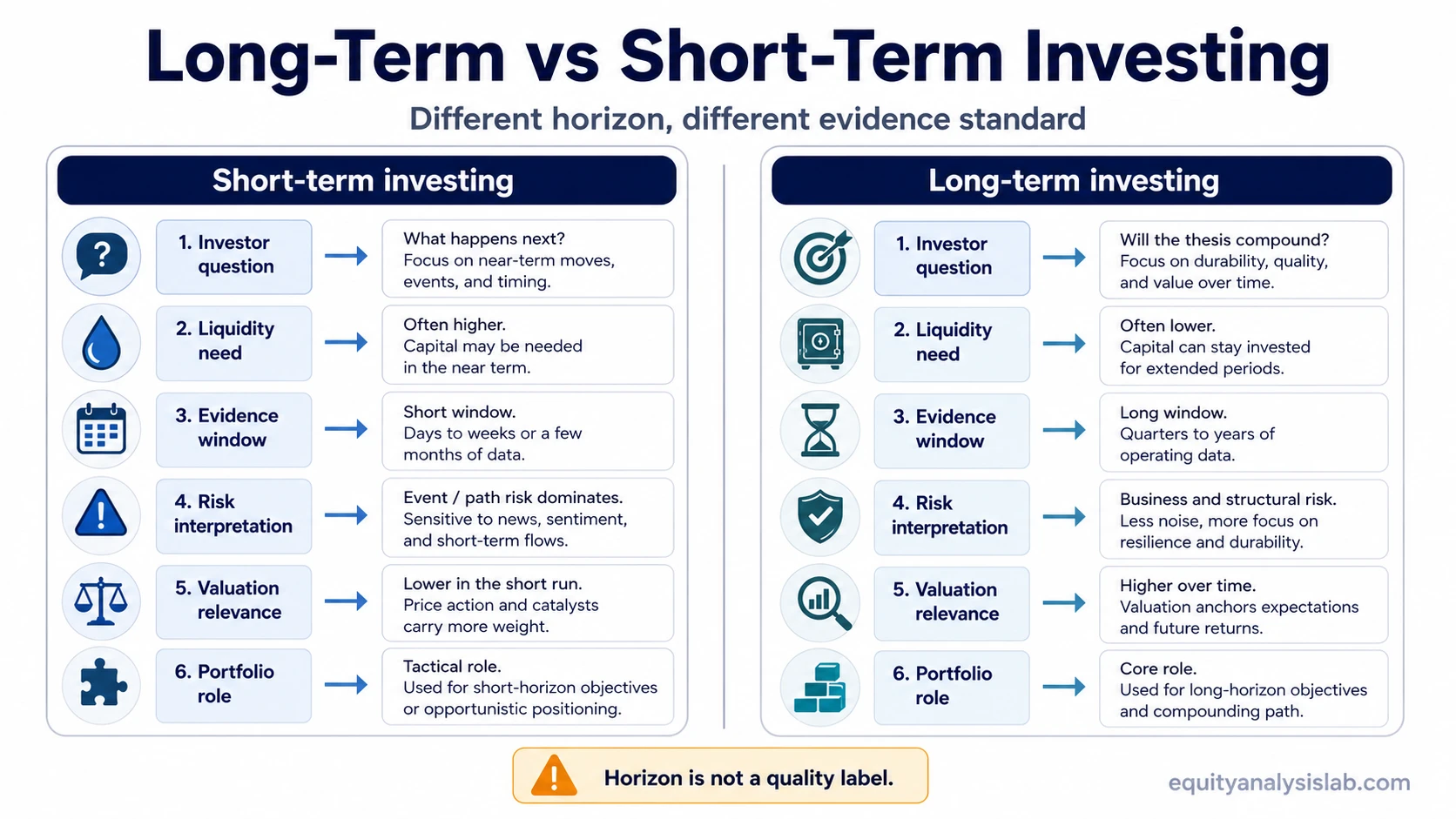

Long-term and short-term investing differ because they answer different investor questions. Short-term investing focuses on nearer-term liquidity, timing, and event or path risk. Long-term investing focuses on whether the underlying thesis, valuation, business quality, and compounding path can hold over a longer evidence window.

