A market cycle is the repeated movement of broad equity conditions through changing phases of risk appetite, liquidity, earnings expectations, valuation behavior, and investor sentiment. The concept helps investors organize market context, but it does not identify precise turning points, prove that stocks are safe, or replace company-level analysis.

Market cycles matter because the same business can be judged very differently under expanding, slowing, stressed, or recovering conditions. Revenue growth, margins, valuation multiples, financing costs, and sector leadership can all change as the cycle evolves. The useful question is not “which phase guarantees the next move?” but “what conditions are changing, and how could those changes affect different companies?”

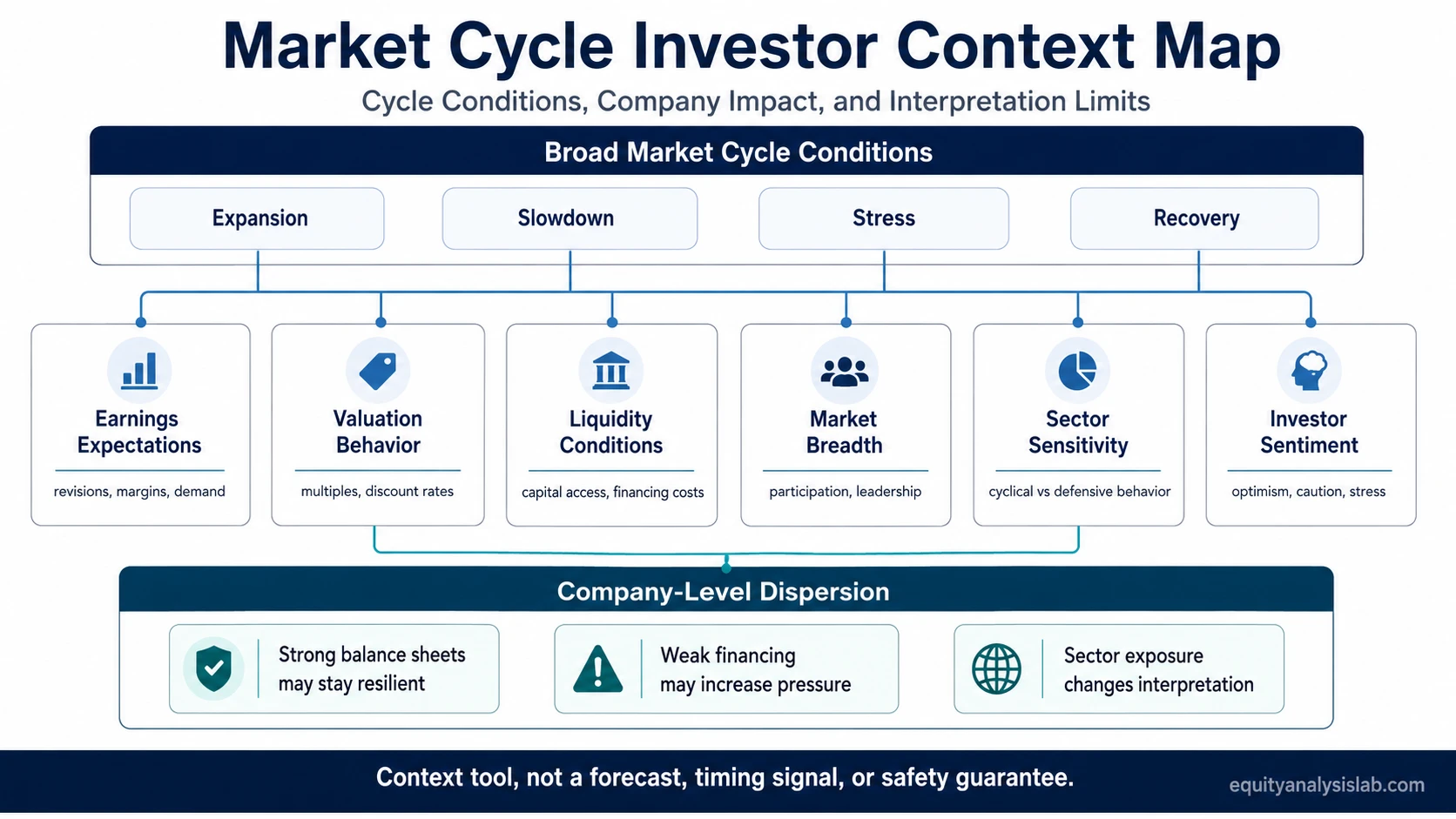

Key Points

- A market cycle describes broad changes in equity conditions, not a precise forecast of market tops or bottoms.

- Cycle phases are useful labels only when they are tied to observable evidence such as earnings trends, liquidity, credit conditions, breadth, valuations, and sector behavior.

- Market-cycle context can help investors separate broad market pressure from company-specific weakness or strength.

- A cycle label can frame the backdrop, but valuation, quality, balance-sheet risk, and return potential still require separate company-level evidence.

- Company-level dispersion remains important because strong and weak businesses can behave very differently inside the same broad cycle.

