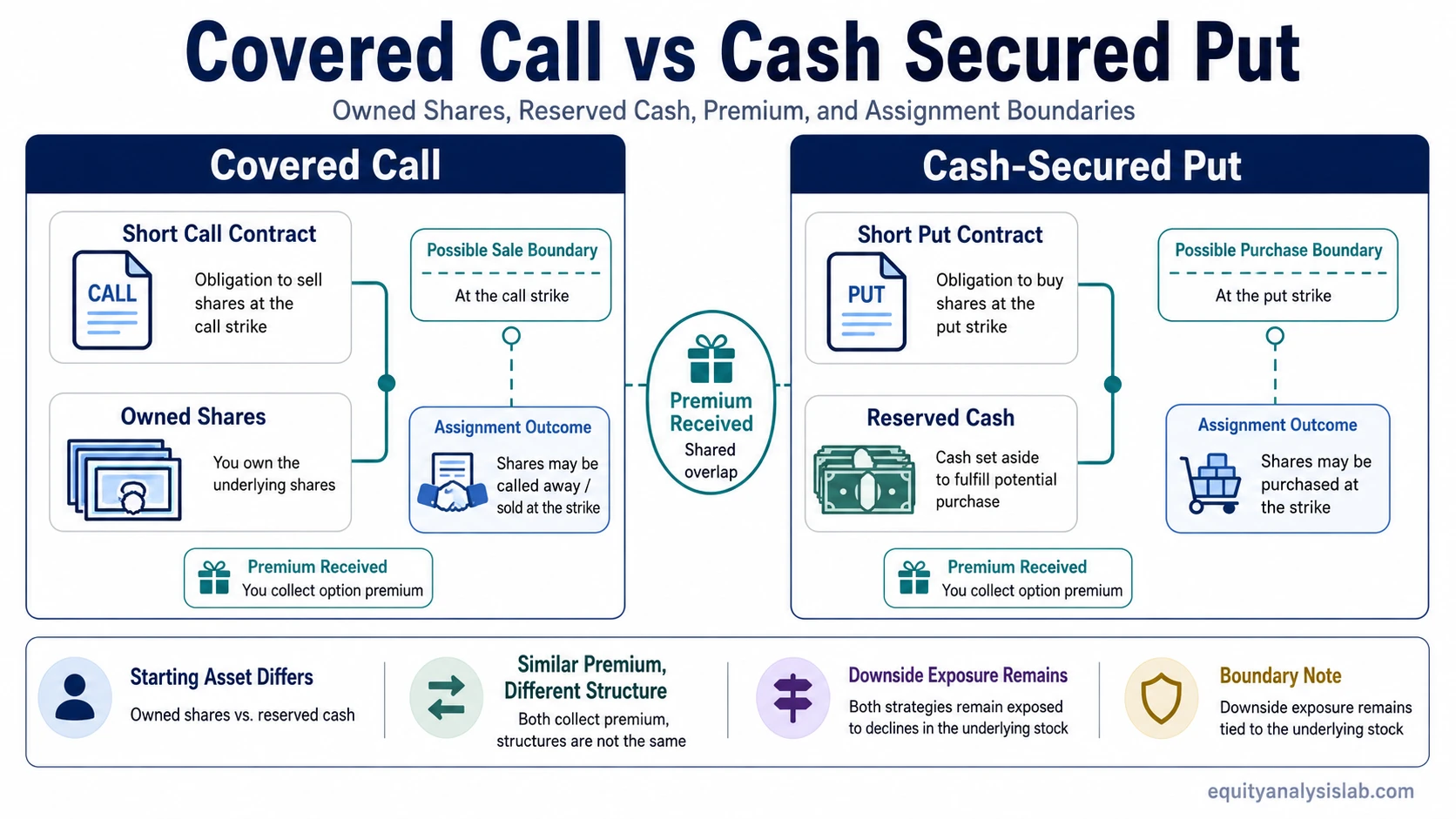

A covered call starts with shares already owned, while a cash-secured put starts with cash reserved for a possible stock purchase.

A covered call modifies an existing share position. A cash-secured put creates a possible purchase obligation from cash. Both structures collect option premium, but the starting asset, assignment outcome, and opportunity cost are different.

The real comparison is not simply call versus put. It is owned shares versus reserved cash, obligation to sell versus obligation to buy, and capped participation versus possible missed ownership if the stock rises without assignment.

Definition: A covered call sells a call option against shares already held. A cash-secured put sells a put option while holding enough cash to buy the shares if assignment occurs.

Key Points

- A covered call begins with owned shares.

- A cash-secured put begins with reserved cash.

- Both collect option premium.

- Covered call assignment can require selling shares.

- Cash-secured put assignment can require buying shares.

- Premium changes the economics but does not remove exposure to the underlying stock.

Covered Call vs Cash Secured Put: Core Difference

A covered call combines stock ownership with a short call. The investor already has the shares, collects premium from selling the call, and accepts that assignment may require selling those shares at the strike price.