The difference is not only the number of months or years an investor expects to hold an asset. A holding period matters, but the more useful distinction is what the investor is trying to learn from that period. One investor may use the same stock, fund, or portfolio position to manage a near-term cash need, while another may use it to test a multi-year business or portfolio thesis.

Key points

- Long-term and short-term investing are separated by investor question, not only by calendar length.

- Time horizon changes the evidence window, liquidity need, valuation relevance, and risk interpretation.

- The same asset can be short-term or long-term depending on purpose, expected holding period, and portfolio role.

- Neither horizon proves safety, suitability, expected return, or investment quality.

Key differences between long-term and short-term investing

Short-term investing usually gives more weight to cash availability, near-term events, price path, and whether the position may need to be sold soon. Long-term investing usually gives more weight to thesis durability, valuation discipline, reinvestment, earnings quality, cash flow, and whether compounding can work through changing market conditions.

A short-term horizon does not automatically mean speculation. A long-term horizon does not automatically mean discipline. The horizon only defines the window in which the investor expects the decision to be judged, funded, monitored, and possibly changed.

| Comparison area | Short-term investing | Long-term investing |

|---|---|---|

| Investor question | Can this position serve a near-term purpose without exposing the investor to unacceptable path or liquidity risk? | Can this position remain supported by thesis quality, valuation, and business or portfolio evidence over a longer period? |

| Time horizon | Usually measured over a shorter holding period, but the exact length depends on the investor’s objective and cash-flow needs. | Usually measured over multiple years, where business results, valuation changes, reinvestment, and compounding become more relevant. |

| Evidence window | Near-term catalysts, liquidity, price path, upcoming events, and the ability to exit without disrupting the plan matter more. | Durability of earnings, cash flow, balance-sheet strength, capital allocation, competitive position, and valuation discipline matter more. |

| Liquidity need | Higher liquidity need can make drawdowns, lockups, spreads, or delayed exits more important. | Lower near-term liquidity need can allow more time for a thesis to develop, but it does not remove risk. |

| Risk interpretation | Risk is often felt through near-term price movement, timing error, event risk, and forced-sale risk. | Risk is often felt through thesis deterioration, valuation overpayment, dilution, weak cash flow, or permanent impairment. |

| Valuation relevance | Valuation can matter, but short-term outcomes may be dominated by timing, liquidity, and near-term sentiment. | Valuation usually matters more because the investor is relying on a longer path of business results and return expectations. |

| Portfolio role | The position may be used for liquidity management, temporary exposure, or a shorter defined purpose. | The position may be used as part of a longer allocation, thesis, or ownership exposure plan. |

