Cyclical stocks are companies whose demand, margins, earnings, and valuation perception tend to move with economic-cycle conditions.

Definition: A cyclical stock is a stock tied to a business that usually benefits when economic activity, consumer spending, industrial demand, or credit conditions are strong, and usually faces more pressure when those conditions weaken.

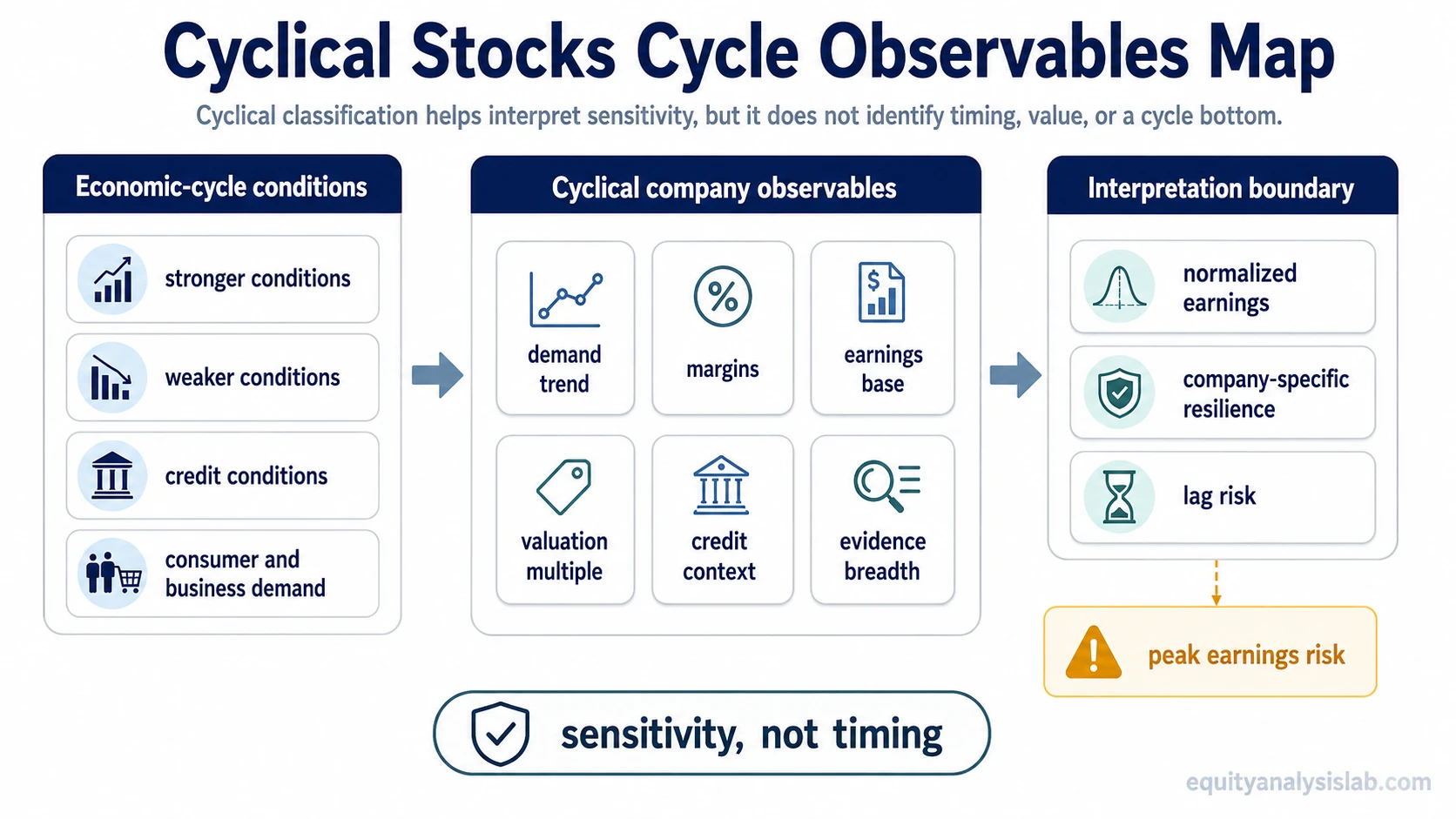

The classification helps investors understand sensitivity, not timing. A cyclical label can explain why profits may expand quickly during stronger periods and contract sharply during weaker periods, but it does not identify a market top, a market bottom, or undervaluation by itself.

