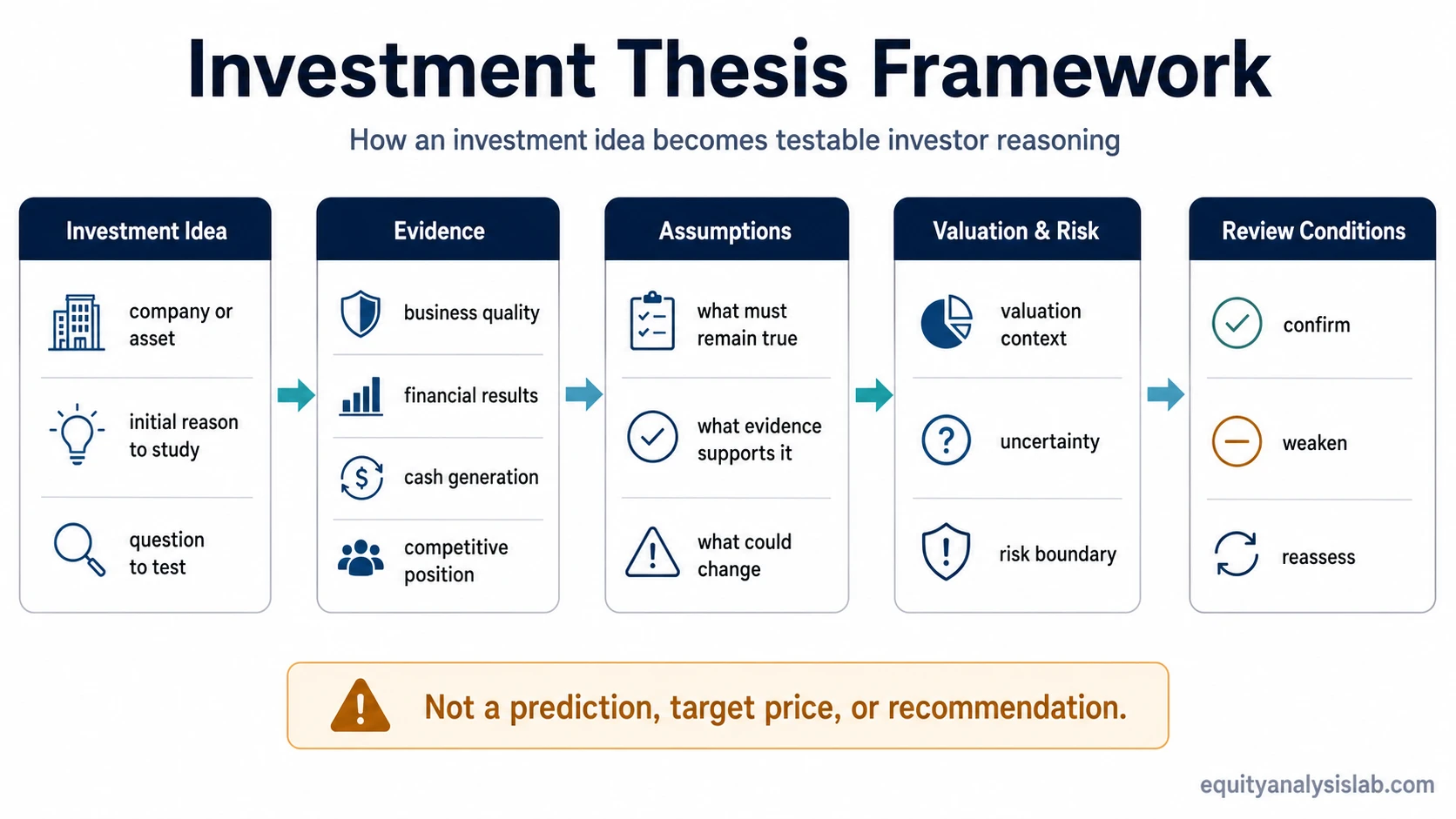

An investment thesis is a research-backed explanation of why an investor believes a company, asset, or strategy may be attractive, mispriced, risky, or worth further analysis under specific assumptions.

It connects observable evidence to an investor decision process. A thesis can include business quality, financial results, valuation, risk limits, and the conditions that would weaken or change the original interpretation.

An investment thesis is not a prediction, guarantee, target price, or statement of personal conviction. It is a testable line of reasoning that helps an investor decide which facts matter and what would make the idea less credible.

What Is an Investment Thesis?

An investment thesis is the central reasoning behind an investment idea. It explains what the investor believes, why that belief may be reasonable, what evidence supports it, and which assumptions must remain intact for the idea to stay valid.

For an equity investor, a thesis often links the company’s business model, competitive position, financial performance, valuation, and risk profile. The thesis does not need to be complex, but it must be specific enough to be tested against new information.

A useful thesis separates the reason to study an investment from the decision to own it. A company may look interesting because it has strong economics, but the thesis still needs valuation context, risk awareness, and evidence that can be monitored over time.

Key Points About an Investment Thesis

- An investment thesis turns a broad investment idea into structured reasoning.

- It should connect evidence, assumptions, valuation, and risk limits.

- It is stronger when the investor can identify what would confirm, weaken, or invalidate it.

- It is weaker when it only says a company is good, cheap, popular, or likely to rise.

- It does not prove that an investment will work or that a stock should be bought, held, or sold.

What an Investment Thesis Is Used For

An investment thesis is used to organize investor judgment. It helps define why an idea deserves attention, which facts matter most, and what evidence should be monitored after the initial research is complete.

