SaaS valuation multiples compare the value assigned to a software company with a revenue base such as revenue, forward revenue, run-rate revenue, or annual recurring revenue. The most common reading is a revenue or ARR multiple: how many dollars of company value investors are assigning to each dollar of SaaS revenue.

The multiple is not a full valuation answer. It is an interpretation input. The same 8x revenue multiple can look aggressive, reasonable, or weak depending on revenue durability, retention, gross margin, growth, profitability path, peer quality, balance-sheet context, and the market environment around software stocks.

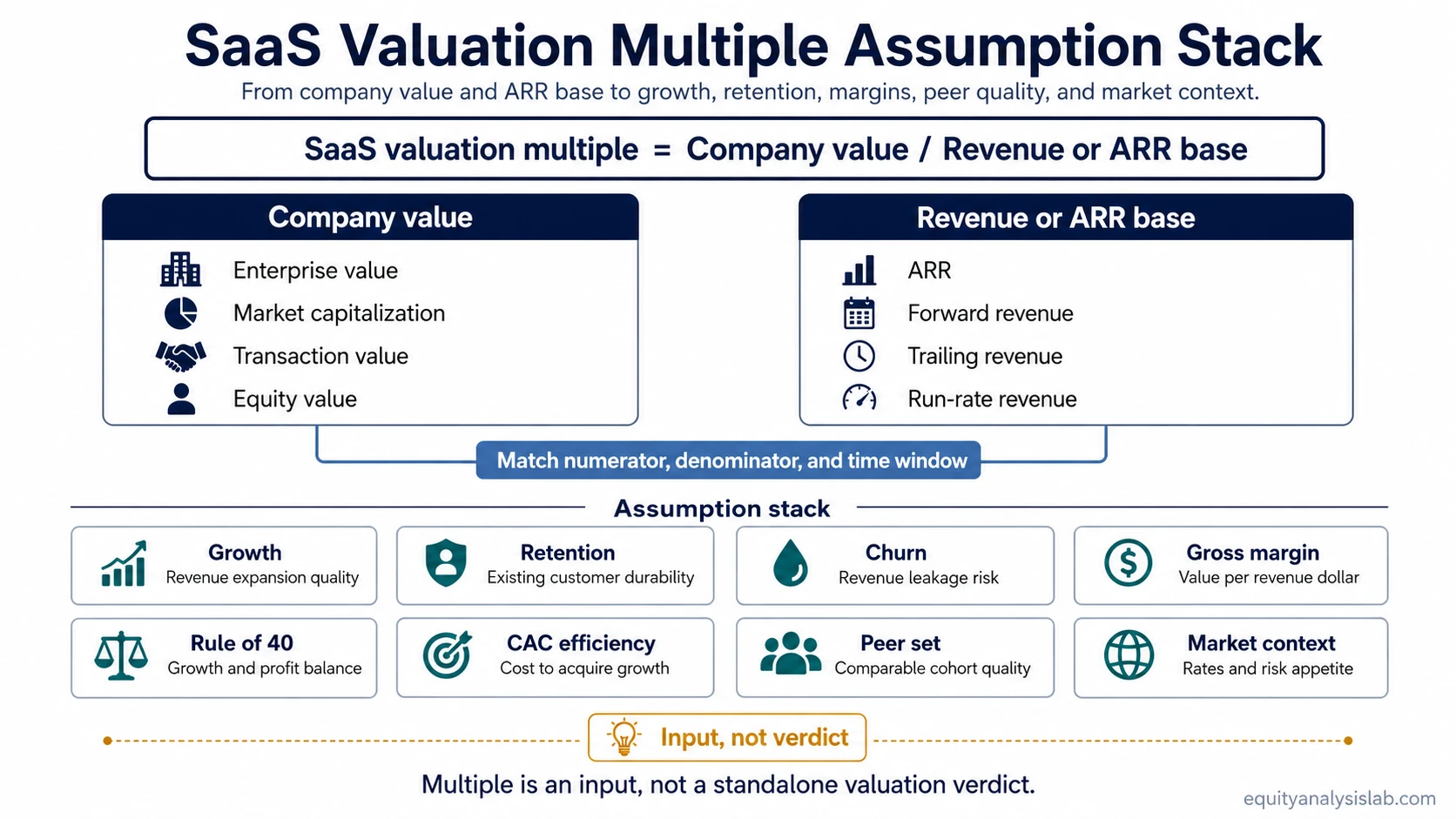

Direct definition: A SaaS valuation multiple is a ratio that compares company value with a SaaS revenue base. It helps investors normalize valuation across software companies, but it must be read together with revenue quality and business-model durability.

