Sector rotation is the shift in market leadership from one stock-market sector to another as expectations about growth, earnings, rates, liquidity, valuation, and risk appetite change.

It describes where relative strength is moving inside the equity market. It does not prove that a sector is cheap, safe, early, late, recession-proof, or likely to keep leading.

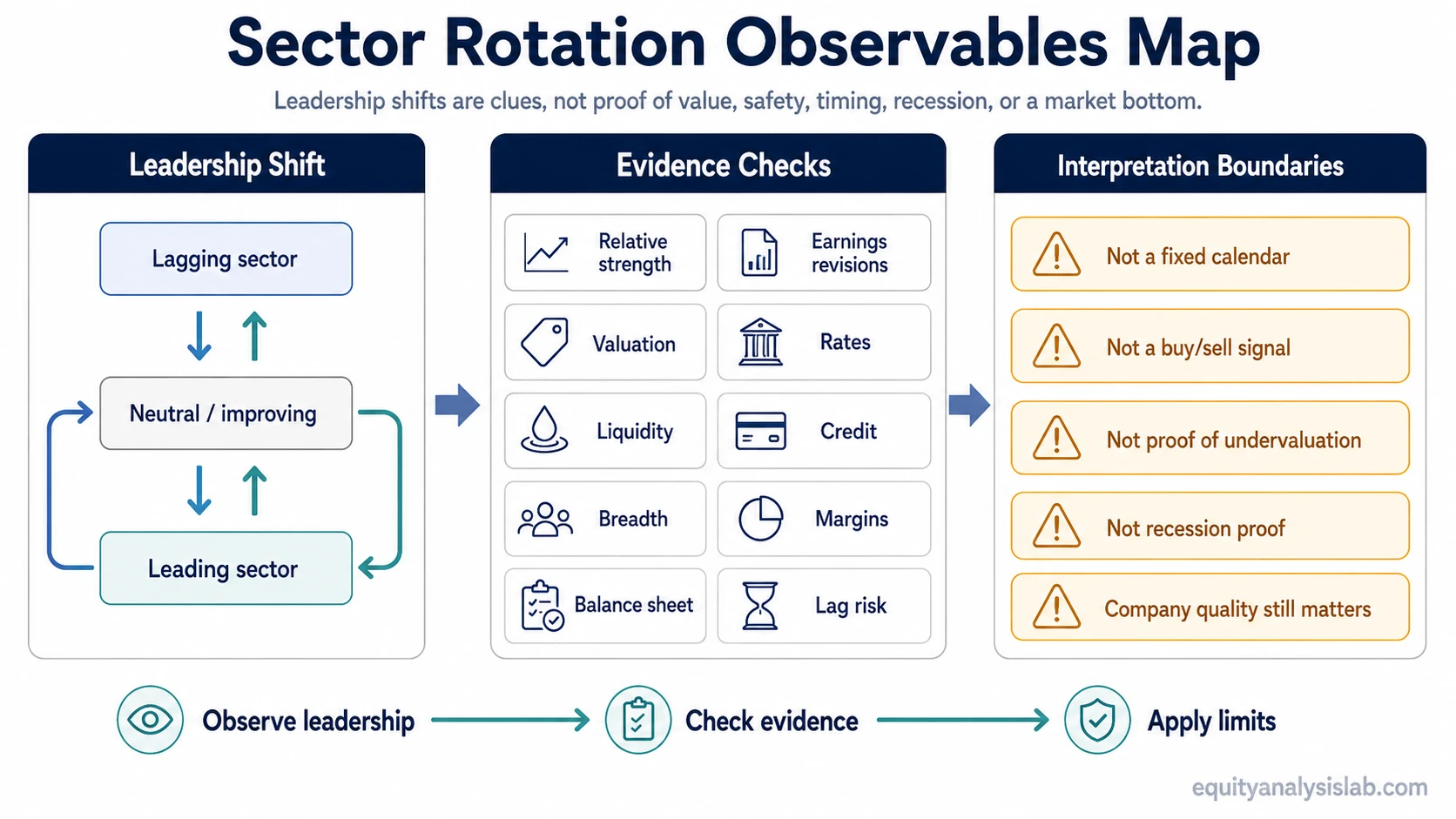

Definition: Sector rotation is an observable change in sector leadership. Investors use it to study which areas of the market are gaining or losing relative strength, then compare that movement with fundamentals, cycle conditions, and risk signals.

Key Points About Sector Rotation

- Sector rotation means leadership shifts between sectors, not that a specific sector must be bought or sold.

- Rotation can reflect changing expectations about earnings, inflation, interest rates, liquidity, credit, and risk appetite.

- Cycle maps can help organize the idea, but sector leadership does not follow a fixed calendar.

- Sector strength needs confirmation from valuation, earnings quality, margins, balance-sheet risk, and breadth.

- The label is an analytical starting point, not a timing signal, recession verdict, market-bottom signal, or proof of undervaluation.

What Is Sector Rotation?

Sector rotation starts with relative leadership. A sector may begin outperforming the broader market, stop lagging, or lose leadership while another group strengthens. The shift can happen across economically sensitive sectors, defensive groups, rate-sensitive industries, or growth-oriented areas of the market.

The concept is easiest to understand alongside the broader market cycle, but the two ideas are not identical. A market cycle describes broad phases in risk appetite and economic expectations. Sector rotation focuses more narrowly on which parts of the equity market are leading or lagging inside that environment.

For investors, the useful question is not “which sector comes next?” The better question is whether sector leadership is supported by earnings expectations, valuation, balance-sheet strength, credit conditions, and company-level quality.