Without a thesis, an investor can confuse a story with an analysis. A company may have a strong brand, a popular product, or a rising share price, but those observations do not become a thesis until they are connected to durable economics, cash generation, valuation, and risk.

The practical value of a thesis is discipline. It gives the investor a reference point for reviewing new earnings reports, changes in competitive position, valuation changes, and emerging risks. When the evidence changes, the thesis can be reviewed instead of defended automatically.

Core Evidence Behind an Investment Thesis

The evidence behind an investment thesis depends on the type of company and the investor’s process, but most equity theses rely on a small set of recurring evidence categories.

| Evidence source | Investor interpretation | Assumption being tested | Limitation |

|---|---|---|---|

| Business quality | Whether the company can defend returns, pricing, or customer relationships | The company has durable advantages rather than temporary momentum | Quality can fade if competition, regulation, or customer behavior changes |

| Financial evidence | Whether revenue, margins, earnings, and cash generation support the story | The business model converts activity into durable owner value | Accounting profits can look stronger than cash economics |

| Valuation context | Whether the current price leaves enough room for the thesis to matter | The market is underestimating, overestimating, or misreading the company | A good business can still be a poor opportunity if expectations are too high |

| Risk boundary | What could make the thesis incomplete, outdated, or wrong | The downside risks are identifiable rather than ignored | Some risks are uncertain until new evidence appears |

| Thesis-change conditions | Which facts would require the investor to reassess the idea | The thesis is testable and not only a fixed opinion | Evidence may be mixed before it becomes decisive |

For example, business-quality evidence may include whether a company has an economic moat, but the thesis should still ask whether that advantage is visible in financial results and valuation expectations.

Financial evidence can include margins, reinvestment needs, debt, earnings quality, and free cash flow. A thesis becomes more useful when these inputs test the business story rather than simply decorate it.

How Evidence Becomes an Investor Assumption

Evidence becomes part of an investment thesis only when it supports a specific assumption. A high margin is not a thesis by itself. It becomes thesis evidence when the investor explains why that margin may persist, expand, normalize, or come under pressure.

The same rule applies to valuation. A stock may look inexpensive on one metric, but the thesis needs to explain what the market may be missing and whether valuation relative to intrinsic value leaves enough room for uncertainty.

A stronger thesis states both the positive assumption and the review condition. For example, the investor may believe that durable cash generation supports reinvestment and shareholder value, while also identifying the evidence that would force reassessment, such as lower margins, weaker demand, declining cash conversion, or expectations that already reflect the optimistic case.

What an Investment Thesis Cannot Prove

An investment thesis cannot prove that an investment will succeed. It can only explain why the idea may be reasonable under the evidence and assumptions available at the time.

A thesis cannot remove valuation risk, business risk, market risk, or uncertainty. It also cannot turn preference into proof. Saying that a company is well managed, popular, or high quality is not enough unless the claim is tied to evidence and to conditions that can later be reviewed.

A thesis can also be reviewed against the broader risk-on risk-off environment, but that regime label should remain separate from company-level evidence, valuation, and thesis-change conditions.

The thesis can also become outdated. New competition, weaker cash flow, deteriorating unit economics, capital allocation mistakes, or valuation expansion can all change the balance between evidence and risk. A margin of safety can help frame uncertainty, but it does not guarantee protection if the thesis itself is wrong.

Investment Thesis Example

A weak statement says: “This is a high-quality company, so the stock is attractive.” That is an opinion, not a complete investment thesis.

A stronger thesis would connect the quality claim to specific evidence. It might say that the company appears to have durable margins, recurring cash generation, disciplined reinvestment opportunities, and valuation expectations that do not fully reflect those strengths. It would also state what could weaken the thesis, such as margin compression, slower growth, weaker cash conversion, or a valuation that already discounts the optimistic case.

This example is illustrative only. It does not describe a real company or recommend an investment action. Its purpose is to show that a thesis needs evidence, assumptions, valuation context, and review conditions rather than a vague positive view.

Common Mistakes When Reading an Investment Thesis

Mistake 1: Treating a thesis as a forecast. A thesis explains why an idea may be reasonable; it does not predict a certain return.

Mistake 2: Treating conviction as evidence. Confidence can be useful, but it is not a substitute for observable business, financial, and valuation support.

Mistake 3: Treating a target price as the thesis. A valuation output may summarize an estimate, but the thesis is the reasoning that explains the estimate and the conditions behind it.

Mistake 4: Ignoring what would make the thesis wrong. A thesis that cannot be challenged is usually too vague to guide decision-making.

Related Concepts

An investment thesis is easier to evaluate when the investor separates business evidence, financial evidence, valuation context, and risk boundaries.

- Economic moat helps frame whether a company may have durable competitive advantages.

- Free cash flow helps test whether reported performance converts into cash economics.

- Intrinsic value helps connect business assumptions to valuation judgment.

- Margin of safety helps frame uncertainty when valuation and thesis risk are both present.

FAQ

Is an investment thesis the same as a stock prediction?

No. An investment thesis explains why an investment idea may be reasonable under specific evidence and assumptions. It does not predict a certain price move, return, or outcome.

What should an investment thesis include?

An investment thesis should include the core idea, supporting evidence, key assumptions, valuation context, risk boundaries, and the conditions that would weaken or change the thesis.

Is a target price an investment thesis?

No. A target price is a valuation output or estimate. The investment thesis is the reasoning that explains why the estimate may or may not be justified.