What SaaS valuation multiples measure

A SaaS valuation multiple measures how much value the market, a buyer, or an investor assigns to a company relative to its revenue base. In public markets, the numerator is often enterprise value or market capitalization. In private-market or acquisition analysis, the numerator may be transaction value or equity value, depending on the deal structure and the question being answered.

The denominator is usually revenue, forward revenue, run-rate revenue, or ARR. ARR is especially common when recurring subscription revenue is the economic center of the business. A revenue multiple is useful because many SaaS companies reinvest heavily in product, sales, marketing, and customer acquisition, so earnings may be low, volatile, or intentionally depressed during growth phases.

That does not make revenue a complete proxy for value. A dollar of recurring, high-retention, high-margin revenue is not the same as a dollar of one-time implementation revenue, usage-sensitive revenue, or revenue attached to weak retention. The multiple only becomes useful after the revenue base is understood.

How the formula works

The basic structure is simple, but the analytical meaning depends on matching the numerator and denominator correctly.

| Formula element | Common choices | What to check |

|---|---|---|

| Numerator | Enterprise value, market capitalization, transaction value, or equity value | The value measure must match the purpose of the analysis. Enterprise value is often better for operating-company comparisons because it adjusts for debt and cash. |

| Denominator | ARR, annualized recurring revenue, trailing revenue, forward revenue, or run-rate revenue | The revenue base must be clear, comparable, and not inflated by temporary or non-recurring items. |

| Time window | Trailing period, current run-rate, next-year estimate, or transaction-period revenue | A trailing numerator should not be casually compared with a forward denominator unless the adjustment is explicit. |

| Peer set | Public SaaS peers, private transactions, vertical SaaS peers, or growth-stage peers | The peer group must share enough growth, margin, retention, stage, and business-model similarity to make the comparison useful. |

Basic structure: SaaS valuation multiple = company value / revenue or ARR base.

For example, if a SaaS company has an enterprise value of $800 million and ARR of $100 million, the company is being valued at 8x ARR. That number is only the starting point. If the ARR is growing quickly, retention is strong, gross margin is high, and the path to profitability is credible, investors may interpret the same 8x differently than they would for a slower-growth company with high churn and weak unit economics.

Why revenue and ARR multiples are common in SaaS

Revenue and ARR multiples are common because many SaaS companies reinvest heavily before mature profitability appears. Sales, marketing, product development, and customer success costs may depress earnings even when the subscription base is expanding.

That makes revenue a practical comparison base, but only when the revenue is durable enough to justify the comparison. Recurring subscription revenue, expansion revenue, and high retention can make the denominator more meaningful. Weak retention, customer concentration, low gross margin, and heavy acquisition spend can make the same denominator less reliable.

What drives SaaS valuation multiples

The multiple is shaped by the assumptions investors attach to future revenue durability, not only by the latest revenue figure. Growth, retention, churn, gross margin, sales efficiency, profitability path, peer quality, and market context all affect the interpretation.

| Driver | Why it matters | What weakens the reading |

|---|---|---|

| Growth rate | Higher growth can support a higher multiple when the growth is durable and not purchased at any cost. | Growth becomes less valuable if it depends on inefficient sales spend, weak retention, or temporary demand. |

| Net revenue retention | Strong net revenue retention shows that existing customers can expand revenue over time. | Low retention or weak expansion means new customer acquisition must do more of the work. |

| Churn | SaaS churn rate helps show how much revenue leaks from the customer base. | High churn can make revenue growth less durable and reduce the quality of ARR. |

| Gross margin | Gross margin affects how much value each revenue dollar can eventually support. | Low gross margin can make a revenue multiple look richer than it appears at first glance. |

| Rule of 40 | The Rule of 40 gives a quick view of growth and profitability balance. | A high growth rate may be less attractive if losses are widening and operating leverage is absent. |

| CAC efficiency | SaaS customer acquisition cost affects how expensive it is to create new recurring revenue. | Growth funded by inefficient acquisition spending may deserve a lower multiple than headline growth suggests. |

| Peer set | Comparable companies help anchor the multiple in a realistic valuation context. | The comparison weakens if peers differ by size, vertical, growth, profitability, retention, or business model. |

| Market context | Risk appetite, discount rates, software-sector sentiment, and capital availability can all influence multiples. | A multiple may compress even when company fundamentals remain stable if market conditions change. |