Key Points

- Cyclical stocks are tied to economic-cycle sensitivity rather than stable demand.

- Demand, margins, earnings, cash flow, and valuation multiples can all change as the cycle changes.

- Sector examples help classification, but company-specific revenue mix, balance sheet strength, and cost structure still matter.

- A low valuation multiple can be misleading when current earnings are temporarily elevated.

What Makes a Stock Cyclical

A stock is usually cyclical when the underlying business depends on spending or investment that can be delayed, reduced, or accelerated as economic conditions change. This often includes businesses tied to discretionary consumption, housing, autos, travel, industrial production, materials demand, or capital equipment.

The key mechanism is operating sensitivity. When demand improves, a cyclical company may sell more units, use capacity more efficiently, gain margin leverage, and report stronger earnings. When demand weakens, the same cost base can pressure margins and make earnings fall faster than revenue.

Valuation perception can also shift. During a strong bull market or expansion phase, investors may be more willing to pay for cyclical earnings growth. During a slowdown, they may discount the same company more heavily because future profits look less durable.

Common Cyclical Stock Examples by Sector

Sector classification is only a starting point. A company can sit inside a cyclical industry but still have different sensitivity because of pricing power, contract structure, balance-sheet strength, customer mix, or recurring revenue.

| Sector or category | Why demand can be cyclical | What to examine |

|---|---|---|

| Autos and auto suppliers | Vehicle purchases can be delayed when confidence, credit availability, or household budgets weaken. | Unit volumes, financing sensitivity, inventory levels, margins, and operating leverage. |

| Travel, leisure, and hospitality | Discretionary travel and leisure spending often changes with income, employment, and confidence. | Occupancy, pricing, booking trends, fixed costs, and demand recovery durability. |

| Industrials and capital equipment | Orders can rise or fall with business investment, production plans, and financing conditions. | Backlog quality, order trends, cancellations, customer concentration, and margin sensitivity. |

| Materials and commodity-linked businesses | Revenue can depend on construction, manufacturing, commodity prices, and global demand. | Volume, price realization, cost inflation, balance-sheet strength, and cash-flow cyclicality. |

| Consumer discretionary retail | Non-essential purchases can weaken when household budgets tighten. | Same-store sales, gross margin, inventory risk, promotional pressure, and brand resilience. |

| Homebuilding and housing-linked businesses | Demand often depends on mortgage rates, affordability, confidence, and credit availability. | Orders, cancellations, backlog, land exposure, financing conditions, and affordability pressure. |

Cyclical Stocks vs Defensive Stocks

The contrast with defensive stocks comes from demand behavior. Cyclical companies usually depend more on spending that rises and falls with economic confidence, while defensive companies usually sell products or services that remain needed across weaker conditions.

Cyclical stock: earnings may be strong when demand, confidence, credit, and investment activity are improving, but may weaken quickly when those conditions reverse.

Defensive stock: earnings may be steadier because demand is less tied to discretionary spending or business-cycle acceleration.

The distinction is not absolute. Some companies combine cyclical and defensive characteristics, and the same sector can contain businesses with very different operating leverage, revenue durability, and balance-sheet risk.