What Is a Market Cycle?

A market cycle is a recurring sequence of changing market conditions that can include expansion, optimism, valuation pressure, stress, decline, stabilization, and recovery. In equity analysis, it is best understood as a context map for interpreting risk appetite, earnings expectations, liquidity, valuation behavior, and investor psychology.

A market cycle is not the same thing as a calendar schedule. It does not move in fixed time intervals, and it does not require each phase to look identical across every index, sector, or company. Some parts of the market may show late-cycle pressure while others remain resilient. Some businesses may suffer from tighter financing conditions, while others may keep stable demand and healthy balance sheets.

For that reason, a market cycle should be treated as a broad analytical lens. It can help investors ask better questions about earnings durability, balance-sheet risk, valuation sensitivity, and sector exposure. It should not be used as a standalone reason to buy, sell, avoid, or favor any security.

How Market Cycles Work

Market cycles work through several forces that interact over time. Liquidity affects how easily capital moves through the system. Interest rates influence discount rates, financing costs, and the valuation investors are willing to pay for future earnings. Earnings expectations change as demand, margins, and business confidence rise or weaken. Sentiment can amplify these shifts when investors become too confident during expansions or too pessimistic during stress.

The mechanism is rarely clean. A stock index can rise while earnings revisions are already slowing. Valuation multiples can compress even when reported profits still look strong. Credit conditions can tighten before the damage is obvious in company results. This is why cycle analysis becomes more useful when it combines observable signals instead of relying on one label.

Market cycle mechanism:

A practical market-cycle review separates five questions:

- Liquidity: Is capital becoming easier or harder to access?

- Earnings: Are expectations rising, stabilizing, or being revised lower?

- Valuation: Are investors paying more or less for the same future earnings?

- Breadth: Is market strength broad, or is leadership narrowing into fewer stocks?

- Company sensitivity: Which businesses are more exposed to demand, financing, or margin changes?

This mechanism keeps the concept investor-centered. A market cycle can describe the backdrop, but the actual investment question still depends on the business, price, balance sheet, earnings quality, and risk being evaluated.

Market Cycle Phases

Market-cycle phases are useful shorthand, but they are not precise labels that markets announce in real time. Different sources may use different names, and phases can overlap. The table below uses a simple investor-context version rather than a mechanical timing model.

| Phase | What often changes | Investor interpretation | Main limitation |

|---|---|---|---|

| Recovery | Sentiment improves, liquidity may ease, and earnings expectations begin to stabilize. | Investors may look for evidence that conditions are improving beyond the first rebound. | Early rebounds can fail if earnings and credit conditions do not confirm the improvement. |

| Expansion | Risk appetite strengthens, earnings revisions improve, and market breadth can widen. | Broad participation can support confidence, but valuation discipline still matters. | Strong price action does not prove that every company is high quality or fairly valued. |

| Late cycle | Valuations may become stretched, leadership can narrow, and margin or rate pressure may rise. | Investors may pay closer attention to balance-sheet strength, earnings durability, and cyclicality. | Late-cycle conditions can persist longer than expected and are not automatic sell signals. |

| Downturn | Risk appetite weakens, earnings forecasts fall, credit conditions tighten, and market breadth deteriorates. | Stress can expose fragile business models, high leverage, and weak cash generation. | A decline alone does not prove that an asset is cheap or near a durable bottom. |

| Stabilization | Volatility may remain high while selling pressure slows and forward expectations stop deteriorating. | Investors may compare improving conditions with remaining risks in earnings and liquidity. | Stabilization is not the same as a confirmed new expansion. |

The phase names are less important than the evidence behind them. A market can appear to be in recovery on price alone while earnings revisions, credit spreads, or sector breadth still point to fragility.

What Investors Can Observe

Market-cycle analysis becomes more useful when it is tied to observable conditions. No single measure confirms the whole cycle, but a group of signals can help investors understand whether broad conditions are improving, deteriorating, or becoming more uneven.

| Observable area | What to examine | Why it matters |

|---|---|---|

| Earnings revisions | Whether analysts and companies are raising or cutting future expectations. | Market prices often respond to changes in expected earnings before reported results fully reflect them. |

| Margins | Whether input costs, labor costs, demand weakness, or pricing pressure are compressing profitability. | Margin pressure can turn revenue growth into weaker earnings quality. |

| Liquidity and credit | Whether financing conditions are becoming easier or tighter for companies and investors. | Tighter credit can pressure leveraged businesses and speculative parts of the market. |

| Interest rates | Whether discount rates and financing costs are rising or falling. | The way higher rates can pressure equity valuations is often a key cycle mechanism. |

| Market breadth | Whether gains or losses are spread across many stocks or concentrated in a narrow group. | Broad participation can show healthier risk appetite, while narrow leadership can signal fragility. |

| Sector sensitivity | Whether economically sensitive groups are leading or lagging more stable demand areas. | Sector behavior can show how investors are pricing growth, recession risk, inflation pressure, or defensiveness. |

| Valuation behavior | Whether multiples are expanding, compressing, or diverging across sectors. | Multiple expansion can support returns during optimism, while multiple compression can offset earnings growth. |

A useful cycle review compares these areas rather than forcing them into one answer. When earnings, breadth, liquidity, and valuations point in different directions, the market-cycle label should remain tentative.

