Stocks can fall when interest rates rise because higher rates can lower the present value of future cash flows, raise company financing costs, weaken demand, pressure earnings expectations, and make bonds or cash more competitive.

That pressure is real, but it is not automatic. Stocks can also rise during periods of higher rates when earnings growth, liquidity, sector leadership, or investor expectations offset the valuation pressure. The useful question is not only whether rates are rising. The useful question is which pressure channel is active, whether earnings are absorbing it, and whether the market already priced it in.

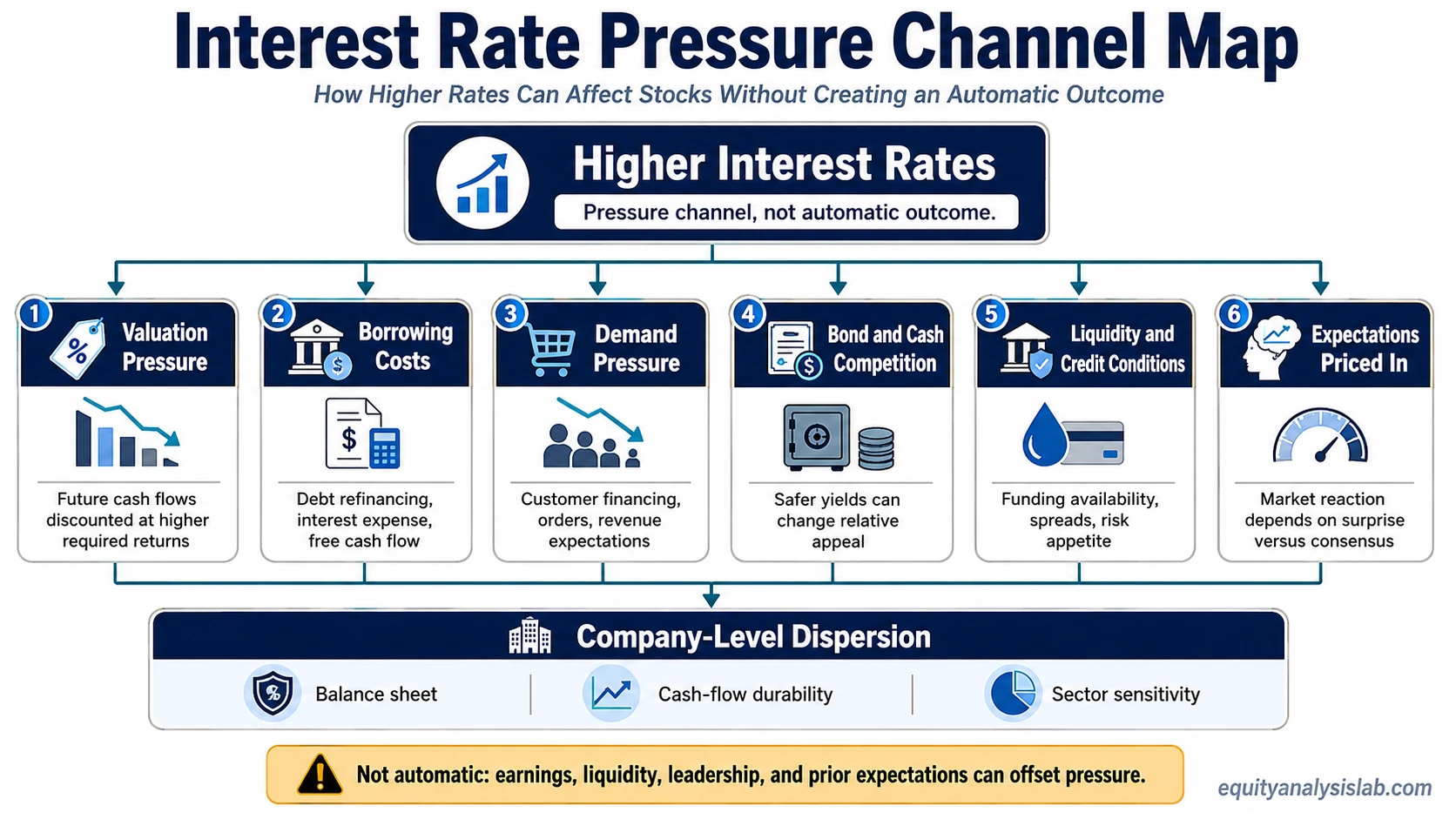

Core idea: Rising rates are a pressure channel for equity prices. They are not a complete investment decision, a recession forecast, or proof that all stocks should move in the same direction.