Why the same SaaS multiple can mean different things

A multiple does not carry the same meaning across every SaaS company. An 8x ARR multiple for a company growing 35% with strong retention and high gross margin is not the same as an 8x ARR multiple for a company growing 10% with high churn and limited operating leverage.

The surface ratio can match while the business quality differs. The interpretation depends on what investors are paying for: durable recurring revenue, future margin expansion, efficient growth, strategic value, or simply a market cycle that is assigning high prices to software revenue.

Enterprise value, market cap, and transaction value

The numerator matters because each value measure answers a different question. Enterprise value is often used when comparing operating companies because it adjusts for cash and debt. Market capitalization focuses on the value of common equity. Transaction value can include acquisition-specific terms, control premiums, buyer synergies, or other deal considerations.

For public SaaS comparisons, enterprise value to revenue or enterprise value to ARR is often more useful than market capitalization to revenue because two companies with the same market cap can have very different cash and debt positions. For private transactions, the correct numerator depends on the deal structure and what the analyst is trying to compare.

ARR quality matters more than the label

ARR is useful only if it represents durable recurring revenue. Reported ARR, annualized recurring revenue, run-rate revenue, and subscription revenue can sound similar, but they may not be built from the same assumptions.

Before relying on an ARR multiple, check what is included in the revenue base. Recurring subscriptions, committed contracts, usage-based revenue, professional services, implementation revenue, discounts, and one-time items can all change the quality of the denominator.

Simple SaaS valuation multiple example

Assume a SaaS company has an enterprise value of $1.2 billion and ARR of $150 million. The enterprise value to ARR multiple is 8x.

That 8x figure does not say whether the company is cheap or expensive by itself. If the company has strong retention, expanding customer accounts, high gross margin, and improving operating leverage, the multiple may reflect a durable revenue base. If the company has high churn, weak customer economics, and slowing growth, the same multiple may rely on assumptions that are harder to defend.

How to compare SaaS valuation multiples

Useful comparison starts with matching the denominator and time window. A forward revenue multiple should not be compared casually with a trailing revenue multiple. ARR should not be mixed with total revenue if one company has more services revenue, usage-sensitive revenue, or non-recurring items.

The next step is to compare business quality. Growth, retention, churn, gross margin, customer acquisition efficiency, profitability path, and company stage all affect how much investors may pay for revenue. A cleaner comparison usually groups companies by business model, vertical, size, growth profile, and margin structure.

| Comparison step | Question to ask | Why it matters |

|---|---|---|

| Match the numerator | Are you using enterprise value, market cap, transaction value, or equity value? | Different value measures can produce different multiples for the same company. |

| Match the denominator | Are you comparing ARR, trailing revenue, forward revenue, or run-rate revenue? | The revenue base must represent the same economic period and revenue type. |

| Check revenue quality | How much revenue is recurring, expanding, retained, or one-time? | Higher-quality revenue can support a different valuation reading than weaker revenue. |

| Check growth efficiency | How much sales and marketing spend is required to create growth? | Growth that requires excessive acquisition cost may not deserve the same multiple as efficient growth. |

| Check profitability path | Is the company showing operating leverage or only revenue expansion? | Revenue growth matters more when it can plausibly convert into cash flow over time. |

When SaaS valuation multiples become misleading

SaaS valuation multiples become misleading when the ratio is separated from the assumptions behind it. A low multiple can look attractive but may reflect churn, slowing growth, customer concentration, weak margins, or doubts about the profitability path. A high multiple can reflect quality, but it can also reflect optimistic market assumptions that leave little room for disappointment.

The risk is highest when analysts compare companies only by headline multiple. The multiple should be tested against ARR quality, retention, gross margin, CAC efficiency, free cash flow potential, and peer context before it is used as valuation evidence.