Market Cycle Context and Company-Level Analysis

Market cycles do not affect all companies equally. A broad downturn can pressure most risk assets, but the damage may be far greater in businesses with weak balance sheets, unstable margins, high financing needs, or demand tied closely to economic confidence. A broad expansion can lift many stocks, but the strongest long-term outcomes still depend on business quality and valuation discipline.

This is where market-cycle context becomes useful for equity analysis. It helps separate three different questions: whether the broad backdrop is supportive, whether the sector is sensitive to that backdrop, and whether the individual company has the quality and valuation to justify investor attention.

Example: Same Cycle, Different Company Impact

Consider two companies during a slowing economic phase. One sells products that customers can delay, uses debt heavily, and depends on strong consumer confidence. The other has recurring demand, modest leverage, and more stable cash flow. The broad market cycle may pressure both valuations, but the operating risk is not the same. The cycle label gives context; company analysis explains the difference.

This distinction is especially important when reviewing cyclical stock behavior. Economic sensitivity can make some companies more exposed to changes in demand, credit, and investor sentiment, but it does not automatically make them bad investments or good investments. The price paid, earnings durability, capital structure, and cycle position all matter.

What Market Cycles Do Not Prove

A market-cycle label is not proof of timing, safety, valuation, company quality, or future return. It can describe the environment, but it cannot confirm that a top has formed, a bottom is complete, a stock is cheap, or a company is financially strong.

The main limitation is real-time ambiguity. Investors usually recognize clean cycle labels more easily after the fact than during the transition. A market can look weak before recovering, expensive before moving higher, or resilient before earnings pressure appears. Treating a phase label as certainty can create false confidence.

Another limitation is aggregation. A broad index can hide major differences underneath the surface. Large companies may support the index while smaller companies weaken. Defensive areas may hold up while economically sensitive groups deteriorate. High-quality companies may remain resilient while speculative companies collapse.

Because of that dispersion, market-cycle analysis should support company analysis rather than replace it. A cycle view may explain why investors are becoming more cautious, but the individual security still requires a separate review of business quality, financial strength, valuation, and risk.

Market Cycle vs Related Concepts

A market cycle is the broader sequence of changing market conditions. Related terms describe narrower pieces of that sequence.

| Concept | How it differs from a market cycle |

|---|---|

| bull market conditions | A bull market describes a broad rising environment, while a market cycle includes rising, slowing, declining, and recovering conditions. |

| bear market | A bear market describes a broad declining environment, while a market cycle describes the wider sequence that can include the decline and the eventual stabilization. |

| Business cycle | The business cycle focuses on economic activity, while a market cycle focuses on how financial markets price changing expectations, risk, and liquidity. |

| Sector rotation | Sector rotation describes changing leadership among groups of stocks, while a market cycle describes the broader environment in which leadership changes occur. |

| Market timing | Market timing tries to identify entry and exit points, while market-cycle analysis is safer when used as context rather than a precise timing system. |

The distinction matters because related labels can overlap without meaning the same thing. A market can be in a broad expansion while some sectors lag. A downturn can resemble a bear market in one index but look milder in another. The better interpretation comes from matching the label to the evidence being observed.

Common Mistake: Turning a Cycle Label Into an Investment Thesis

The common mistake is treating the market-cycle label as the thesis itself. Saying that conditions look early-cycle, late-cycle, bullish, or stressed does not explain whether a specific company has durable earnings, strong cash flow, reasonable leverage, or an attractive valuation.

A better process starts with the cycle backdrop and then narrows the analysis. If liquidity is tightening, which companies are most exposed to refinancing risk? If margins are under pressure, which businesses can defend pricing power? If market breadth is narrowing, is the weakness concentrated in speculative names or spreading into higher-quality companies?

This approach keeps market-cycle analysis useful without turning it into a forecast. The label frames the questions. The evidence answers them.

FAQ

What is a market cycle?

A market cycle is the repeated movement of broad market conditions through phases such as recovery, expansion, late-cycle pressure, downturn, and stabilization. It describes changing risk appetite, liquidity, earnings expectations, valuation behavior, and investor sentiment.

What are the main market cycle phases?

Common market cycle phases include recovery, expansion, late cycle, downturn, and stabilization. The exact labels vary, and phases can overlap, so they should be treated as analytical context rather than precise real-time signals.

Is market cycle analysis the same as market timing?

No. Market cycle analysis organizes broad conditions, while market timing tries to identify exact entry or exit points. A cycle label can help frame risk, but it does not prove when a top or bottom will occur.

Can a market cycle label prove that a stock is cheap?

No. A market cycle label does not prove valuation, quality, safety, or future return. A stock still needs company-level analysis, including earnings quality, balance-sheet strength, cash flow, valuation, and business sensitivity.