Stock selection criteria are the standards investors use to decide which companies deserve deeper research. They organize evidence around investor objective, business quality, financial strength, valuation context, risk, and portfolio fit.

The criteria do not predict returns, prove that a stock is attractive, or replace judgment. A useful stock selection framework narrows the research universe first, then tests whether the evidence is complete enough to support further analysis.

Key Points

- Stock selection criteria work best as an evidence sequence, not as a mechanical scorecard.

- Investor objective and time horizon come before business, financial, and valuation filters.

- Screening tools can find candidates, but they cannot judge business quality, risk, or context by themselves.

- Criteria become weaker when the evidence conflicts, the companies are not comparable, or valuation ignores risk.

What Stock Selection Criteria Means

Stock selection criteria are the filters and judgment standards used to decide whether a company fits a research process. They can include business quality, financial durability, valuation, balance-sheet risk, earnings quality, portfolio role, and time horizon.

The important distinction is that criteria are inputs. They help organize evidence, but they do not create a final decision by themselves. A company can pass a valuation screen and still have weak cash flow, poor balance-sheet flexibility, deteriorating margins, or risks that make the apparent opportunity less useful.

Why Criteria Start With Investor Context

Investor context comes first because the same company can fit one research process and fail another. A long-term investor looking for durable cash generation may use different criteria from an investor studying cyclical recovery, dividend stability, or valuation dislocation.

The starting point is usually objective, time horizon, risk tolerance, and portfolio role. Without that context, stock selection criteria can turn into a loose list of ratios that appear precise but do not answer what the investor is actually trying to evaluate.