A cash secured put combines reserved cash with a short put. The investor collects premium from selling the put and accepts that assignment may require buying shares at the strike price.

The overlap is premium collection. The separation is the starting asset and the contract boundary. One structure modifies an existing stock position. The other creates a possible entry into stock ownership through an assigned put.

Starting Position, Obligation, and Premium

The comparison becomes clearer when each structure is broken into the same contract variables. Premium is only one part of the structure. The starting position, assignment result, capital use, and exposure after assignment change the economic meaning.

| Criterion | Covered Call | Cash-Secured Put |

|---|---|---|

| Starting position | Shares are already owned. | Cash is reserved for a possible share purchase. |

| Option sold | Call option. | Put option. |

| Assignment outcome | Shares may be sold at the call strike. | Shares may be bought at the put strike. |

| Premium role | Premium partially offsets the economics of holding shares, but the shares can still decline. | Premium partially offsets the purchase economics if assignment occurs, but assigned shares can still decline. |

| Capital or collateral | Capital is tied to the existing shares. | Cash is set aside to cover the possible purchase obligation. |

| Upside boundary | Upside may be capped above the strike if the shares are called away. | Upside may be missed if the stock rises and the put expires without assignment. |

| Downside exposure | The owned shares can still fall in value. | Assigned shares can fall in value after purchase. |

| Ownership and dividends | Share ownership remains until shares are sold or called away, so dividend treatment depends on ownership and assignment timing. | No share ownership exists before assignment, so dividends are not received unless shares are acquired. |

Same Stock Scenario: Owned Shares vs Reserved Cash

Consider a generic stock trading at 50. One investor already owns 100 shares. Another investor does not own the shares but has enough cash reserved to buy 100 shares if assigned. Both sell an option with a 50 strike and both collect premium, but the contract boundary is different.

| Scenario element | Covered call path | Cash-secured put path |

|---|---|---|

| Initial state before assignment | The investor owns 100 shares. | The investor holds cash for a possible 100-share purchase. |

| Contract sold | A call is sold against the shares. | A put is sold against the reserved cash. |

| If the stock rises well above the strike | The shares may be called away, limiting further participation above the strike. | The put may expire without assignment, and the investor may not become a shareholder. |

| If the stock falls well below the strike | The existing shares lose value while the premium only partially offsets the decline. | The put may be assigned, creating share ownership at the strike while the premium only partially offsets the purchase economics. |

| Main boundary after assignment | Possible sale boundary for shares already owned. | Possible purchase boundary for shares not yet owned. |

Same-scenario reading: If the investor already owns shares and accepts a possible sale boundary, the structure resembles a covered call. If the investor starts with cash and accepts a possible purchase boundary, the structure resembles a cash-secured put.

Why These Structures Are Often Confused

The confusion usually comes from premium collection. Both positions receive premium up front, both can be discussed as option-selling structures, and both can be connected in a broader sequence of stock ownership and option assignment. That overlap is real, but it is incomplete.

Common mistake: Treating premium income as the same decision in both cases ignores the starting asset. The covered call question begins with an existing stock position. The cash-secured put question begins with available cash and a possible future purchase.

Risk Boundaries and Assignment Outcomes

Assignment defines how the position can change. Covered call assignment can convert stock ownership into cash by requiring delivery of shares. Cash-secured put assignment can convert cash into stock ownership by requiring purchase of shares.

Upside also differs. A covered call may give up gains above the call strike if the shares are called away. A cash-secured put may miss the stock’s advance if the stock rises and no shares are assigned. These are different opportunity costs, even when the premium received looks similar.

Boundary note: A wheel-style sequence can connect cash-secured puts and covered calls over time, but that sequence does not make the two positions identical. The comparison remains the starting position, option sold, and assignment result.

Limitation: Similar payoff shapes do not create full economic equivalence. Cash use, time value, opportunity cost, assignment terms, and broker treatment can change how the two structures behave in an actual account.

Reading the Contract Boundary

The cleanest reading starts with the asset already held, then identifies the option sold and the assignment result. That sequence separates contract structure from preference, suitability, and market outlook.

The label alone does not define risk. The underlying stock, strike, premium, expiration, account treatment, and broader portfolio process all affect how the structure behaves.

FAQ

Are covered calls and cash-secured puts the same?

No. They can both collect option premium, but a covered call starts with owned shares and a cash-secured put starts with reserved cash. Assignment also moves in opposite directions: possible share sale for the covered call and possible share purchase for the cash-secured put.

Can both covered calls and cash-secured puts lose money?

Yes. A covered call can lose value if the owned shares decline more than the premium offsets. A cash-secured put can create losses after assignment if the acquired shares decline more than the premium offsets.

Does premium remove downside exposure?

No. Premium can reduce the effective economics of the position, but it does not remove exposure to the underlying stock. A covered call remains exposed through owned shares, and a cash-secured put can become exposed through assigned shares.