How SaaS multiples connect to broader valuation work

SaaS valuation multiples are one part of broader valuation multiples analysis. They help normalize company value against revenue when earnings are not yet a stable base, but they do not replace cash-flow thinking, margin analysis, competitive positioning, or risk assessment.

For mature SaaS companies, investors may place more weight on free cash flow, operating margin, return on invested capital, and long-term earnings power. For earlier-stage companies, the revenue multiple may remain more central, but it still needs to be tested against the quality and cost of growth.

A practical checklist for reading SaaS multiples

| Question | What to inspect | Interpretation risk |

|---|---|---|

| What value measure is being used? | Enterprise value, market cap, transaction value, or equity value | The numerator may not match the comparison group. |

| What revenue base is being used? | ARR, forward revenue, trailing revenue, run-rate revenue, or total revenue | The denominator may not be comparable across companies. |

| How durable is the revenue? | Retention, churn, expansion, contract structure, and revenue mix | The multiple can overstate quality if the revenue base is fragile. |

| How efficient is growth? | CAC, payback, sales efficiency, and expansion revenue | Growth may be expensive to maintain. |

| Is profitability credible? | Gross margin, operating leverage, free cash flow trend, and Rule of 40 | The path from growth to profitability affects how much investors may pay for revenue today. |

| Is the peer set comparable? | Business model, vertical, size, growth rate, margin profile, and retention | The wrong peer set can make a multiple look cheap or expensive for the wrong reason. |

| What would break the valuation case? | Slower growth, weaker retention, higher churn, lower margins, or a less credible profitability path | The multiple is sensitive to assumptions. When the assumptions weaken, the same multiple can deserve a different reading. |

Public and private SaaS multiples need separate treatment

Public SaaS multiples and private SaaS transaction multiples should not be treated as interchangeable. Public multiples reflect liquid market pricing, current investor risk appetite, public reporting, and daily changes in software-sector sentiment. Private transaction multiples can also reflect control value, buyer synergies, financing structure, deal size, growth stage, and company-specific diligence.

That does not make public multiples useless for private-company context. They can still provide a directional reference point. The mistake is to transfer a public multiple mechanically into a private valuation without adjusting for liquidity, scale, growth quality, margin profile, retention, and deal-specific factors.

What to avoid when reading SaaS multiples

- Do not treat a high multiple as proof of quality.

- Do not treat a low multiple as proof of undervaluation.

- Do not compare ARR multiples without checking retention, churn, expansion, and revenue mix.

- Do not use public SaaS multiples as direct private-company multiples without adjustment.

- Do not mix trailing revenue, forward revenue, run-rate revenue, and ARR without making the time window explicit.

- Do not compare SaaS companies only by growth rate when gross margin, acquisition efficiency, and profitability path differ.

Bottom line

SaaS valuation multiples are useful because they normalize company value against revenue or ARR, but the ratio is only an entry point. The real analysis starts with the quality of the revenue base and the assumptions behind growth, retention, margin structure, peer set, and market context.

FAQ

Are SaaS valuation multiples the same as revenue multiples?

SaaS valuation multiples often use revenue or ARR, so they overlap with revenue multiples. The difference is that SaaS analysis usually places more weight on recurring revenue quality, retention, churn, expansion, gross margin, and customer acquisition efficiency.

Why do SaaS companies often use revenue or ARR multiples?

Revenue and ARR multiples are common because many SaaS companies reinvest heavily, which can make near-term earnings less useful as a comparison base. Revenue-based multiples help normalize companies before mature profitability is visible, but they still require quality checks.

Does a higher SaaS valuation multiple mean a better company?

No. A higher multiple can reflect stronger growth, retention, margins, and market confidence, but it can also reflect overly optimistic assumptions. The multiple has to be tested against revenue quality, peer context, and the path to profitability.

Can private SaaS multiples be compared with public SaaS multiples?

They can be compared directionally, but not mechanically. Public multiples reflect liquid market pricing, while private multiples may include control premiums, buyer synergies, financing terms, deal size, and company-specific diligence.

Related concepts to compare next

For revenue-base quality, compare SaaS valuation multiples with ARR, net revenue retention, SaaS churn rate, and gross margin. For growth efficiency, compare the multiple with SaaS customer acquisition cost and the SaaS magic number. For valuation context, compare it with valuation multiples and price-to-sales ratio.