Cycle Observables That Change Interpretation

Cyclical-stock analysis becomes more useful when the label is connected to observable business conditions. The same stock can look attractive, risky, or unresolved depending on whether the current earnings base is normal, temporarily elevated, or already depressed.

| Observable | What to examine | Why it changes interpretation |

|---|---|---|

| Demand trend | Orders, volumes, bookings, store traffic, backlog, cancellations, or end-market demand. | Revenue strength may be durable, temporary, or already rolling over. |

| Margins | Gross margin, operating margin, utilization, input costs, labor costs, and pricing pressure. | Margins often expand in strong periods and compress quickly when demand softens. |

| Earnings base | Trailing earnings, forward estimates, normalized earnings, and one-off gains or losses. | Peak earnings can make a stock appear cheaper than it is on normalized profits. |

| Valuation multiple | P/E, EV/EBITDA, free cash flow yield, and how the denominator changes across the cycle. | A low multiple may reflect rising uncertainty rather than clear undervaluation. |

| Credit and liquidity context | Financing availability, refinancing risk, leverage, interest expense, and customer credit conditions. | Rate and credit pressure can affect both demand and the valuation multiple. |

| Evidence breadth | Whether signals appear in one metric or across revenue, margins, cash flow, orders, and guidance. | A single strong metric may not represent the full business cycle position. |

| Lag risk | Whether reported results reflect past demand while forward conditions are already changing. | Cyclical companies can report strong results after the underlying cycle has started to weaken. |

Why Cyclical Stocks Can Look Cheap at the Wrong Time

Cyclical stocks often look most statistically attractive when current earnings are high. If margins, volumes, and cash flow are near peak levels, a low earnings multiple may reflect the market’s concern that profits are not sustainable.

Peak earnings risk: A cyclical company can screen as cheap when trailing profits are temporarily elevated. Normalized earnings, margin durability, balance-sheet resilience, and demand direction are needed before the valuation multiple has much meaning.

Free cash flow deserves the same caution. Strong cash generation during a favorable period may not represent a normal run rate if working capital, pricing, volumes, or capital spending are about to change. That is why valuation work on cyclicals usually compares current profits with a more normalized earnings base.

Simple cyclical stock example: A cyclical business falls after a weaker demand update and now trades at a low earnings multiple. At first glance, the stock appears inexpensive. The interpretation stays incomplete if margins are still compressing, free cash flow is weakening, and end-market demand has not stabilized. The stronger analytical question is whether current earnings represent normal profitability or a temporary high point from the prior cycle.

Limits and Common Mistakes

Cyclical classification is useful, but it is not a timing system. A cyclical stock can decline before a formal bear market, recover before economic data improves, or remain weak even after broad conditions stabilize.

Common mistake: Treating “cyclical” as a buy signal after a decline. The label only describes sensitivity. It does not prove that the cycle has bottomed, that earnings have normalized, or that the stock is undervalued.

Another mistake is treating every company in a cyclical sector as equally exposed. Two businesses can operate in the same sector but differ in leverage, pricing power, recurring revenue, customer concentration, cost flexibility, and exposure to financing conditions.

Interest rates can also change the interpretation. Higher financing costs may pressure demand in rate-sensitive areas such as housing, autos, and capital spending, while also affecting valuation multiples. The mechanism is broader than cyclicality alone, which is why interest-rate sensitivity should be checked separately when rates are part of the setup.

Related Concepts

Defensive demand, broad expansion or stress conditions, and rate sensitivity can all change how cyclical earnings are interpreted. The company-level work still comes back to demand durability, margin behavior, cash-flow quality, balance-sheet resilience, and whether current earnings are normal for the cycle.

FAQ

Are cyclical stocks the same as growth stocks?

No. A growth stock is usually defined by expected expansion in revenue or earnings, while a cyclical stock is defined by sensitivity to economic conditions. A stock can be both, but the labels describe different things.

Are cyclical stocks risky?

They can be more sensitive to slowdowns, credit conditions, margin pressure, and earnings revisions. The risk depends on the specific company, balance sheet, valuation, and cycle position.

Why can cyclical stocks look cheap near peak earnings?

They can look cheap because the valuation multiple is being applied to temporarily high profits. If earnings normalize downward, the apparent cheapness can disappear.