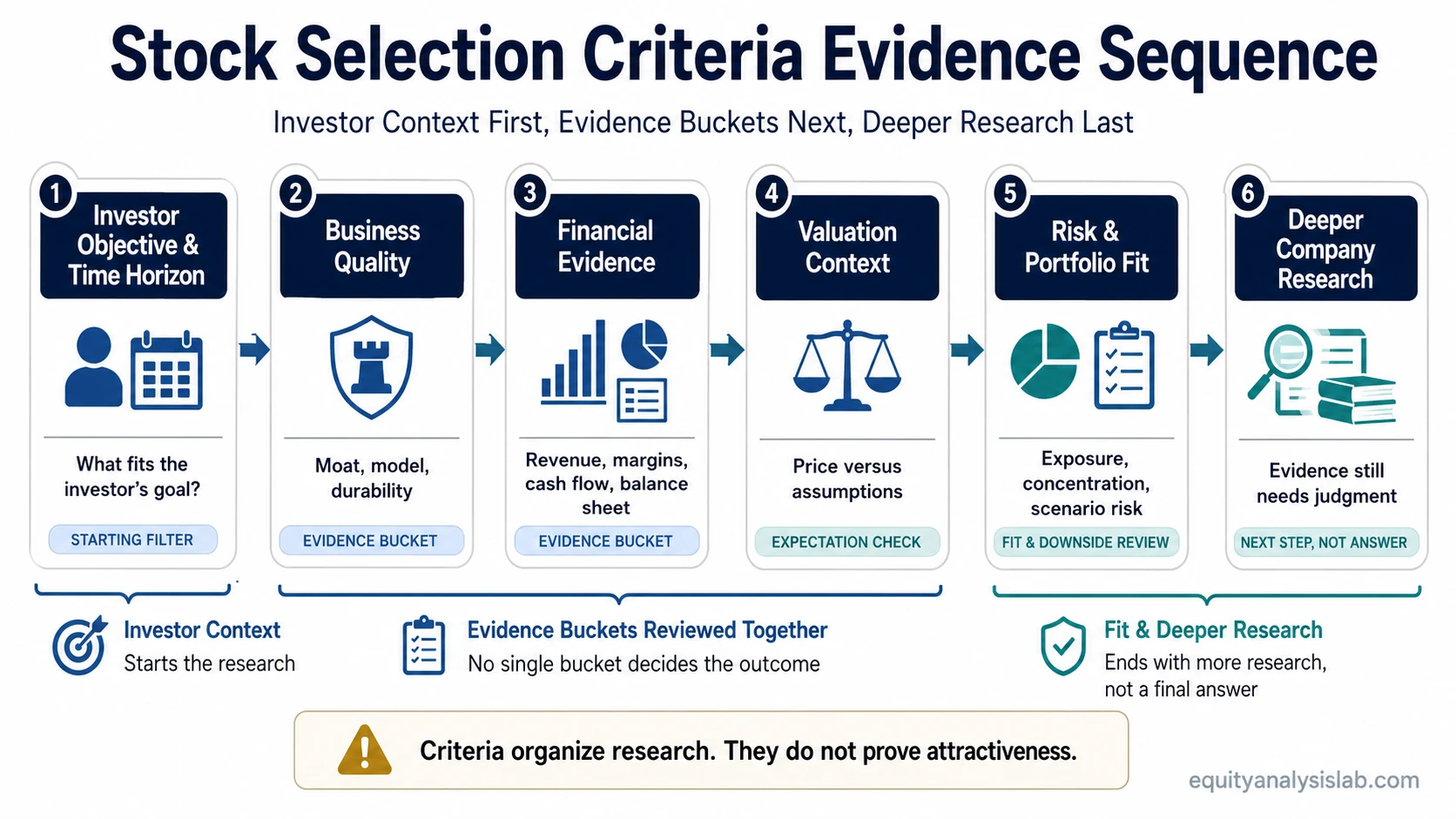

The Main Stock Selection Criteria Buckets

A useful stock selection process usually moves from broad fit to company-specific evidence. The order matters because later criteria can change the meaning of earlier ones.

| Criteria bucket | Evidence source | What it can show | What it cannot prove |

|---|---|---|---|

| Investor objective | Time horizon, portfolio role, risk limits, required liquidity | Whether the company belongs in the research universe | Whether the stock is attractive at the current price |

| Business quality | Competitive position, pricing power, customer durability, business model structure | Whether the company may have durable operating advantages | Whether those advantages are already priced into the stock |

| Financial evidence | Revenue, margins, cash flow, balance sheet, capital efficiency | Whether the business is converting activity into usable financial results | Whether the financial pattern will continue unchanged |

| Valuation context | Multiples, earnings expectations, cash-flow assumptions, peer context | Whether the market price reflects demanding or conservative expectations | Whether a low multiple is automatically cheap or a high multiple is automatically expensive |

| Risk and portfolio fit | Debt, cyclicality, concentration, volatility, downside scenarios | Whether the position would add a suitable type of exposure | Whether the investment outcome will be positive |

Business Quality Criteria

Business quality criteria ask whether the company has a durable reason to earn acceptable returns over time. The evidence can include pricing power, repeat demand, customer retention, cost advantages, network effects, scale benefits, or other sources of economic moat.

This layer should not be reduced to brand strength or growth language. A company may look attractive because revenue is expanding, but weak customer economics, low switching costs, or rising competitive pressure can reduce the value of that growth.

Financial Evidence Criteria

Financial evidence tests whether the business quality argument appears in the numbers. Revenue durability, gross margin, operating margin, free cash flow, debt structure, dilution, and capital efficiency can all change the interpretation.

Capital efficiency is especially useful because growth funded by heavy reinvestment may not create much value if returns are weak. Measures such as returns on invested capital can help separate high-quality expansion from expansion that consumes capital without producing attractive economics.

No single metric should carry the whole decision. A margin trend can look strong while cash conversion weakens. A balance sheet can look safe until refinancing risk changes. A revenue pattern can look stable while customer concentration creates hidden fragility.

Valuation and Expectation Criteria

Valuation criteria ask what expectations are already embedded in the stock. A low multiple does not automatically mean undervaluation, and a high multiple does not automatically mean overvaluation. The multiple has to be read against growth quality, cash flow, balance-sheet risk, cyclicality, and the durability of earnings.