Why Stocks Can Fall When Interest Rates Rise

Stock prices are partly based on expected future cash flows. When interest rates rise, those future cash flows are often discounted at a higher required return. That can reduce the value investors are willing to pay today, especially for companies whose expected profits sit far in the future.

Higher rates can also change the earnings side of the equation. A company may face higher interest expense when it refinances debt, customers may reduce spending if borrowing becomes more expensive, and investors may demand lower valuation multiples if safer yields become more attractive. The result can be pressure on both earnings expectations and valuation at the same time.

The pressure becomes more visible when rising rates coincide with weakening earnings revisions, tighter credit conditions, narrower market leadership, or falling market breadth. In that environment, rate pressure can contribute to bear market conditions, but it does not prove that a bear market has started.

The Main Channels That Pressure Stock Prices

Interest rates can affect stocks through several channels at once. Separating those channels helps prevent a vague “rates are bad for stocks” reading from replacing actual analysis.

| Rate channel | What it can pressure | What to check | Why it can mislead |

|---|---|---|---|

| Discount-rate / valuation multiple pressure | Present value of future cash flows and valuation multiples | Forward multiples, long-term earnings assumptions, and real-rate direction | Strong earnings growth can offset some multiple pressure. |

| Company borrowing costs | Interest expense, refinancing risk, and free cash flow | Debt maturity schedule, floating-rate debt, interest coverage, and credit rating pressure | Cash-rich companies or firms with fixed long-term debt may be less exposed. |

| Consumer demand / revenue pressure | Sales volumes, order growth, and margin expectations | Customer financing sensitivity, backlog quality, pricing power, and earnings revisions | Some businesses can pass through costs or keep demand stable despite higher rates. |

| Bond and cash competition | Relative appeal of equities versus lower-risk income alternatives | Treasury yields, cash yields, equity risk premium, and dividend yield context | Higher bond yields do not automatically make every stock unattractive. |

| Liquidity and credit conditions | Risk appetite, funding availability, and speculative activity | Credit spreads, lending standards, market breadth, and liquidity-sensitive sectors | Liquidity can tighten unevenly, with some companies affected much more than others. |

| Expectations already priced in | Market reaction to new rate information | Prior price move, consensus expectations, earnings guidance, and rate-path surprises | Stocks can rise after a rate increase if the outcome was expected or less severe than feared. |

Why the Relationship Is Not Automatic

Stocks do not fall simply because a rate number moves higher. The reason rates are rising matters. Rates can rise because inflation is still too high, because growth expectations are improving, because bond investors demand more compensation, or because policy is becoming more restrictive. Each setting affects equities differently.

A stronger economy can sometimes support revenue and earnings even while rates rise. A bull market phase can continue if earnings growth, liquidity, and leadership remain strong enough to absorb the pressure from higher discount rates. The same rate move can look very different when earnings estimates are rising than when earnings estimates are falling.

Condition: Rates rise while earnings revisions weaken, credit spreads widen, and valuation multiples compress.

Interpretation: Stocks may face pressure because both the discount-rate channel and earnings channel are moving against valuations.

Limitation: That still does not prove a recession, a bear market, or a universal decline across all stocks. Company quality, balance-sheet strength, sector exposure, and prior expectations can change the outcome.

Why Some Companies React Differently

“Stocks” do not react as one uniform asset. Rate sensitivity depends on business model, balance sheet, cash-flow timing, customer base, and investor expectations.

Long-duration growth companies can be more sensitive when much of their expected value depends on profits far in the future. A higher discount rate can have a larger effect on those distant cash flows than on a mature company already producing durable free cash flow.

