Dollar cost averaging vs lump sum compares staged capital deployment with immediate capital deployment. Dollar cost averaging spreads purchases across multiple dates, while lump sum investing puts the available cash to work at once.

The practical difference is exposure timing. Dollar cost averaging reduces dependence on a single purchase date, but some cash remains uninvested while the schedule unfolds. Lump sum investing creates full exposure immediately, but the entire amount is tied to the market level on one deployment date.

Core distinction: dollar cost averaging changes the purchase schedule; lump sum investing changes the speed of market exposure. Neither method decides whether the asset is attractive, fairly valued, suitable, or likely to produce a positive result.

Key Points

- Dollar cost averaging stages capital across a defined schedule.

- Lump sum investing deploys the available amount immediately.

- DCA reduces reliance on one entry date, but can leave cash on the sidelines during rising markets.

- Lump sum creates faster exposure, but concentrates timing risk in one date.

- No method is a universal winner because the realized result depends on the market path after deployment.

- The comparison does not judge asset quality, valuation, portfolio fit, or personal suitability.

Dollar Cost Averaging vs Lump Sum: The Core Difference

Dollar cost averaging means investing fixed amounts over multiple scheduled purchases. The schedule may be monthly, quarterly, or otherwise predefined, but the important feature is that the full amount is not invested on the first day.

Lump sum investing means investing the available amount immediately. The investor receives full market exposure from the start, so the outcome is more sensitive to what happens soon after that first purchase date.

The comparison is not “cautious versus aggressive” by itself. The same investor, same asset, and same total cash amount can produce different outcomes only because the timing of exposure changes.

How the Two Methods Change Market Exposure

The biggest mechanical difference is the amount of money exposed to market movement at each point in time. Lump sum investing places the full amount into the asset immediately. Dollar cost averaging exposes only the portion already invested, while the remaining cash waits for future purchase dates.

That waiting cash creates a trade-off. If the asset rises during the deployment period, the uninvested portion may miss part of the advance. If the asset falls during the deployment period, later scheduled purchases occur at lower prices. The result depends on the path of prices, not only the final price after the schedule ends.

This is why time in market matters. Earlier exposure gives more capital the chance to participate in gains, losses, dividends, and reinvestment effects. Over long periods, those reinvestment effects can become part of a broader compounding process, but compounding still depends on the underlying asset return and the investor’s actual holding behavior.

Limitation: reducing dependence on one purchase date is not the same as eliminating risk. A staged schedule can reduce one form of timing concentration while introducing cash drag if the market moves higher before all capital is invested.

Criteria for Comparing DCA and Lump Sum

A useful comparison separates the mechanics from the decision. The mechanics describe how money enters the market. The decision still depends on the asset, valuation, risk tolerance, risk capacity, cash needs, and portfolio context.

| Criteria | Dollar cost averaging | Lump sum | What it does not prove |

|---|---|---|---|

| Deployment timing | Capital enters over several purchase dates. | Capital enters immediately. | It does not prove which asset is better. |

| Timing concentration | Less dependent on one starting market level. | More dependent on the initial deployment date. | It does not remove uncertainty from either method. |

| Cash drag | Uninvested cash may lag if the asset rises during the schedule. | No scheduled cash remains waiting after deployment. | It does not guarantee better realized returns. |

| Falling-market path | Later purchases may occur at lower prices. | The full amount participates in the decline from the start. | It does not prove that a decline will occur. |

| Rising-market path | Some cash may miss earlier gains. | The full amount participates from the first day. | It does not prove that immediate exposure is always wiser. |

| Behavioral implementation | A schedule can make deployment feel easier to follow. | A single decision removes repeated deployment choices. | Comfort is not the same as analytical superiority. |