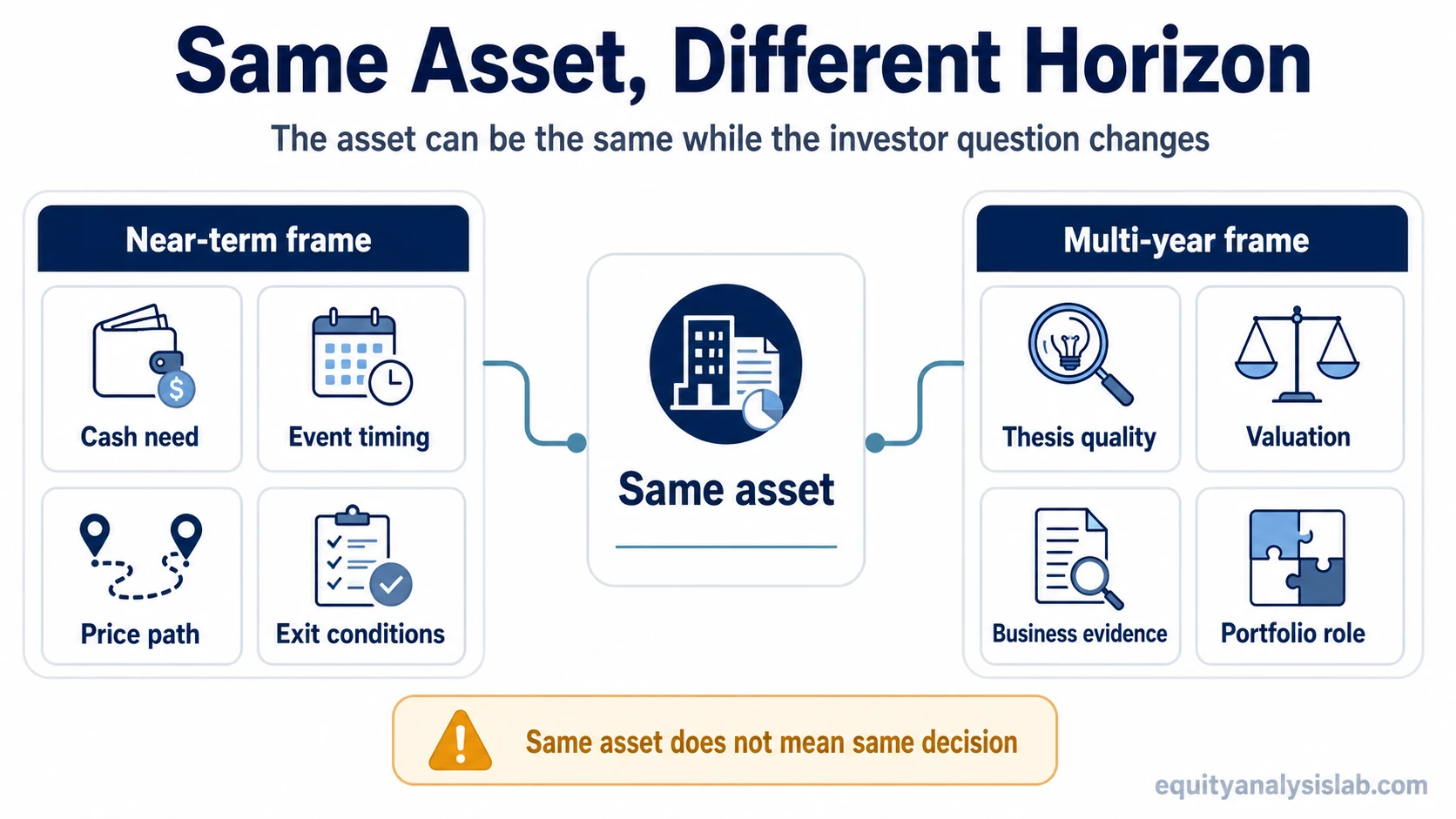

How the same asset can fit different horizons

Consider a hypothetical company. Two investors can look at the same business and reach different horizon decisions without either view being automatically right or wrong.

A short-term investor may care most about whether the position can survive an upcoming earnings release, whether liquidity is strong enough to exit if needed, and whether a near-term price decline would interfere with a cash requirement. The evidence window is narrow. Timing, event risk, and the path between purchase and sale become central.

A long-term investor may care more about whether the company can maintain margins, generate durable cash flow, avoid excessive dilution, reinvest profitably, and remain reasonably valued relative to future earnings power. The evidence window is wider. Business quality, valuation, and the possibility of compounding become more important.

The asset is the same, but the decision frame changes. That is why long-term vs short-term investing should not be treated as a simple label attached to a stock, fund, or portfolio.

What changes the evidence investors should look at

Time changes which evidence deserves more weight. A short horizon gives less time for business fundamentals to overcome bad timing, weak liquidity, or a near-term event shock. A long horizon gives more time for business evidence to matter, but it also gives more time for competition, valuation mistakes, capital allocation errors, and thesis deterioration to appear.

This is where time horizon becomes a practical concept rather than a calendar label. The relevant question is not only “how long,” but “what evidence can reasonably develop within that period?”

| Evidence type | Why it matters more in short-term analysis | Why it matters more in long-term analysis |

|---|---|---|

| Liquidity | A near-term sale may be required, so exit conditions can dominate the decision. | Liquidity still matters, but the investor may not need to sell during ordinary volatility. |

| Price path | Interim movement can determine whether the position still fits its purpose. | Interim movement matters less if the thesis and risk capacity remain intact, but it is not irrelevant. |

| Business performance | Near-term events may matter, but one short window may not reveal durable business quality. | Revenue quality, margins, cash flow, reinvestment, and capital allocation have more time to show through. |

| Valuation | Valuation can influence risk, but short-term prices may move away from fair value for reasons unrelated to business quality. | Starting valuation can strongly affect long-term return expectations because the investor relies on future business value becoming visible. |

| Behavior discipline | The risk is changing the plan when near-term price movement becomes uncomfortable. | The risk is confusing patience with ignoring broken evidence. |