Highly leveraged firms can face greater pressure when refinancing costs rise. If debt matures soon, or if a company uses floating-rate borrowing, higher rates can move quickly into interest expense. The risk is different for a company with large cash reserves, low debt, or fixed-rate obligations that do not need refinancing soon.

Real estate-sensitive businesses often face pressure because property values, mortgage affordability, financing costs, and capitalization rates can all respond to rate changes. Banks and financials can react differently again: higher rates may improve some lending spreads, but credit losses, deposit costs, and loan demand can change the result.

Demand-sensitive and cyclical companies may be more exposed when higher rates slow customer spending or business investment. Defensive businesses may hold up better when demand is stable, but defensive labels are not safety guarantees. Commodity-linked companies can also behave differently if inflation, supply constraints, or global demand support cash flows while rates rise.

Example: A highly leveraged growth company with near-term refinancing needs can face multiple pressure points at once: higher interest expense, lower valuation tolerance, and weaker demand expectations. A cash-generative company with low debt and stable demand may face the same rate backdrop but a much smaller earnings or balance-sheet hit.

What Investors Can Check Before Interpreting Rate Pressure

Rate direction becomes more useful when it is checked against market and company evidence. A rising yield alone is too broad to explain whether equity pressure is valuation-led, earnings-led, liquidity-led, or already priced in.

Interest-Rate Pressure Checklist

- Treasury yield direction and real rates: Check whether nominal yields and inflation-adjusted yields are both moving higher.

- Earnings revisions: Look for whether analysts and management guidance are moving expected earnings up or down.

- Valuation multiples: Compare multiple compression with changes in earnings expectations.

- Credit spreads and liquidity conditions: Wider spreads can show that credit risk is rising alongside rates.

- Sector leadership: Identify whether leadership is broad or concentrated in a narrow group of less rate-sensitive companies.

- Market breadth: Weak breadth can show that headline index strength is masking pressure beneath the surface.

- Company refinancing exposure: Review maturity schedules, floating-rate debt, and interest coverage.

- Cash-flow durability: Test whether the company can keep producing cash if demand slows or financing costs rise.

Common Mistakes When Reading Rates and Stocks

| Mistake | Safer interpretation |

|---|---|

| Treating rate direction as a market timing signal | Higher rates can pressure stocks, but rate direction alone does not define an entry point, exit point, or market phase. |

| Assuming all valuation pressure is the same | A profitable company with strong cash flow, low debt, and durable demand is not exposed in the same way as a speculative company that depends on future financing and distant earnings. |

| Ignoring expectations | Markets react to surprises, not only to the level of rates. A rate increase can be less damaging if it was already priced in, while a smaller move can matter if it changes future expectations. |

| Using bond competition as a complete answer | Higher cash or bond yields can compete with stocks, but equities also reflect growth, earnings durability, reinvestment potential, and long-term business quality. |

Rising rates are a pressure channel, not a complete investment decision. They do not guarantee stock declines, multiple compression, recession, or identical reactions across companies.

Related Market Cycle Concepts

Rate pressure often appears inside broader market-cycle interpretation, but it should not replace cycle analysis. A market can weaken when rates rise, earnings expectations fall, and breadth deteriorates together. A market can also remain resilient when earnings, liquidity, and leadership offset higher discount rates.

A more useful interpretation separates three questions: what rates are doing, how companies are absorbing the pressure, and whether market behavior confirms broad deterioration or only selective repricing.

FAQ

Do stocks always fall when interest rates rise?

No. Stocks can fall when higher rates pressure valuations, earnings, borrowing costs, demand, or liquidity, but the effect is not automatic. Earnings growth, sector leadership, balance-sheet strength, and prior expectations can change the outcome.

Why do growth stocks often react more strongly to rising rates?

Growth stocks often depend more on profits expected far in the future. When discount rates rise, those distant expected cash flows can lose more present value than near-term cash flows from mature, profitable companies.

Can rising rates happen during a bull market?

Yes. Rising rates can occur during a bull market when earnings growth, liquidity, productivity, or sector leadership remain strong enough to offset valuation pressure. The rate move needs to be read alongside earnings and market breadth.