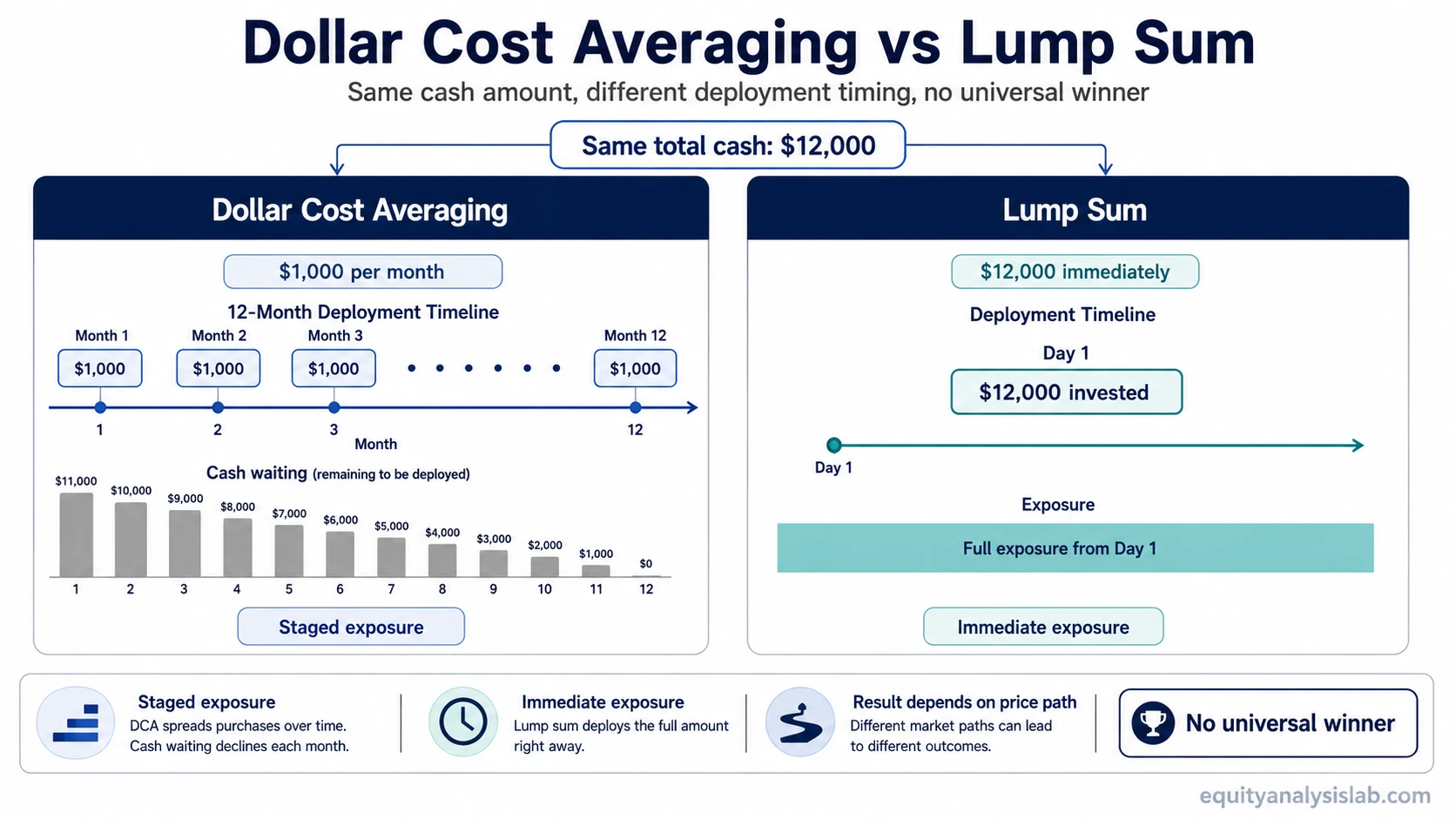

Same-Cash Example: Immediate vs Staged Deployment

Consider an investor with $12,000 available for the same diversified investment exposure. Under a lump sum approach, the full $12,000 is invested immediately. Under a dollar-cost averaging approach, $1,000 is invested each month for 12 months.

Example: if the market rises steadily during the 12-month schedule, the lump sum approach has more money exposed earlier. If the market falls during the early part of the schedule, the staged approach makes some later purchases at lower prices. If the market moves sideways with sharp swings, the difference may come less from the final level and more from the sequence of prices along the way.

The example isolates the mechanism rather than naming a winner. Lump sum investing changes exposure immediately; DCA changes the average purchase timing across the schedule.

Expected Return, Timing Risk, and Realized Results

Expected return is an estimate built from assumptions, not the actual result that will appear in an account. A method can look attractive under one assumed return path and less attractive under another path.

Lump sum investing often has more immediate exposure to the asset’s expected return because more capital is invested sooner. That does not make the realized result certain. If the asset falls soon after deployment, the larger early exposure also means the full amount participates in the decline.

Dollar cost averaging changes the timing of exposure. It may reduce regret from investing the full amount before a near-term decline, but it may also create regret if the asset rises while the schedule is still holding cash. The comparison is therefore a timing and behavior trade-off, not a forecast.

Common Mistakes When Comparing DCA and Lump Sum

A common mistake is treating DCA as automatically lower risk in every sense. DCA can reduce the risk of one poorly timed purchase date, but it does not remove market risk, valuation risk, inflation risk, or the risk of choosing a weak asset.

Another mistake is treating lump sum investing as automatically higher-quality decision-making. Immediate deployment can be mechanically efficient when the investment case is strong, but the method itself does not prove that the investment case is strong.

Confusion trap: DCA and lump sum answer a deployment question. They do not answer whether the asset should be owned, how much should be allocated, or whether the investor can tolerate the drawdown that may follow.

What This Comparison Does Not Decide

The DCA versus lump sum comparison is narrow. It clarifies how capital enters the market, not whether the investment is fundamentally attractive.

- It does not choose the asset.

- It does not prove valuation quality.

- It does not determine portfolio suitability.

- It does not forecast future returns.

- It does not replace asset allocation, diversification, or liquidity planning.

- It does not remove the need to understand risk before committing capital.

The more precise question is not simply which method is better. The better question is what kind of timing exposure, cash drag, and implementation risk each method creates under the investor’s broader plan.

FAQ

Is dollar cost averaging safer than lump sum investing?

Dollar cost averaging can reduce dependence on one purchase date, but it does not remove market risk or guarantee a better result.

Why can lump sum investing look stronger during rising markets?

Lump sum investing has more capital exposed earlier, so a rising market gives the full amount more time to participate. That does not guarantee a better result in every period.

Does dollar cost averaging avoid cash drag?

No. Dollar cost averaging can create cash drag because part of the available money remains uninvested until later scheduled purchases.

Does the DCA vs lump sum decision prove whether an investment is good?

No. The deployment method does not prove asset quality, valuation, suitability, or future return potential.