Risk and return depend on the horizon being tested

Short-term investing can expose an investor to timing risk, liquidity risk, reinvestment risk, and the possibility that the asset must be sold during an unfavorable window. Long-term investing can expose an investor to valuation risk, business deterioration, dilution, weak capital allocation, and long periods where expected results fail to appear.

This is why the comparison should not be reduced to “short-term is risky and long-term is safe.” Both horizons carry risk, but the risk shows up differently. A broader discussion of risk and return helps separate volatility, permanent loss, liquidity pressure, and return expectation instead of treating them as one idea.

Longer horizons can make compounding more relevant because gains, reinvestment, and retained value have more time to affect the base. But compounding is a mechanism, not a promise. It can be weakened by overvaluation, poor cash generation, dilution, business decline, taxes, fees, or investor behavior.

Common mistake: treating horizon as a quality label

A common mistake is assuming that a long-term label makes an investment higher quality, or that a short-term label makes it automatically speculative. Horizon describes the decision window. It does not prove that the asset is good, safe, cheap, liquid, diversified, or suitable.

Another mistake is confusing horizon with investing style. Long-term investing is not the same thing as passive investing, and short-term investing is not the same thing as active trading. A passive fund can be used for a short-term liquidity purpose. An individual company position can be analyzed with a long-term thesis. Style, asset type, and holding period are related, but they are not interchangeable.

When the distinction can mislead

The long-term vs short-term investing distinction becomes misleading when it is used as a shortcut for advice. A horizon does not determine whether an investor should own a position, how much to allocate, or whether the expected return is attractive.

- A long horizon does not fix an overpaid valuation.

- A long horizon does not make weak cash flow or excessive dilution harmless.

- A short horizon does not automatically make an asset inappropriate.

- A short horizon does not remove the need to understand liquidity and downside risk.

- A tax rule, product category, or account type should not be treated as the whole distinction.

The safer interpretation is that horizon sets the evidence standard. The investor still has to evaluate valuation, risk, liquidity, business quality, cash-flow durability, and portfolio role separately.

How dollar-cost averaging changes the horizon question

Repeated contributions can make the horizon question more complicated. An investor using dollar-cost averaging may have a long-term objective while each contribution is made at a different price and in a different market condition.

That does not make dollar-cost averaging automatically better or safer. It only means the investor is separating contribution timing from the broader holding-period thesis. The investment still needs a clear purpose, a realistic evidence window, and risk that can be understood before the strategy is judged.

Related concepts to review next

Long-term vs short-term investing is easiest to understand when it is separated from nearby concepts that answer different questions.

- Time horizon: explains how the length of the decision window changes what evidence can matter.

- Risk and return: separates return expectation from the different forms of risk an investor may face.

- Compounding: explains how changes in the base can matter over longer periods without guaranteeing a result.

- Dollar-cost averaging: explains how repeated contributions interact with timing and holding-period decisions.

FAQ

Is the difference only about holding for more or less than one year?

No. Calendar length matters, but it is not the whole distinction. A shorter horizon may emphasize liquidity, event timing, and forced-sale risk, while a longer horizon may emphasize valuation, business durability, cash-flow evidence, and thesis quality.

Is long-term investing always safer than short-term investing?

No. A longer horizon can reduce the need to react to ordinary short-term volatility, but it does not remove valuation risk, business deterioration, dilution, weak cash flow, or behavioral mistakes. Horizon changes the type of risk being tested; it does not eliminate risk.

Can the same investment be short-term for one investor and long-term for another?

Yes. The same stock, fund, or portfolio position can serve different purposes. One investor may hold it for a near-term liquidity or timing reason, while another may hold it as part of a multi-year thesis. The asset is the same, but the evidence window and portfolio role are different.