Why Sector Leadership Changes

Sector leadership changes because different businesses respond differently to growth, inflation, interest rates, credit conditions, and consumer demand. A stronger growth backdrop can help economically sensitive groups, while stress or slower demand can push attention toward businesses with steadier revenue patterns.

Cyclical stocks often receive more attention when investors expect stronger demand, operating leverage, or earnings recovery. Defensive stocks can attract attention when investors care more about revenue stability, cash-flow durability, or lower economic sensitivity.

Interest rates can also change the interpretation. Some sectors are more sensitive to discount rates, financing costs, or credit availability. The relationship between yields and equity valuation is covered more directly in why stocks fall when interest rates rise.

How Investors Can Observe Sector Rotation

Sector rotation becomes more useful when leadership is checked against several layers of evidence. Relative price strength alone can show that money is moving, but it cannot explain whether the move is fundamentally supported, already crowded, or late.

| Observable | What it can suggest | Why it is not enough alone |

|---|---|---|

| Relative strength | Which sectors are leading or lagging versus the broader market. | Price leadership can be late, crowded, or disconnected from fundamentals. |

| Earnings revisions | Whether analysts and investors expect improving or weakening fundamentals. | Revisions can lag price moves and may change quickly if demand weakens. |

| Valuation | Whether leadership is already pricing in optimistic expectations. | A strong sector can still be expensive, and a weak sector is not automatically cheap. |

| Rates | Whether duration-sensitive sectors, financials, or leveraged businesses are being affected by yield changes. | Rate moves can reflect growth optimism, inflation pressure, policy stress, or risk aversion. |

| Liquidity | Whether risk appetite appears to be expanding or tightening across equities. | Liquidity conditions are broad inputs and do not identify company quality by themselves. |

| Credit | Whether sector strength is supported or contradicted by stress signals. | Credit stress can weaken the interpretation even when equity prices still look firm. |

| Breadth | Whether leadership is spread across many stocks or concentrated in a few large names. | Narrow leadership can make a sector look stronger than the average constituent. |

| Margins | Whether input costs, pricing power, and operating leverage support earnings durability. | Revenue growth may not translate into profit if margin pressure rises. |

| Balance sheet | Whether rate sensitivity, refinancing needs, or credit exposure change the risk profile. | Sector labels can hide large differences between strong and weak companies. |

| Lag risk | Whether the observed rotation may already reflect expectations that have been priced in. | A visible rotation can become less useful after the market has already repriced the story. |

Same Rotation, Different Interpretation

A growth-oriented sector can lead because earnings expectations are improving, because lower rates support long-duration cash flows, or because risk appetite is expanding. The same price leadership has different meaning depending on whether breadth is improving, valuation remains reasonable, credit conditions are calm, and company fundamentals support the move.

A defensive sector can strengthen because investors want steadier cash flows, but that does not automatically prove a recession. It may also reflect valuation reset, temporary earnings resilience, falling yields, or weakness in more cyclical areas. The surrounding evidence determines whether the move is a useful clue or a misleading headline.

What Sector Rotation Does Not Prove

Sector rotation does not prove that a sector is undervalued. Valuation still depends on earnings quality, cash flow, balance-sheet strength, growth durability, and expectations already embedded in price.

Sector rotation does not prove safety. Even a group with steadier demand can fall if valuation is stretched, earnings disappoint, rates move against the sector, or the broader market is under pressure.

Sector rotation does not confirm a recession or identify a market bottom. Defensive leadership can appear inside a bull market, and cyclical rebounds can happen inside a bear market rally. The label needs context.

Common Mistakes When Reading Sector Rotation

- Treating a cycle chart as a calendar: Sector leadership can change before, during, or after a visible economic shift. Markets price expectations, not a clean timetable.

- Confusing sector strength with company quality: A strong sector can contain weak companies, poor balance sheets, stretched valuations, or fragile earnings.

- Ignoring valuation: A sector can lead because expectations have improved, but that improvement may already be reflected in price.

- Reading defensives as a recession verdict: Defensive leadership can indicate caution, but it does not prove that the economy is already in recession.

- Turning observation into action too quickly: Rotation can help frame research, but it should not replace company analysis, portfolio risk review, or valuation work.

Sector Rotation Versus Sector Type

Sector rotation and sector type are related, but they answer different questions. Sector rotation describes changing leadership. Sector type describes economic sensitivity. The distinction matters because a sector can be cyclical, defensive, rate-sensitive, or growth-oriented without always leading at the same point in every cycle.

The comparison between cyclical and defensive stocks helps separate sector sensitivity from sector leadership. A sensitivity label describes how a business may respond to conditions. Rotation describes how market leadership is actually shifting.

Related Concepts

- Market cycle: the broader environment that can influence sector leadership.

- Cyclical stocks: companies whose revenue and earnings tend to be more sensitive to economic conditions.

- Defensive stocks: companies often analyzed for steadier demand and lower economic sensitivity.

- Cyclical vs defensive stocks: the distinction between sensitivity types, not a forecast of which group must lead next.

- Bull market and bear market: broad market conditions that can affect how sector leadership is interpreted.

FAQ

Is sector rotation a timing signal?

No. Sector rotation can show that leadership is changing, but it does not identify an exact entry point, exit point, or next winning sector.

Does sector rotation prove a recession?

No. Defensive leadership or cyclical weakness can indicate caution, but recession analysis requires broader economic and market evidence.

Can sector rotation happen inside a bull market?

Yes. Leadership can shift within a rising market as earnings expectations, rates, valuation, and risk appetite change across sectors.