For example, a company may look inexpensive on earnings multiple context, but that signal weakens if earnings are cyclical, cash conversion is poor, or the balance sheet limits flexibility. The reverse can also happen: a higher multiple may be less concerning when revenue quality, margins, reinvestment returns, and balance-sheet strength support the expectations.

Risk, Time Horizon, and Portfolio Fit

Risk criteria connect the company to the investor’s broader process. They can include business cyclicality, debt maturity, currency exposure, customer concentration, regulatory exposure, liquidity, volatility, and the effect of adding the stock to an existing portfolio.

Time horizon changes the weight of these criteria. A temporary earnings decline may matter less if the business has durable cash flow and a long recovery window. The same decline may matter more when leverage is high, refinancing risk is near, or the thesis depends on quick improvement.

Portfolio fit also matters because a strong company can still create concentration risk. If a portfolio already has heavy exposure to one sector, factor, geography, or business model, another similar position may increase fragility rather than improve the overall research set.

How Screeners Support the Criteria

Screeners are useful for narrowing a large universe into a smaller research list. A stock screener filter can identify companies with certain valuation multiples, margins, growth rates, balance-sheet metrics, or dividend characteristics.

The limitation is that screeners usually capture outputs, not full interpretation. They may show that a company meets a numerical threshold, but they do not explain whether the number is sustainable, comparable across industries, supported by cash flow, or distorted by accounting, cyclicality, or one-time effects.

When Stock Selection Criteria Fail

Stock selection criteria become unreliable when they are used without context. The most common failure is treating a passed filter as a conclusion.

- Unclear objective: Criteria cannot work well when the investor has not defined time horizon, risk tolerance, or portfolio role.

- Incomplete evidence: Valuation, quality, growth, and risk need to be read together rather than in isolation.

- Wrong comparison set: A metric may mean different things across sectors, capital structures, and business models.

- Quality and valuation conflict: A strong company may be priced for very optimistic assumptions, while a cheap stock may be cheap for structural reasons.

- Risk is treated as secondary: Debt, dilution, cyclicality, concentration, and liquidity can change the meaning of otherwise attractive criteria.

Stock Selection Criteria Example in Context

Consider two companies with similar revenue growth and similar valuation multiples. The first company converts a large share of revenue into free cash flow, carries modest debt, and earns stable returns on capital. The second company grows at a similar rate but needs heavy reinvestment, has thinner margins, and relies on a more cyclical customer base.

A simple screen may place both companies in the same candidate list. A criteria-based process would not treat them as equal. Business quality, cash conversion, balance-sheet risk, capital efficiency, and time horizon change how the same growth and valuation numbers should be interpreted.

The useful conclusion is not that one company is automatically better. The useful conclusion is that stock selection criteria should expose where the next layer of research is needed.

Related Concepts for Deeper Research

A practical research sequence usually starts with business quality: whether the company has durable advantages, pricing power, repeat demand, or other reasons to sustain returns.

Financial evidence comes next because quality claims need support from margins, cash conversion, balance-sheet resilience, and capital efficiency.

Screening tools can narrow the universe, but their output still needs context before it becomes a serious research candidate.

Valuation context closes the sequence by testing whether the stock price already reflects optimistic, conservative, or fragile expectations.

FAQ

Are stock selection criteria the same as a stock-picking checklist?

No. A checklist can help standardize review, but stock selection criteria are broader judgment standards. They define which evidence matters, how the evidence should be sequenced, and when a company needs deeper research.

Can a stock screener replace stock selection criteria?

No. A screener can find companies that match numerical filters, but it cannot fully judge business quality, cash-flow durability, valuation expectations, sector context, or portfolio fit.

Which stock selection criteria matter most?

The most useful criteria depend on objective and time horizon. For many investor research processes, business quality, financial durability, valuation context, balance-sheet risk, and portfolio fit need to be read together.